Central Banks Cornered: What Will Next Year Bring?

Economic recoveries continue, but at a slower pace

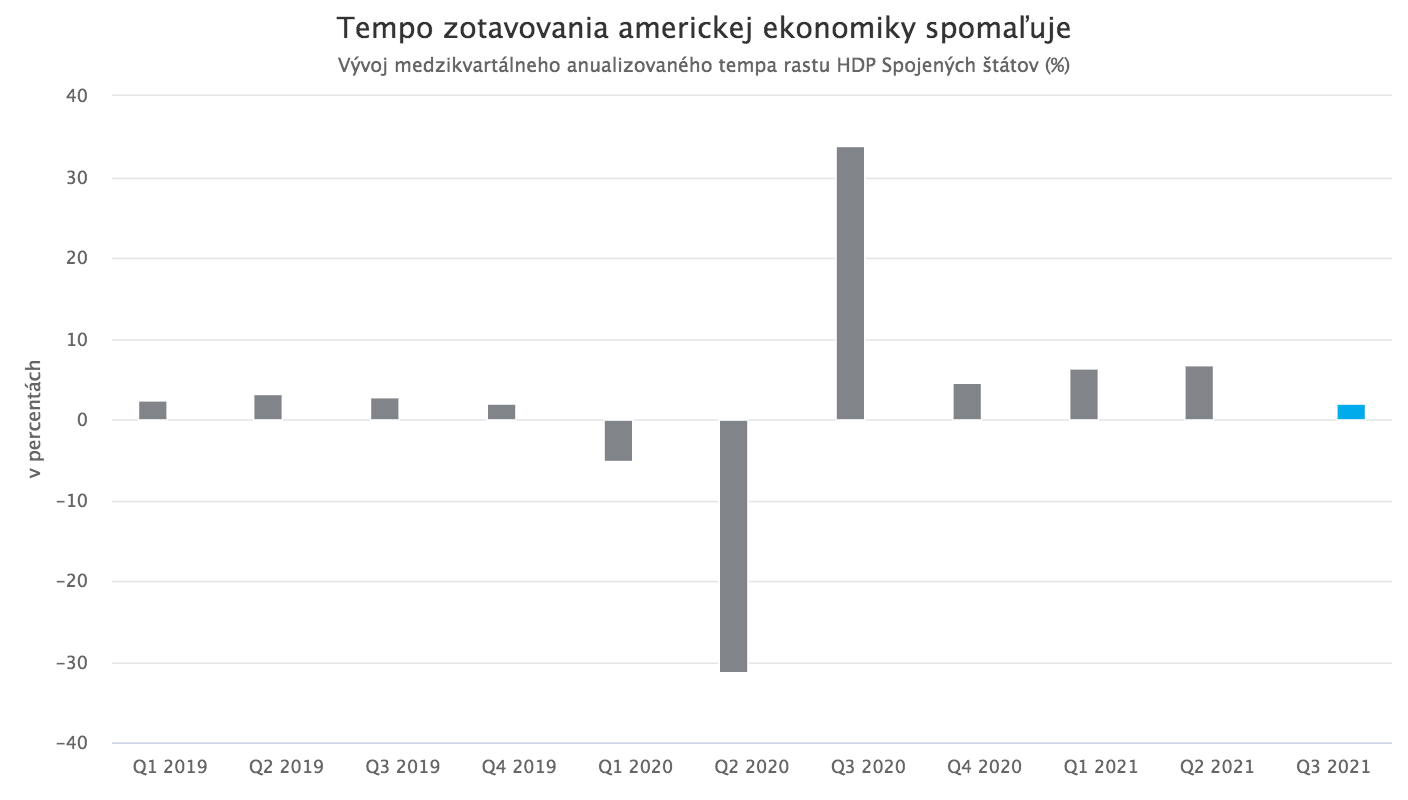

Most advanced economies, including euro area countries and the United States, continued in the second half of the year with a relatively strong recovery from the effects of the pandemic, although the pace of their rebound gradually began to slow. First in the United States, and later also in the euro area. In the US economy, signs of a slowdown in growth momentum were already clearly visible during August, when leading macroeconomic indicators began to point to a deterioration in consumer sentiment and a decline in consumer spending. This development was driven by a renewed increase in COVID-19 cases as well as persistent price increases, ongoing imbalances in the labor market, and supply-side problems including disruptions in supply chains and labor shortages in services. Consumer sentiment was also certainly not improved by the termination of a large portion of extraordinary pandemic benefits and complicated domestic political developments. The inability of Democrats and Republicans to agree on anything, accompanied by an internal struggle between the progressive and conservative wings within the Democratic Party, resulted in a de facto paralyzed Congress. Under the pressure of these factors, the US economy recorded a significant slowdown in the third quarter, achieving an annualized GDP growth rate of only 2%. This significantly lagged not only the performance of the previous quarter (6.7%) but also analysts’ expectations, which had projected 2.7% expansion.

