Bond Yields Are Rising Again and Pulling Tech Stocks Lower

U.S. and European bond yields have surged sharply higher in recent days. This move has spooked equity markets. As is usually the case when yields rise, technology stocks have suffered the steepest declines. Unlike the yield increase seen in the first months of the year, the current rise has the potential to continue for a longer period. What does this development mean for individual asset classes?

In recent days, global bond markets have seen a fairly sharp sell-off, which is quickly pushing up yields on U.S. dollar, euro, and British pound-denominated bonds.

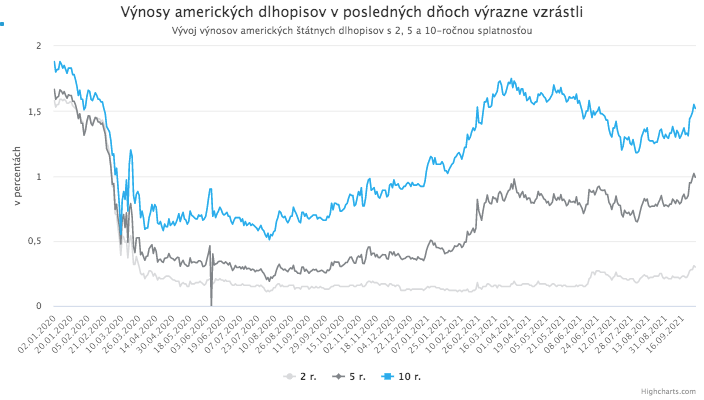

Yields on 10-year U.S. Treasuries have moved back above 1.5%, while yields on 2-year and 5-year dollar-denominated bonds have climbed to their highest levels since the pandemic began.

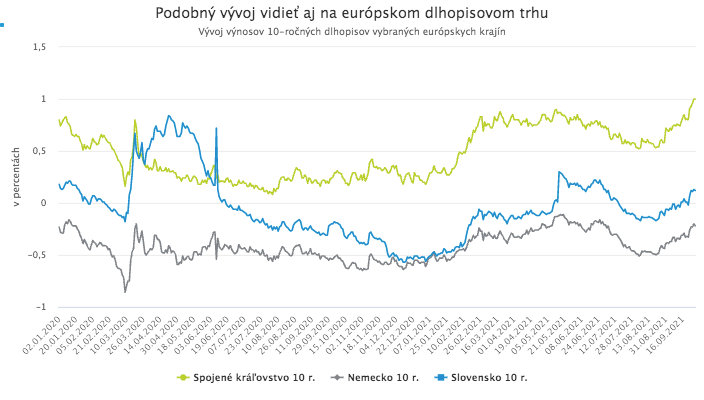

Yields on 10-year UK gilts have risen toward 1% for the first time in 18 months. German 10-year bonds are now “only” 20 basis points away from positive yields, and Slovak government bonds with a similar maturity are already back in positive territory.

This sell-off, which is driving yields higher, has been fueled by an explosive combination of several factors. Technical factors played a role as usual, but the main drivers were fundamental: the beginning of monetary tightening by several major central banks, persistently high inflation being pushed even higher by rising energy commodity prices, and a degree of optimism tied to a decline in new COVID-19 cases in the United States without the introduction of stricter measures.

Sharp moves in the bond market are, as usual, spilling over into other asset classes, above all equities.

The relationship between bond yields and the stock market

Equity markets are traditionally very sensitive to any significant moves in bond yields. What matters is not so much the absolute level of yields, but above all the speed and magnitude of their changes. Sharp declines in yields usually signal market panic characterized by a “flight to safety,” and are therefore almost always accompanied by falling stock prices.

When bond yields rise sharply, as they are doing now, stock markets also fall. Higher yields, together with expectations of higher interest rates, increase the discount rates used to value companies’ future revenues and profits. That reduces the present value of expected future cash flows, and thus lowers estimates of the intrinsic value of their stocks.

Stocks therefore typically fall when yields either rise rapidly or fall rapidly. Even so, there is one important difference between the equity market’s reaction to falling yields and its reaction to rising yields, and it is clearly visible today.

When bond yields fall quickly, the biggest declines are usually seen in the riskiest stocks, especially smaller and cyclical companies, while growth stocks of a few of the largest tech companies are relatively immune to such market sell-offs. Shares of companies such as Microsoft, Alphabet, or Apple are considered exceptionally safe due to their business models with relatively stable cash flow and their ability to grow even in an unfavorable economic environment. They are therefore something like a “safe haven” within the stock market. Lower yields (and interest rates) also increase the present value of their expected future earnings, mechanically lifting their valuations.

When bond yields rise, the opposite happens. Shares of large technology companies fall the most sharply as the present value of their expected, strongly growing future earnings declines. Meanwhile, cyclical, small-cap, and value stocks are relatively resilient because a higher-rate environment does not harm their valuations and business models as much.

