US Consumer Prices and China’s Producer Prices at Multi-Year Highs

Worrying inflation data from the US and China came only a few days after representatives of the most important central banks, including the Fed, emphasized that the current rise in inflation is a problem, but so far does not provide a reason to raise interest rates. If a few more similarly troubling inflation readings arrive in the coming weeks, an early rate hike will likely be back on the table.

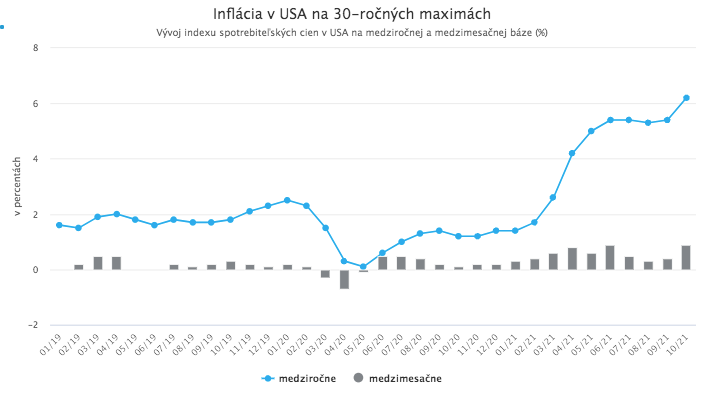

US inflation at a 30-year high

Data released last week showed that consumer prices in the United States increased by as much as 0.9% in October. This is a much larger increase than economists had expected, with forecasts ranging from 0.4% to 0.7%.

On a year-on-year basis, this represents growth of as much as 6.2%. This figure is also higher than the consensus estimate of economists at 5.9%, and at the same time it is the highest level in 30 years.

