German Election Results Calm Equity Markets

Germany’s weekend election delivered a tight result and several surprises. The exact shape of the next government and the identity of the next chancellor will only become clear after weeks, if not months, of coalition talks. Even so, equity markets reacted positively. The distribution of votes makes it clear that a purely left-wing government involving the radical Left Party (DIE LINKE) cannot materialize, and that was the scenario investors feared most.

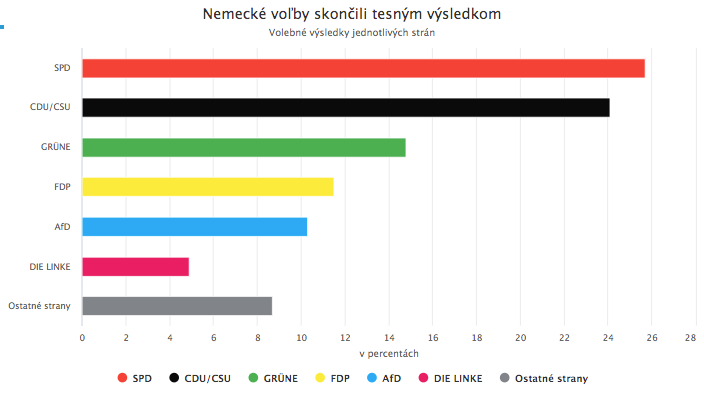

According to preliminary (still unofficial) results, the winner was the Social Democratic Party (SPD) led by Olaf Scholz, which secured almost 26% of the vote. This outcome would make the SPD the largest party in the Bundestag again for the first time in 16 years. In a close second place, the conservative CDU/CSU bloc led by Armin Laschet, who succeeded outgoing Chancellor Angela Merkel at the helm of the party, won around 24%.

While the result represents a historic success for the Social Democrats, it is a humiliating defeat for the CDU/CSU, which dominated German politics under Merkel’s leadership for 16 years.

In third place were the Greens, which have been gaining steadily in recent years and won nearly 15% of the vote. The liberal FDP also entered parliament with 11.5%, as did the far-right Alternative for Germany (AfD) with 10.3%. The far-left DIE LINKE narrowly made it as well with 4.9%, though it significantly underperformed expectations.

Jamaica or “traffic-light” coalition?

With the two largest parties, SPD and CDU/CSU, for now ruling out cooperation with each other; no party willing to work with the far-right AfD; DIE LINKE unacceptable to the right; and, given its weak result, not a particularly useful partner for the center-left either, it is highly likely that the Greens and the FDP will end up as the kingmakers. If these two parties join either of the two largest blocs, the resulting coalition would command a workable parliamentary majority.

A coalition of the SPD with the Greens and the FDP is commonly referred to as the “traffic-light” coalition, reflecting the parties’ colors. By contrast, a CDU/CSU-Greens-FDP coalition is typically labeled the “Jamaica” coalition.

The SPD is, in principle, in a stronger position to form a government given its first-place finish. Ultimately, however, everything will depend on detailed coalition negotiations, which in Germany often take months. For the SPD, the main challenge may be reaching agreement with the FDP, which is ideologically closer to the CDU/CSU than to the center-left SPD.

If the FDP fails to align with the SPD and the Greens on policy priorities, a task that will be difficult given the ideological gaps, the SPD may not be able to form a government. In that case, the CDU/CSU would likely attempt to do so instead. It would probably find it easier to strike a deal with the FDP and would work hard to reach an arrangement with the Greens.

The status quo is likely to hold

At this stage, neither the composition of the next coalition nor the identity of the next chancellor is known. The person who ultimately takes office will face the difficult task of succeeding Angela Merkel. Nevertheless, the election results already provide several important signals about the likely direction of German policy, and what that means for the economy and financial markets.

Perhaps the most important takeaway is that centrist parties strengthened overall at the expense of more radical forces. It is therefore highly likely that, whether Germany ends up with a “Jamaica” coalition or a “traffic-light” coalition, the policy status quo in key areas will broadly hold. The presence of the FDP in a traffic-light coalition, or of the Greens in a Jamaica coalition, also implies that the government program will have to remain sufficiently centrist to be acceptable to all coalition partners.

From an investor perspective, this broad centrist outcome may matter more than the precise coalition constellation or the name of the future chancellor.

Given AfD’s political isolation, a far-right government was never a major concern. Instead, markets were primarily focused on the risk of a purely left-wing coalition, which could have been plausible if DIE LINKE had secured a stronger mandate and could have joined the SPD and the Greens, thereby gaining leverage to push more radical proposals. That risk could not be ruled out entirely, especially in light of Berlin’s weekend referendum in which voters supported the expropriation of 250,000 rental apartments owned by large real-estate companies.

Equity market winners

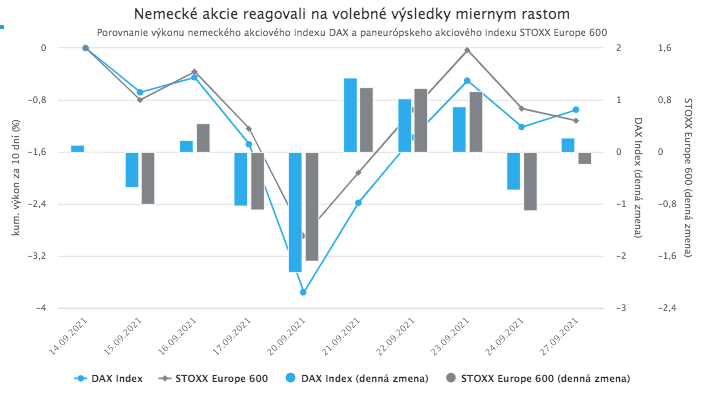

DIE LINKE’s weak showing, falling short of the 5% threshold and entering parliament only due to specific features of Germany’s electoral system, has effectively reduced the probability of a purely left-wing government to near zero. Markets responded with relief. The DAX jumped as much as 1.1% at the open. It later pared gains but still closed higher, while most European equity markets ended the day in negative territory.

Beyond the centrist tilt of the likely coalition, the results also offer one clear certainty: all plausible governing parties support increased investment in green technologies and in digital infrastructure. Wind and solar capacity is expected to expand by more than 50% over the next decade.

In equity markets, the perceived winners of the election therefore include companies exposed to green technologies, renewable power (solar and wind), and digital infrastructure. By contrast, airlines, airports, chemical-sector firms, and major polluters more broadly may face a more challenging policy environment.

If you would like help selecting specific investment instruments that can provide exposure to these long-term trends, our team at Sympatia will be happy to assist.