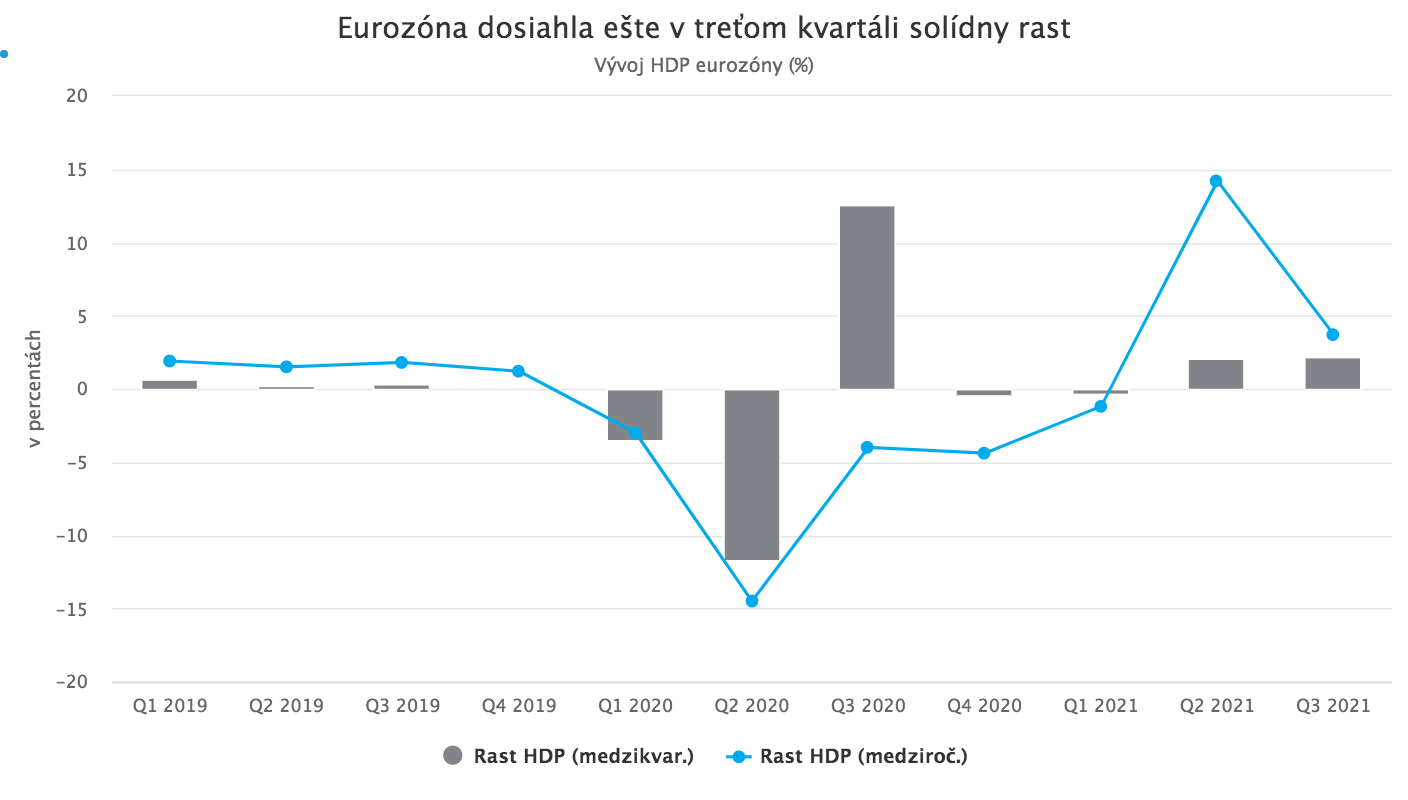

In European economies, the slowdown in the pace of recovery occurred later than in the United States. One reason is the later start of the recovery in Europe, which meant that inflation, currently accompanying the recovery of virtually all advanced economies, began to rise later in Europe than in the United States. Differences in the timing of subsequent coronavirus waves, political differences, and variations in labor market developments also played a role.