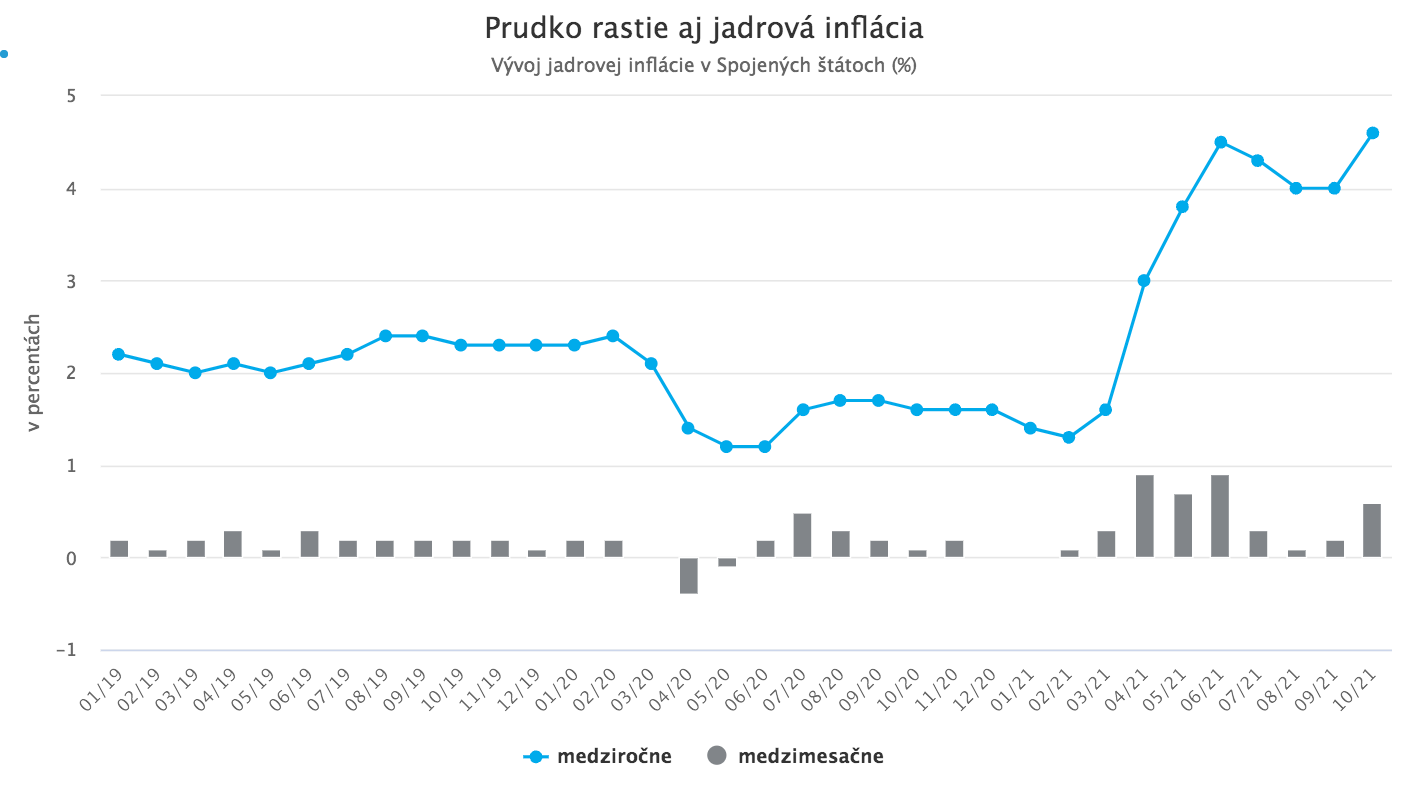

What is even more concerning is that core inflation, meaning inflation adjusted for the impact of food and energy prices, is also rising sharply and exceeding expectations. Month on month, it increased by 0.6%, and year on year by as much as 4.6%. Prices rose in housing, used and new cars, healthcare costs, household equipment, and recreation. Price pressures in the United States are therefore no longer concentrated only in a few specific items, but are spreading throughout the economy.

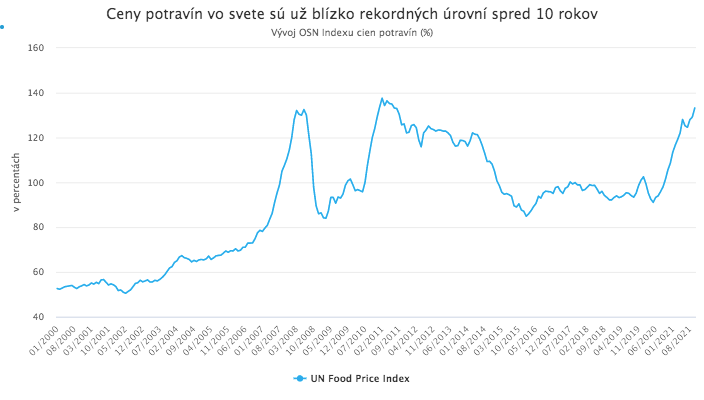

Energy and food prices continue to rise rapidly, and not only in the US. The UN index measuring global food prices is already approaching the record levels from 10 years ago, when record-high food prices contributed to the wave of protests known as the Arab Spring.