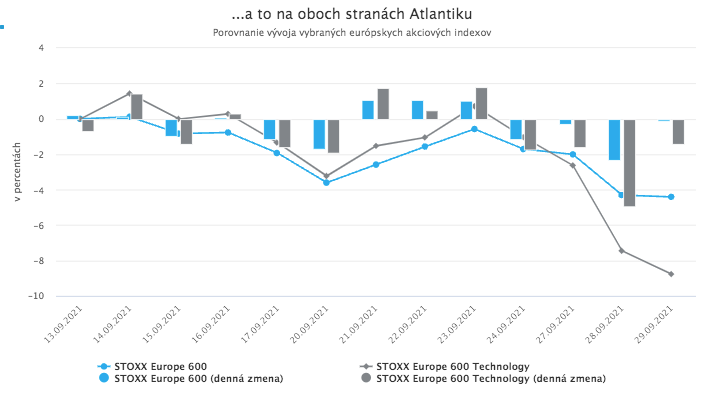

Tech stocks are falling the most

Given the relationship described above between bond yields and the stock market, it is not surprising that the current rapid rise in yields is accompanied by an equity market decline, with the biggest losses being posted by technology stocks on both sides of the Atlantic.

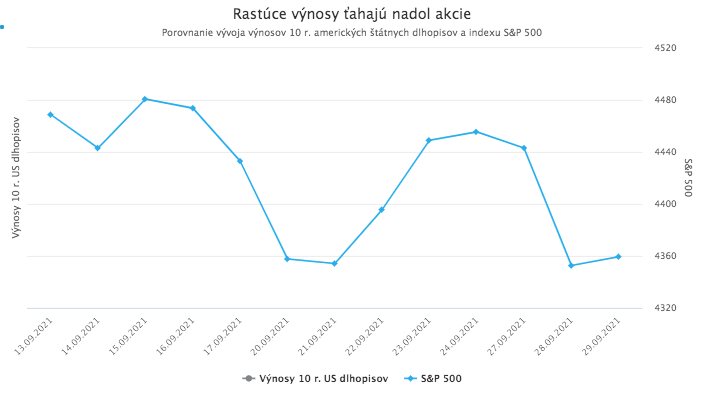

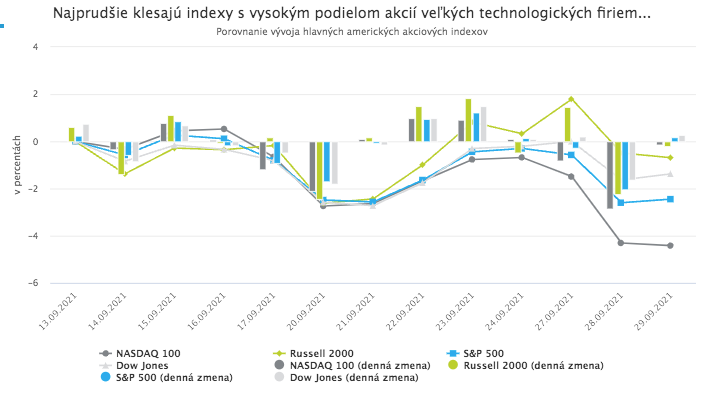

The sharpest declines occurred at the start of the week, on Monday and Tuesday. Tuesday’s losses in U.S. equities were the largest since May this year. Naturally, the deepest declines among the major U.S. equity indices were recorded by the NASDAQ, which has a high share of technology stocks.

The benchmark S&P 500 also suffered fairly significant losses, primarily due to its similarly high weighting in tech stocks. The five largest U.S. technology companies together account for more than 20% of the index. By contrast, the Dow Jones and Russell 2000 indices have been relatively resilient thanks to their composition, which includes a high share of cyclical and value, or small-cap, stocks.

Declines also occurred in European markets, where technology stocks again fell the most. Over the last two weeks, they have suffered losses twice as large as the broader European market.

Traditional portfolios may face a problem

This year, the current rapid rise in bond yields accompanied by falling stock markets is not the first such episode. Similar episodes occurred at the beginning of February and later in May. However, they did not last long. They were stopped by central banks, which concluded that it was still too early for any tightening of monetary policy, and later by concerns about the impact of the Delta variant on the global economy. This time, however, it may be different. The current rise in yields has the potential to continue for a longer period.

The central banks of South Korea, Norway, and the Czech Republic have already raised their main policy rate. The U.S. Fed has already signaled and will most likely, by December at the latest, officially announce the beginning of a gradual reduction in its regular asset purchases. A similar step is expected soon from the Bank of England, and the ECB has already reduced the volume of bond purchases under the PEPP. The central banks of the most developed economies have thus embarked on a path of tightening monetary policy.

Ultimately, rising inflation may soon leave them with no choice. Energy commodity prices continue to rise strongly and problems in global supply chains, pushing up prices across a wide range of goods, are unlikely to be resolved anytime soon. The current situation in the United States is also fueling optimism that the current Delta wave may not have as negative an effect on advanced economies as previous waves of COVID-19.

All of these factors argue in favor of further increases in yields. If yields do indeed keep rising, continued increases in bond yields will be a major problem for traditional investment portfolios composed of a “risky” equity component represented by one of the main stock indices, most often the S&P 500, and a “safe” bond component. These portfolios are built on the assumption of negative correlation between the two components. During market turbulence caused by rapidly rising yields, however, this assumption does not hold. Bond prices fall at the same time as the main equity indices.

In an environment of rising yields, it is therefore appropriate to expand traditional portfolios with additional components that are not positively correlated with stocks and bonds. These may include, for example, real estate or commodities. At the same time, it can be appropriate to adjust the equity portion of such portfolios toward a higher share of stocks that are positively correlated with rising yields, such as financial sector stocks.