Trump’s Diagnosis Shook Markets. Investors No Longer Believe in His Electoral Victory.

Market moves following the announcement of President Trump’s diagnosis suggest that investors have largely stopped believing he will win the election. These moves also indicate how to best position a portfolio for a potential victory by his opponent, Joe Biden.

President Trump’s announcement that he tested positive for coronavirus immediately stirred turbulence in financial markets as well. Equities and other risk assets fell sharply. Trump’s diagnosis injected yet another massive dose of uncertainty into an already exceptionally uncertain political environment in the United States.

The US is only a few weeks away from one of the most important elections in its history, taking place at an extraordinarily turbulent time. The outcome will have an enormous impact on the country’s subsequent political and economic trajectory. Investors and analysts are, of course, trying to anticipate the result and position their portfolios accordingly, but it is more difficult than ever.

The last election already demonstrated that polling cannot be relied upon. Moreover, while analysts typically consider only two outcomes, a victory by one candidate or the other, this election cycle has openly discussed a third, and worst, possibility: Trump loses the election officially but refuses to accept the outcome, pushing the country into a deep political crisis. This third scenario is considered most likely if the result is close.

Investors are therefore extremely nervous about the approaching election. This is also visible in options-market data, which point to expectations of elevated volatility in November and December. Trump’s illness has further amplified this already significant election uncertainty.

Another unknown added to an ocean of uncertainty

It was clear that such a major event would materially alter the probabilities of the various election scenarios. The problem, however, was that until the situation stabilized and more information became available, no one knew in which direction. Questions around the potential course of the illness and how the public would respond created an almost endless range of scenarios to consider.

Will Trump overcome the virus without major complications and use it in his campaign? If so, will downplaying the virus win him more support, or will it instead repel voters given how many Americans have already died from Covid? Or will the virus take a severe course and effectively remove Trump from the campaign during its final stretch? Would people sympathize with him and would his polling improve, similar to Boris Johnson when he battled Covid?

If the illness becomes serious, could it bring Republicans and Democrats in Congress closer together and motivate them to overcome hostility and finally agree on a new economic support package? Or will the phenomenon known as “rally around the flag/leader” fail to materialize among US voters, and would a severe course of illness instead hurt Trump’s prospects by fully exposing how misguided his previous dismissive stance on the pandemic was?

And what about Trump’s own posture? Would a longer hospitalization late in the campaign strengthen his determination to refuse to accept a potential defeat? And what would happen under the worst-case scenario, if Trump were to succumb to the disease? Would the election even take place as scheduled? Would the economy become entirely secondary?

Simply too much uncertainty. And markets hate uncertainty more than anything else. It is therefore not surprising that immediately after Trump’s late-night announcement, futures on the major equity indices fell by more than 2%.

Trump’s chances of victory are declining

Greater clarity reached markets only as additional information about the president’s health condition emerged throughout Friday and then over the weekend. By Monday, market behavior suggested that most investors had already formed a clear base-case expectation for the next phase. It can be summarized as follows:

Trump will recover without major complications, but the episode will damage his electoral prospects because it prevents his campaign from following its strategy of diverting attention away from the pandemic toward (alleged) economic achievements and the nomination of a conservative Supreme Court justice. This implies a further widening of Biden’s lead over Trump, bringing not only greater confidence that Biden will indeed win, but also a higher probability that Trump will accept the election result in the event of a decisive defeat with a large margin.

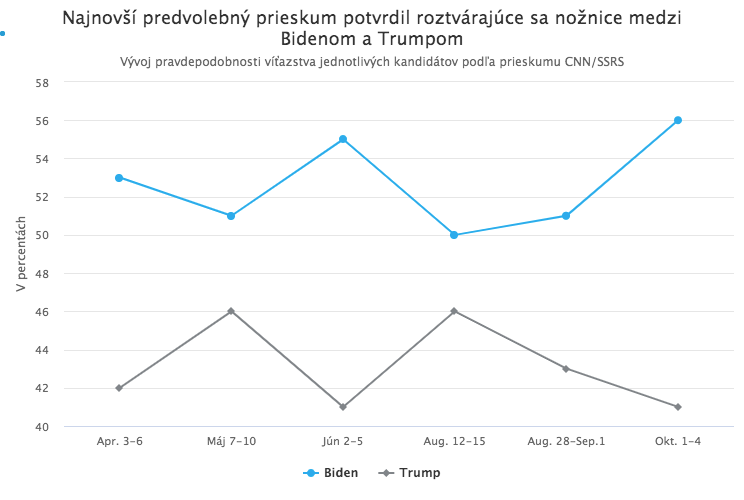

This widening gap between the two candidates was also reflected in a CNN/SSRS poll conducted precisely during the period 1 to 4 October:

