Euro Strengthens, Dollar Weakens

The euro has gained more than 3% since the start of the month, reaching its strongest level since 2018. The sharpest leg of the move came this week, following European leaders’ agreement on a multi-billion-euro package to support the recovery of the European economy. Since late March, when the plan was finalized, the euro has strengthened by roughly 7%.

Importantly, the euro’s appreciation in response to the recovery fund is not primarily driven by expectations of a direct near-term boost to European growth. The agreed size of the package, particularly its grant component, may still prove insufficient, and there are substantial open questions around the practical implementation of the Recovery and Resilience Facility, not least due to deliberately vague language on conditionality that was likely necessary to secure political agreement. For the euro’s longer-term outlook, however, what matters most is the programme’s financing structure and the political signal it sends.

Joint European bonds

The European Commission will raise the agreed EUR 750 billion by issuing bonds in the capital markets. The key point is that these bonds will not be issued by individual member states; the issuer will be the European Commission itself. In effect, the EU will issue a form of common debt backed by all member states, regardless of which countries ultimately receive support.

For years, joint European debt was a political taboo that could not be broken due to resistance from wealthier northern countries. The severity of the current crisis, however, has persuaded even the most important prior opponent, Germany. The taboo has been broken and the EU has crossed a Rubicon, moving in the direction of a fiscal union.

This is positive for the euro for several reasons. A monetary union without elements of fiscal union has never been fully coherent from an economic standpoint and has created serious structural vulnerabilities for the euro area. Investors have long priced a degree of “redenomination risk” into the euro, reflecting concerns that in a severe crisis the euro area could fragment, potentially threatening the currency itself.

The current crisis could have triggered a new European sovereign debt crisis, given that the countries hit hardest by the pandemic are also among the most indebted. The agreement among European leaders, combined with ECB bond purchases that have departed from the capital key in favor of Italy and other higher-risk jurisdictions, has materially reduced this risk.

Next Generation EU’s planned joint issuance also means that countries such as Italy, Spain, and Greece should be able to borrow on exceptionally favorable terms, potentially even at negative yields, given that the European Commission, as issuer, carries a top-tier credit rating. If these countries were forced to issue on their own, borrowing costs could rise and spreads could widen sharply on sustainability concerns. Italy and Spain are also set to receive the largest allocations from the grant component of the fund. The risk of a renewed debt crisis in the euro area that would threaten the integrity of the currency union has therefore been significantly reduced, particularly if joint issuance proves to be more than a one-off response.

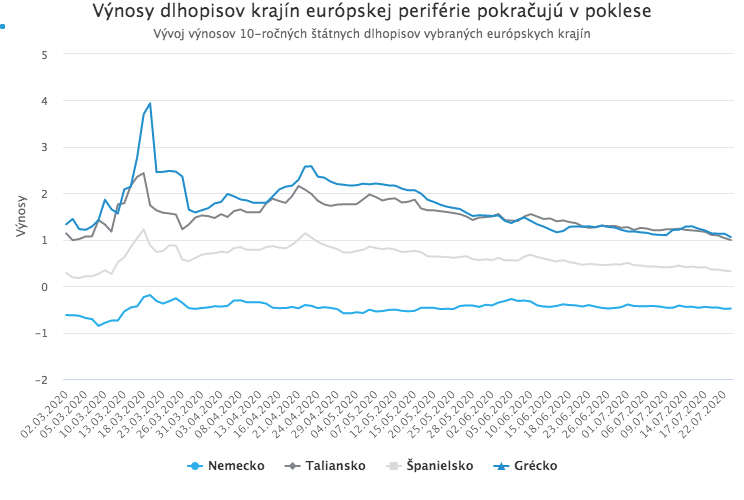

Markets have reflected this shift. Yields in Europe’s “periphery” fell further after the deal, and the spread between Italian and German yields has compressed back toward pre-pandemic levels. Ten-year Italian yields are now only around 40 basis points above U.S. Treasuries.

The euro as a reserve currency

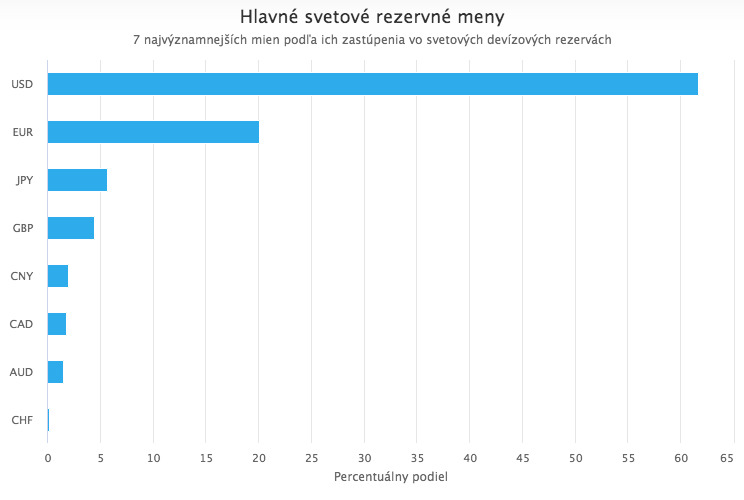

Joint European bonds also have a longer-term positive implication: they increase the euro’s appeal as a reserve currency. They are likely to support a higher share of euro-denominated assets in global foreign-exchange reserves, potentially at the expense of the U.S. dollar.

For a currency to achieve true reserve status, it is not enough to have a large economy and a credible central bank. The system also requires a sufficiently deep supply of safe assets denominated in that currency, allowing reserve managers to park large sums at low risk. This has been one of the euro’s structural weaknesses. The safest euro-area sovereign issuers, led by Germany, have historically been among the most fiscally conservative and have issued relatively limited quantities of government debt compared with the U.S. or Japan. That has constrained the pool of genuinely “safe” euro assets and limited the incentive and ability to accumulate euro reserves.

Joint issuance changes this dynamic by creating a substantial supply of high-quality euro-denominated bonds that can function as a natural reserve asset.

The dollar is weakening

While the euro has strengthened sharply, the dollar has weakened just as visibly. Part of this is mechanical, given that EUR/USD is the most heavily traded currency pair and euro strength necessarily implies dollar softness. But the dollar is also facing additional headwinds.

In the near term, these include escalating tensions with China, domestic political risks ahead of the election, and the still-unresolved coronavirus situation, which threatens a fragile U.S. recovery. More structurally, the flood of dollar liquidity following the onset of the pandemic has eased pressures that previously supported dollar appreciation. In addition, the Fed’s rapid rate cuts have largely eliminated what had been a significant interest-rate differential in favour of the dollar versus other major currencies. Together, these factors have reduced the dollar’s relative attractiveness.

In the current environment, a weaker dollar is a tailwind for the global economy, as an excessively strong dollar could have undermined the early stages of the post-pandemic recovery. Dollar weakness also supports risk assets and has been a key driver of the latest surge in gold prices.

Option markets and investor surveys suggest that most market participants are currently positioned for further dollar weakness and additional euro strength. That said, the ECB remains an important constraint. An excessively strong euro would weigh on the recovery of Europe’s export-oriented economy and would also work against the ECB’s inflation objectives