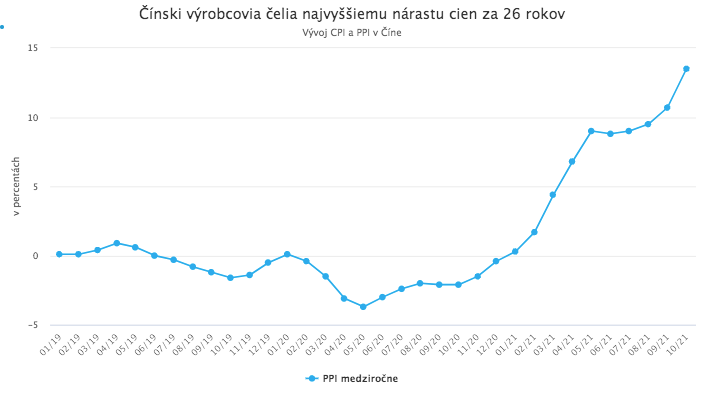

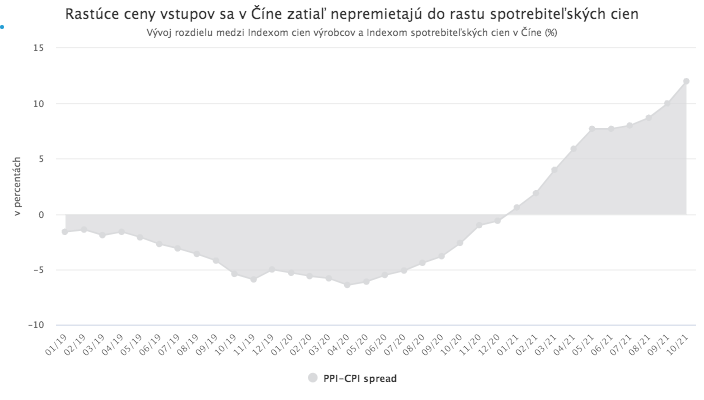

China’s producer price index at a 26-year high

On the same day as the US inflation data, new inflation figures were also released in China. They pointed to an interesting difference between the US and Chinese economies. Chinese companies are currently facing an even larger increase in input costs than US companies. China’s producer price index (PPI) recorded a year-on-year increase of as much as 13.5% in October. This is the fastest pace of increase in 26 years.

The main drivers of this sharp rise are persistently rising commodity prices as well as an acute energy shortage currently faced by Chinese manufacturers due to rising prices on global markets, alongside pressure from the Chinese government to meet emissions targets and use “greener” sources of energy. A notable difference between inflation developments in China and in the US, however, is the fact that rising production input prices in China have not yet translated into higher consumer prices. The consumer price index increased in October by only 1.5% year on year.

The gap between producer price inflation and consumer price inflation is thus a full 12%. This situation is largely a result of weak consumer demand in China, which has not yet fully recovered from the drop after the outbreak of the pandemic. A higher degree of price regulation likely also plays a role. In any case, Chinese firms cannot afford to pass rising input costs on to consumers to the same extent as American or European firms can. Their margins are therefore under strong pressure. Of course, this applies only to passing prices on to domestic consumers, not to exports to the US or European markets, which continue to be characterized by strong consumer demand. Continued rapid growth in producer prices in China will therefore likely contribute to further increases in consumer prices in the United States and Europe.

Will central banks be forced to raise rates?

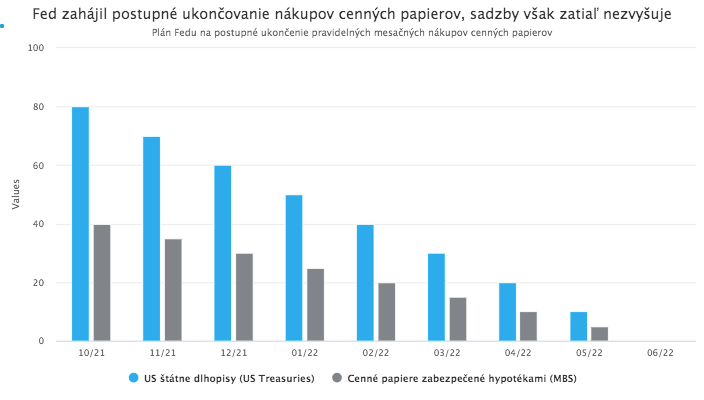

Alarming inflation data from both the Chinese and the US economies came at a delicate time. The Chair of the US Fed, J. Powell, only a few days earlier acknowledged that “the current level of inflation is not at all consistent with price stability” and pledged that the Fed would not allow “inflation to become a persistent feature of life in America.” At the same time, however, Fed officials still consider the current rise in inflation to be a transitory phenomenon that will naturally fade over time, with inflation returning in the medium term to the symmetric 2% target. At the November meeting, the Fed therefore proceeded with the expected start of the gradual wind-down of the bond purchase program by $15 billion per month, while emphasizing that it does not yet see a reason to raise interest rates.

The Fed’s stance, which is also shared by the ECB and other major central banks, has its logic. The main causes of current price pressures are supply-side factors, and so it is indeed unclear how raising interest rates would help in this situation, and whether instead of reducing inflation it would multiply problems in the economy. If inflation nevertheless continues to rise and spreads throughout the economy, central banks, including the Fed, will face an increasingly difficult challenge in insisting on the “transitory” nature of price pressures. Efforts to satisfy political pressure, maintain credibility, or attempt to anchor the public’s inflation expectations could soon lead them to raise interest rates despite the questionable effectiveness of such a step.