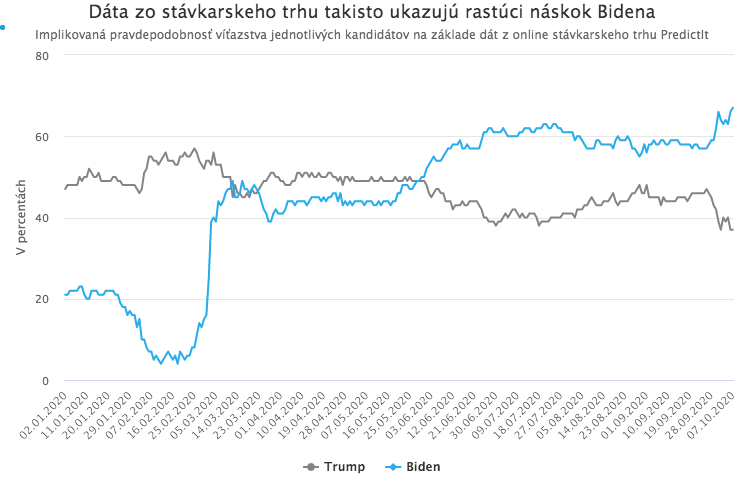

The implied probability derived from data on the largest online prediction market, PredictIt, points even more clearly in the same direction.

Expectations of a clear Biden victory also suggest that Democrats could gain control of the Senate. A Biden victory coupled with a Democratic Senate would, on the economic front, imply a near certainty of large fiscal stimulus, higher corporate taxes, renewed attempts to regulate large technology companies, and increased support for “green” technologies. From an investment perspective, such a policy mix would imply the following:

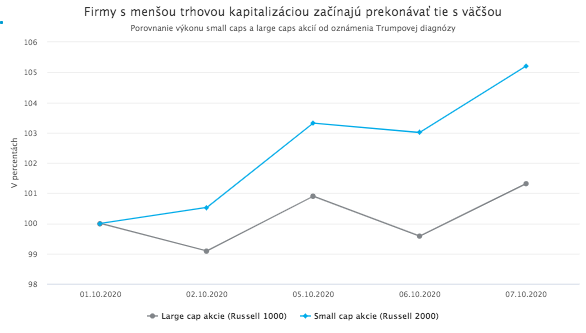

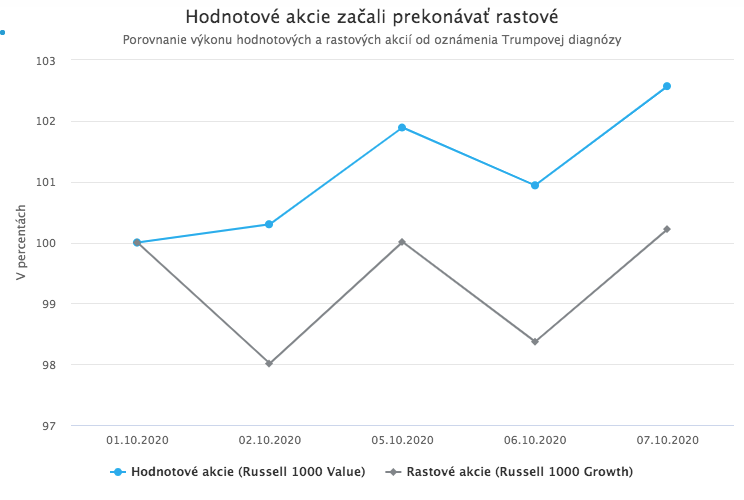

Smaller-cap stocks (small caps) should outperform larger-cap stocks (large caps); so-called value stocks should outperform growth stocks. Large technology stocks would, of course, be expected to lag. Companies focused on renewable energy and infrastructure development would be expected to benefit. Increased fiscal stimulus spending would also raise public debt, and higher Treasury issuance should logically put downward pressure on prices and upward pressure on yields. Over the longer term, this would tend to weaken the US dollar.

How to trade the expected Biden victory?

Market movements since Trump’s coronavirus diagnosis reflect precisely these expectations. Small-cap stocks began to outperform large caps.

Value stocks have also been outperforming growth stocks.