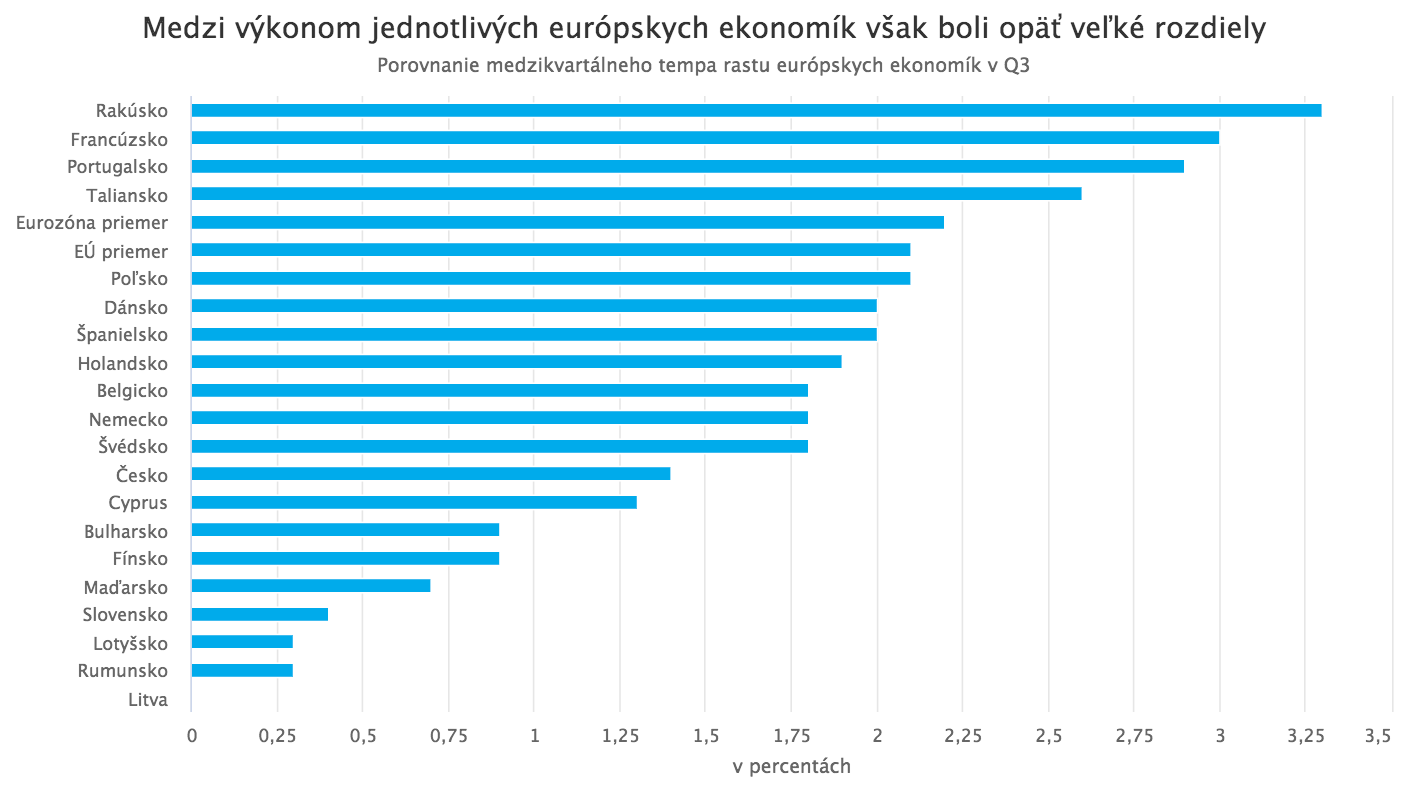

Euro area economies thus still achieved solid quarter-on-quarter growth of 2.2% in the third quarter. As usual, however, there were relatively significant differences among individual euro area economies. The pace of growth of the Slovak economy was among the weakest in the EU.

In the fourth quarter, however, European economies also began to feel the negative effects of persistent inflationary pressures as well as the winter coronavirus wave.

