While a Mob Stormed Congress, U.S. Stocks Rose to New Highs

The year 2021 began at least as dramatically as the previous one. Trump’s supporters attacked the Capitol, the United States recorded a record number of daily deaths from coronavirus on the same day, and several major economies extended lockdowns. Yet U.S. stocks were not shaken by these developments and, amid the chaos, climbed to new highs.

After the difficult and turbulent year 2020, almost everyone likely wished for the new year 2021 to be a bit calmer. Unfortunately, that wish has not been fulfilled so far. The new year began at least as dramatically as the previous one, and that is saying a lot.

In the first week of last year, the world was frightened by the assassination of Iranian General Qasem Soleimani, which could have sparked a major military conflict extending beyond the region, while at the same time information began emerging about a new dangerous virus spreading in the Chinese city of Wuhan. The first January week of 2021 did not lag behind, bringing the shocking attack by Trump supporters on the Capitol, on the very day the United States recorded a record number of coronavirus deaths. Several major economies simultaneously tightened and extended lockdowns, as they struggled to stop a rapid rise in infections, and a growing number of countries reported the presence of a faster-spreading British variant of the virus.

Financial markets, however, successfully ignored these dramatic events. The dollar moved only minimally, and U.S. stocks, after a sharp rise, climbed to new highs.

Stocks detached from reality?

The situation in which live news coverage of dramatic events at the U.S. Capitol alternated in financial media with reports about rising U.S. stocks was undeniably bizarre and created the impression that financial markets are today completely detached from reality. But stock markets are traditionally resilient to unrest, they “look” ahead, and the whole situation was perceived (perhaps incorrectly) as merely a one-off security incident without broader implications for economic or political developments.

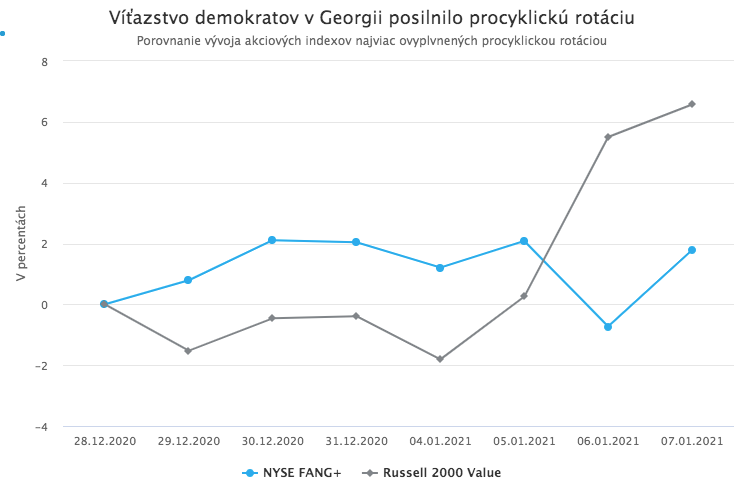

At the same time, markets drew optimism from the results of the Georgia Senate runoff elections, which also took place in the first week of January and whose outcome became clear on January 6. Both Democratic candidates won somewhat surprisingly, giving Democrats the slimmest possible majority in the Senate, which until then had been controlled by Republicans.

This narrow Senate majority means Democrats will likely not be able to push through any more radical left-wing agenda (such as tax hikes or stricter regulation). At the same time, however, they will be able to quickly approve increased stimulus for the economy (and for people affected by the pandemic). The prospect of larger stimulus is, of course, positive for stock markets and reinforces the procyclical rotation that began back in November.

The sharpest gains after the election results were announced were therefore seen in small-cap stocks, cyclical sectors, and so-called value stocks. By contrast, defensive and growth stocks of large companies led by “big tech” lagged, as they traditionally suffer the most during procyclical rotation. The difference in daily performance between small-cap value stocks (the Russell 2000 Value index) and the stocks of the 10 largest technology companies (the NYSE FANG+ index) reached an astonishing 8% on January 6, the day the Georgia results were announced.

Bond yields moved higher

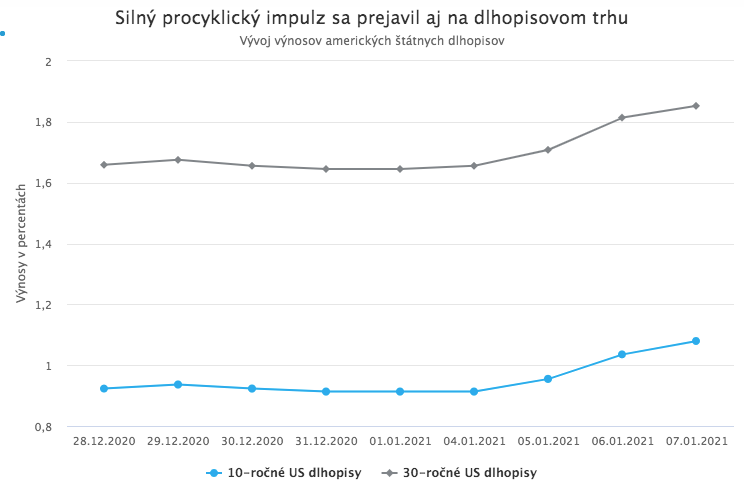

U.S. Treasuries also ignored the domestic unrest and moved in the direction of the procyclical rotation. Expected larger economic stimulus implies a larger increase in public debt and therefore greater issuance of government bonds. Higher supply then puts upward pressure on yields.

