Are Golden Times Ahead?

Gold has been in an uptrend for some time, but the truly sharp move has come only in recent weeks. At the end of last month, it broke above its previous all-time high and has continued to climb at a steep pace. Another milestone followed this week, when the price of the precious metal crossed the psychologically important threshold of USD 2,000 per troy ounce.

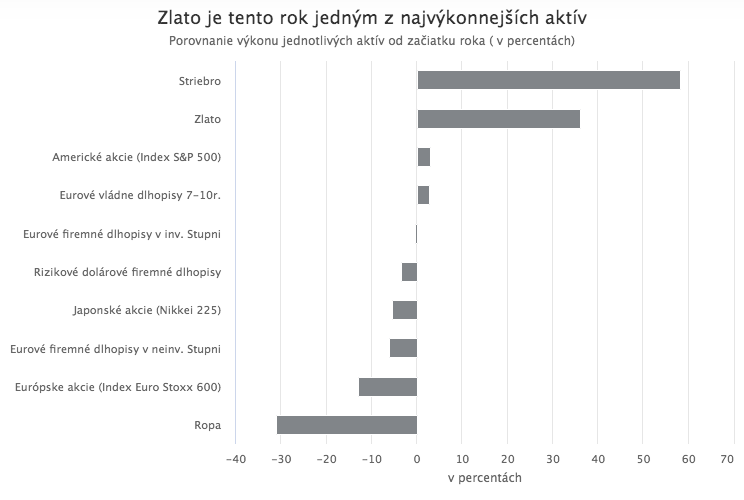

This surge has made gold one of the best-performing assets of the year. Since January, it has gained more than 36%, leaving far behind the major equity indices, which have only just begun to recover from the March sell-off, as well as bonds. The only asset that has performed better is silver, which has been catching up after a long period of underperformance versus gold, and, arguably, the shares of the largest technology companies.

Near-perfect conditions for a rally

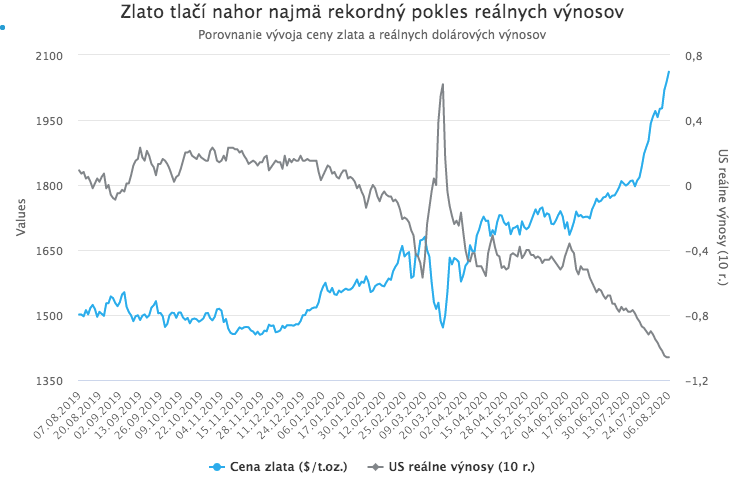

Gold’s performance reflects a combination of factors that has created close to ideal conditions for higher prices. The most important of these is likely the collapse in real U.S. yields, which has pushed them deep into negative territory.

Gold’s main disadvantage relative to other asset classes is that it is, by its nature, unproductive. Unlike traditional investment assets such as equities or bonds, it generates no income and offers no regular, predictable return. On the contrary, investors must bear ongoing costs related to storage and security. Under normal circumstances, investors who prioritize stable and predictable cash flows therefore tend to avoid it.

The sharp decline in real U.S. yields following the Federal Reserve’s aggressive rate cuts after the pandemic outbreak has fundamentally changed that calculus and effectively removed gold’s biggest disadvantage. It means that holding a “safe” dollar asset with a regular yield, such as U.S. Treasuries, now implies a loss in real terms once inflation is taken into account. The same is true for safe euro- and yen-denominated government bonds. Holding gold therefore no longer entails giving up a reliable yield.

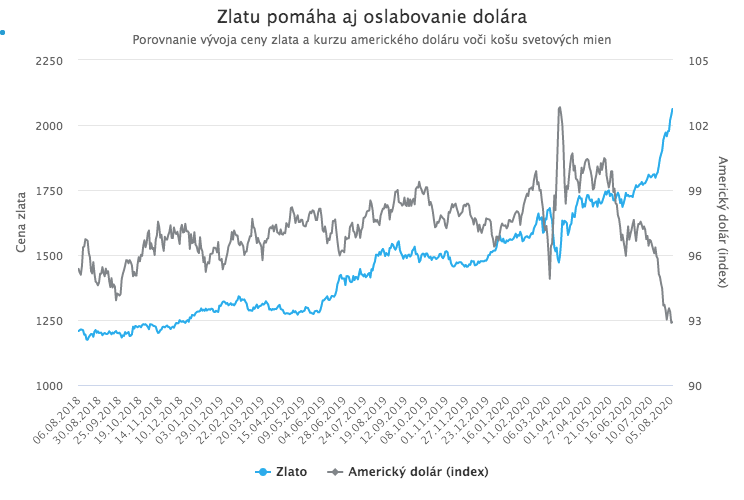

Falling real yields are also one of the key drivers behind the current weakening of the U.S. dollar. A weaker dollar, in turn, tends to be supportive for gold for several reasons.