Complicated developments in China and other emerging markets

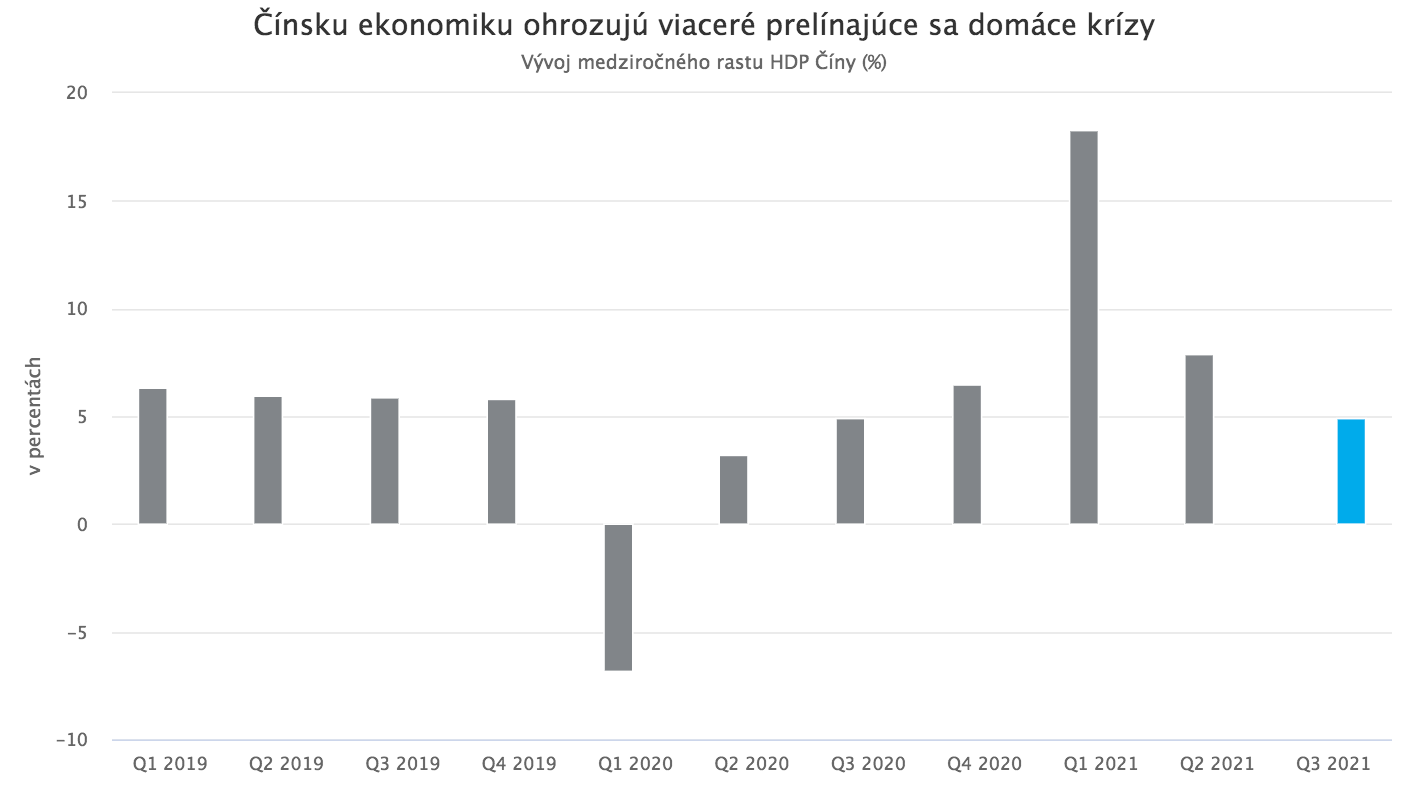

In other developed economies, broadly similar developments to those in Europe and the US took place, namely continued recovery at a slowing pace. This development stands in sharp contrast to the situation in many emerging economies, where economic recovery has not yet even begun due to extremely low vaccination rates, weak healthcare systems, and limited capacity of local economies to absorb shocks. Developments in China are specific. The pace of growth in the Chinese economy has also been slowing in recent months, but this trend is driven more by internal than external factors. The Chinese economy is currently facing several overlapping, sector-specific crises and risk factors that are increasingly weighing on its performance. These include, in particular, a crisis in the real estate sector, which accounts for as much as 20% of overall GDP, a crisis in the domestic technology sector caused by harsh regulatory interventions by the government, and an energy crisis.