U.S. Treasury yields therefore moved sharply higher as soon as the Georgia results were known. Ten-year yields even rose above 1% for the first time since March. This development carries certain risks. If yields were to continue rising sharply and reach levels around 1.2% to 1.3%, equities would likely struggle, especially growth “big tech” stocks, which benefit most from persistently low yields. The effects of procyclical rotation on equities would thus be further amplified.

Such a sustained rise in yields, however, is not very likely at the moment, since the Fed would almost certainly not tolerate it, precisely because of its negative impact on the stock market as well as on government debt financing at a time of fragile economic recovery. The Fed, of course, has tools to quickly stop yields from rising beyond a tolerance threshold. One possibility would be extending the weighted average maturity (WAM extension) of bonds purchased under existing quantitative easing programs.

This step has been expected since the autumn of last year, and it was a surprise when the Fed did not announce it at the December meeting. If yields were to continue rising sharply during January, the Fed likely would not wait much longer and would announce a WAM extension at the January meeting, thereby quickly capping rising yields.

Rising real yields supported the dollar and pushed gold lower

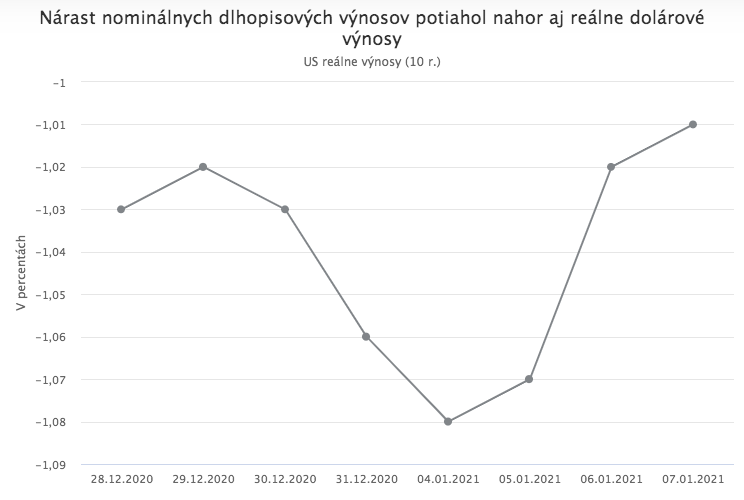

The rise in nominal U.S. bond yields also pushed real dollar yields higher over the course of the week.

It was precisely this rise in real yields that led the dollar to strengthen toward the end of the week, even though the expected increase in public debt due to larger economic stimulus should theoretically weigh on the currency.

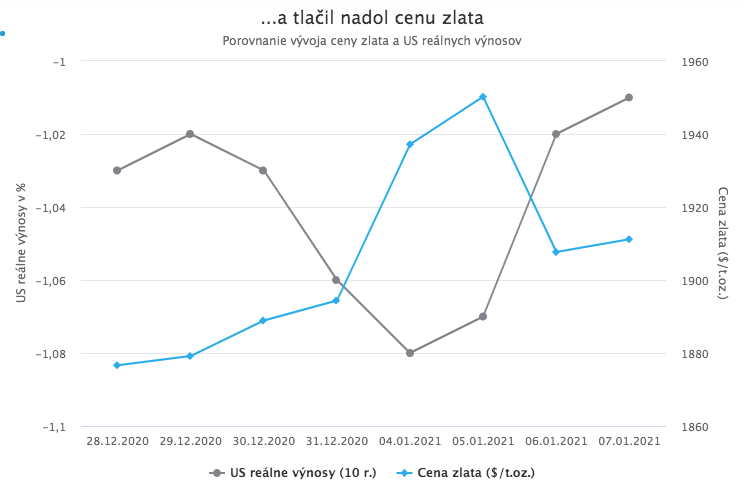

At the same time, higher real yields also contributed to a decline in gold.

As we have emphasized on these pages several times, gold responds primarily to movements in real dollar yields and the related exchange rate of the dollar, not to risk events in the world by themselves. If risk events do not translate into increased demand for U.S. government bonds that would push real dollar yields down, gold does not rise.