Then there is the inflation risk. The Fed, alongside many other central banks including the ECB, flooded the financial system with liquidity in response to the pandemic and the resulting market panic. Unlike the previous crisis, large-scale monetary stimulus was accompanied by massive fiscal spending. As a result, broad money supply has risen sharply. This has reignited concerns about inflation, especially given that the path back to “normal” is likely to be long. Central-bank balance sheets are unlikely to shrink anytime soon, and fiscal spending may remain elevated for an extended period.

At the same time, it is important to note that more money in circulation does not automatically translate into inflation, particularly in the current environment where the pandemic shock has strong deflationary effects. Deflation is therefore at least as plausible as inflation. What matters, however, is that the probability of inflation is not zero. The risk exists, and prudent investors seek to mitigate it.

Under normal conditions, one of the most effective ways to hedge inflation risk is to short bonds. Higher inflation typically leads to falling bond prices and rising yields. That mechanism, however, is currently distorted by central-bank intervention. A key pillar of the policy response has been large-scale bond purchases, designed precisely to prevent bond prices from falling and yields from rising. That keeps borrowing costs for governments and companies contained, allowing them to refinance and weather the crisis without being pushed into deeper financial distress.

As a result, bond yields are being actively pressed lower by central banks, and may not respond to higher inflation with a proportionate rise in yields. Hedging inflation risk by shorting bonds could therefore fail to deliver the intended protection. Investors are forced to look for alternatives, and gold is one of them. Historically, it has been perceived as a hedge against inflation and currency debasement, even if the relationship is not stable at all times.

A gold rush

It appears, however, that part of the current rally is being fuelled by less rational forces, and those are precisely what can introduce instability. Gold has fascinated people for millennia, and even today it attracts far more media attention and public interest than most other asset classes. Whenever its price begins to rise quickly, headlines follow. That coverage draws in new buyers, reinforcing the move. Rising prices then generate more headlines, which attract even more buyers, pushing prices higher still.

The problem, as with any investment frenzy, is that there eventually comes a point when the inflow of new buyers is exhausted. Investors who rode the rally then begin closing positions to lock in profits. A scramble follows, and the price can fall as quickly as it rose.

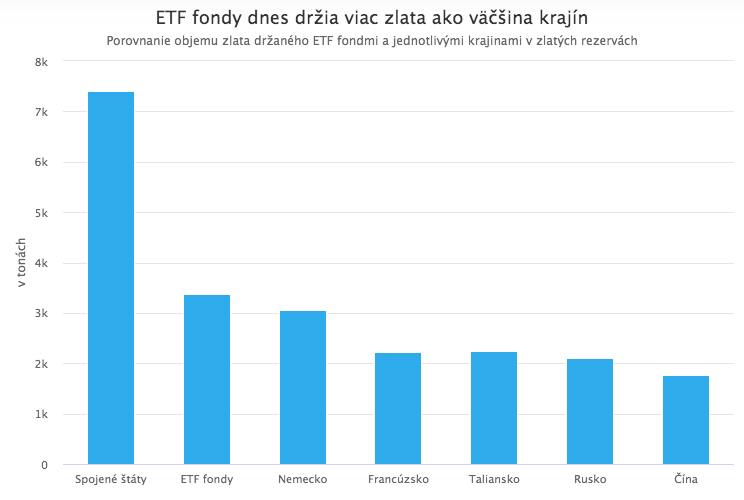

The exact point at which a rational repricing turns into speculative excess is always easier to identify in hindsight. Still, there are signs that the recent acceleration in gold prices has been amplified by a wave of retail participation. One indication is the strong inflow into gold-backed ETFs, a popular vehicle for retail investors seeking exposure to gold.

Indeed, the total amount of gold held by gold-focused ETFs has now surpassed the size of Germany’s gold reserves, the second-largest official stockpile in the world. Only the United States holds more.

Paper versus metal

The gold rally is also being supported, in part, by increasingly bold speculation that the flood of newly created central-bank money, combined with the rapid rise in sovereign debt around the world, will ultimately lead to a loss of confidence in fiat currencies, “worthless paper not backed by anything.” In such scenarios, gold, or gold-backed money, would supposedly reclaim the role of money because it “holds value” and cannot be printed at will.

Such outcomes are, of course, extremely unlikely. There is a long list of practical reasons why gold standards were abandoned in the first place. Moreover, even if one could overcome those practical barriers, it is not clear that a return to gold would solve the very problem that motivates many of its proponents.

Suppose, for example, that paper money were replaced by gold coins. Is there any reason to believe that today’s rulers or bankers would be less creative than medieval sovereigns, who repeatedly found ways to debase coinage? A gold-backed currency would face similar vulnerabilities. While central banks cannot print gold, they can change the conversion rate between currency and gold, as history has shown. Would that not be a faster, more disruptive form of devaluation than a steady, controlled inflation process?

And if gold were once again used for monetary purposes, would that necessarily benefit investors who hold it? Or would governments simply confiscate private gold holdings at an officially set exchange rate, as happened in the twentieth century?

Gold is also often viewed as insurance against truly severe outcomes, war, systemic collapse, or a breakdown of economic order. But is that really true? Does gold itself possess intrinsic value that meaningfully distinguishes it from paper? Or is its role largely a historical convention, a metal that humanity collectively decided to value because it believed others would do the same? And could that belief change again in the future?

In this context, it is also worth recalling how gold traded at the peak of the March panic, when it briefly appeared that the world was heading toward catastrophe.