The situation is further complicated by still weak consumer demand, which prevents firms from passing higher input costs on to consumers, and by the government’s “zero tolerance” approach to COVID-19, which results in factory or port shutdowns if even a single employee becomes infected. A major question going forward is whether Chinese policymakers will manage to address these crises and risk factors without triggering a major economic crisis.

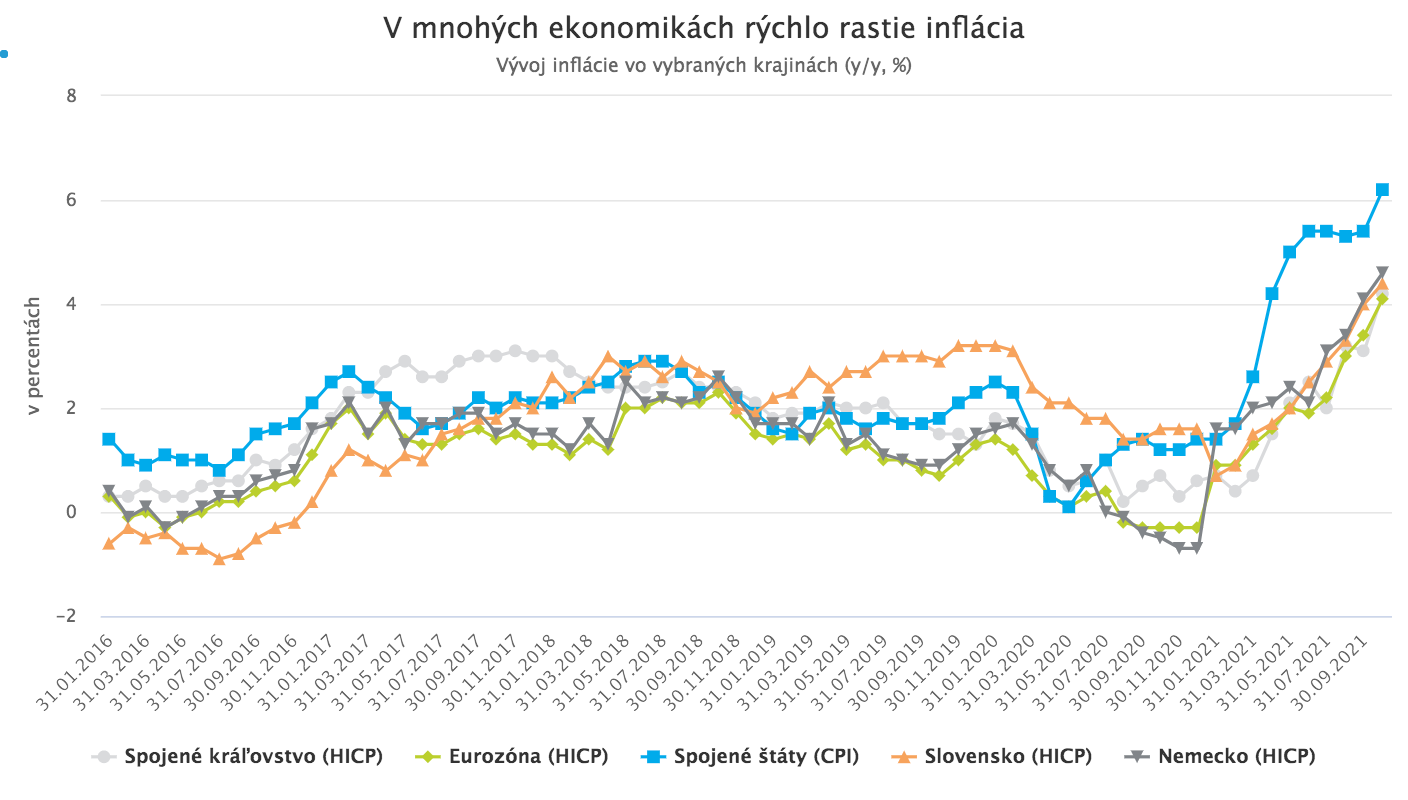

Inflation is rising rapidly

The problematic developments mentioned above in emerging economies and in China are among the causes of the current sharp rise in inflation in advanced economies, including European countries and the United States. Continued unfavorable pandemic and economic conditions in emerging countries lead to disruptions in production and in the extraction of basic raw materials, which in turn cause problems and delays in global manufacturing and supply chains. These disruptions and delays simultaneously motivate Western companies to relocate production closer to target markets, resulting in higher production costs. Frequent shutdowns in Chinese factories and ports due to COVID-19 cases, and efforts or requirements to limit energy consumption, further complicate these issues. The result is rising input and shipping costs that create upward pressure on the prices of final goods. This pressure is further reinforced by the specific pattern of demand recovery in advanced countries, where consumers and businesses were generally able to rely on generous state aid schemes during the pandemic. As a result, they did not experience a significant drop in income and accumulated savings that had nowhere to be spent during the most difficult months of the pandemic. Once the pandemic eased, however, these accumulated savings began to be spent rapidly, leading to a sharp rise in demand amid persistent supply-side problems. Finally, these factors were further compounded by an emerging energy crisis caused both by the sharp recovery of the economy from the pandemic and by political factors (Nord Stream II developments, the transition to renewable energy sources).

The interaction of these overlapping factors has led to rapid increases in consumer prices, which in individual countries are further influenced by local, country-specific factors such as the reintroduction of higher VAT in Germany or pronounced imbalances in the US labor market.

Major central banks are still waiting to raise rates

Rising inflation alongside a weakening pace of economic recovery is a major dilemma for central banks in advanced economies. The standard response of central banks to rising inflation is to raise interest rates. Higher interest rates dampen credit growth and ultimately consumer demand, reducing upward pressure on prices. The problem, however, is that this standard “recipe” for reducing inflation may not work in the current environment and could instead multiply the problems caused by high inflation. The current increase in inflation is driven primarily by supply-side factors and specific pandemic-related impacts that are largely outside central banks’ control. Raising interest rates will not solve supply chain disruptions, nor will it influence the course of the pandemic globally. The only thing a rate hike can achieve in this situation is to suppress demand.