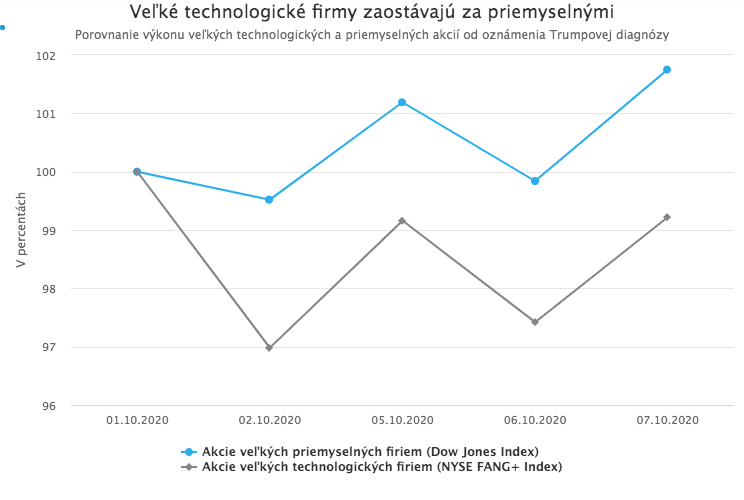

And large technology firms began to lag industrials.

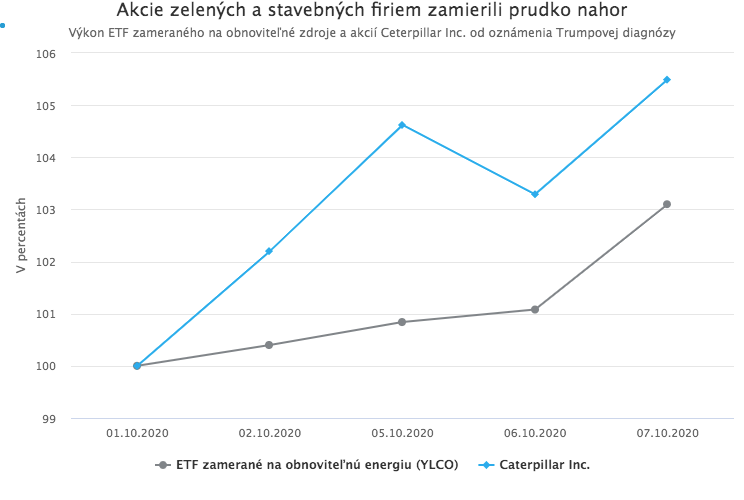

Shares of renewable-energy companies and construction firms, which would likely benefit from higher infrastructure investment, moved higher.

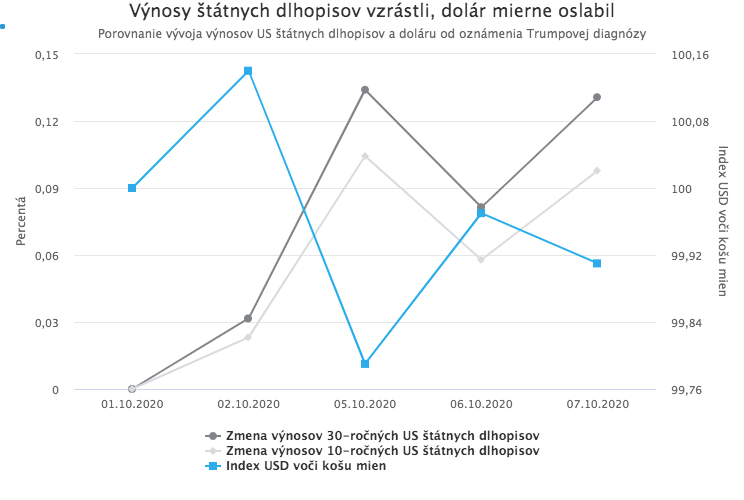

Finally, expectations of higher public spending under a Biden administration were also reflected in higher US Treasury yields and a mild weakening of the dollar.

By the way, the brief move in the opposite direction visible on each of the above charts on 6 October was the result of a Trump tweet calling for an immediate end to ongoing negotiations between Democrats and Republicans over new fiscal stimulus. A few hours later, however, he changed course and tweeted that he would support a more limited stimulus package.

Market moves in recent days therefore show not only what political outcome investors expect, but also indicate how to position a portfolio for a Biden victory. One can only hope that this time, neither polls nor investors are mistaken, and that Trump will accept defeat without unnecessary delays or unrest.