However, the sharp and likely temporary surge in demand as economies recover from the pandemic is only one, and not the main, factor pushing prices higher. Suppressing it would not only interrupt the fragile recovery of economies from the pandemic, but might also fail to reduce inflation. The result could thus be stagflation, a stagnation of economic growth alongside persistently high inflation. The central banks of the world’s largest economies, including the Fed and the ECB, have therefore so far adopted a cautious stance. Their representatives acknowledge that the current sharp and persistent rise in inflation surprised them, but insist that it is transitory in nature and will subside over the course of next year. At the same time, they emphasize that economies have not yet fully recovered from the pandemic and therefore still require support, including in the form of accommodative monetary policy. They thus do not yet see a reason to raise interest rates. In early November, the Fed proceeded only with a partial tightening of monetary policy by beginning the gradual wind-down of regular monthly asset purchases. The ECB likewise reduced the pace of purchases under its emergency pandemic asset purchase program. Both banks, however, emphasized that they are not currently preparing to raise rates.

Unlike the Fed or the ECB, central banks of smaller and emerging countries cannot afford to wait before raising rates. They have lower credibility, less ability to influence inflation expectations, fewer effective tools, and weaker currencies prone to sharp declines. Many central banks in smaller and emerging countries have therefore already raised rates in recent months, further complicating the recovery of their domestic economies from the effects of the pandemic.

What will next year bring?

The macroeconomic outlook for the coming months is accompanied by a high degree of uncertainty, stemming primarily from the unpredictability of the further course of the pandemic and the trajectory of inflation. It is currently unclear what impact the winter wave of the Delta variant will have on affected economies, whether new antiviral drugs from Pfizer and Merck will help bring the pandemic under control, and whether a dangerous new mutation resistant to vaccines might soon emerge. The future path of inflation is likewise a major unknown. It depends primarily on resolving disruptions and delays in supply chains and imbalances in the labor market, with both factors directly linked to the evolution of the pandemic. Inflation will also be significantly influenced by the further course of the emerging energy crisis, driven not only by geopolitical developments but also by an even less predictable factor, the weather during the winter.

Future inflation developments matter not only because of their direct effects on the economy and consumer demand, but also because of how central banks respond. The risk of a “policy mistake” is high and could have serious impacts on the economy. If central banks raise rates too early or too aggressively, they could suppress growth and jeopardize the recovery. If, however, they do not react in time and lose control of inflation expectations, they will later have to respond even more aggressively, risking a recession caused by excessive rate hikes.

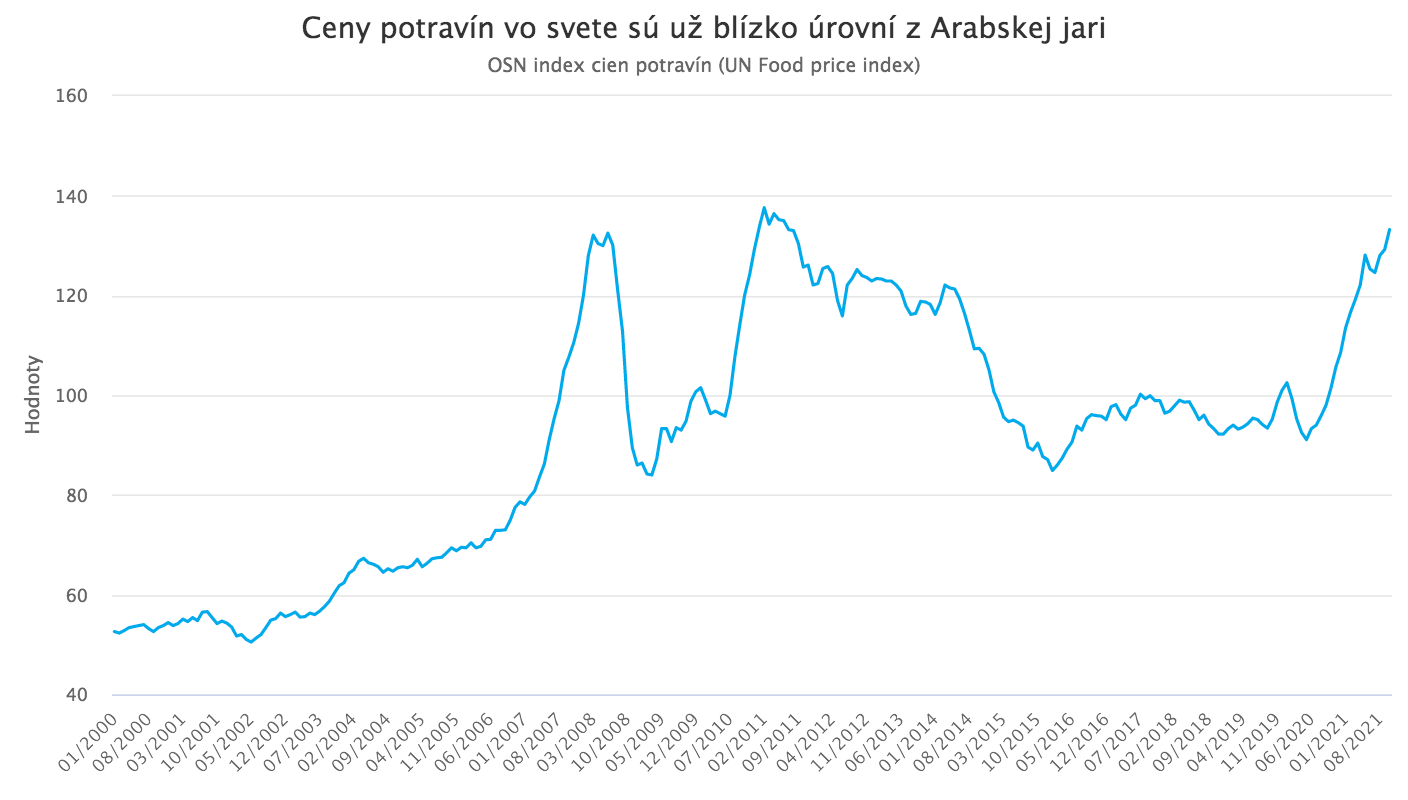

Finally, very important and even harder to predict is the impact of inflation on political developments in parliaments and on the streets, especially in emerging economies. Global food prices are already close to the record level reached during the Arab Spring, and it is believed that precisely high food prices were one of the most important triggers of the revolutions and unrest that occurred in several countries at that time.

If none of the extremely negative scenarios materializes, such as a new deadly COVID-19 variant, a sharp slowdown in China, or an energy crisis, and inflationary pressures gradually subside over the course of next year as central banks currently assume, advanced economies including euro area countries will have good conditions to continue their recovery next year at a solid pace.