Equities, Bonds and Oil Post a Record Quarter

The global economy is recovering from the pandemic only gradually, and it may take years before it returns to “normal.” Financial markets, however, staged a rapid rebound in the second quarter, a V-shaped recovery in some asset classes.

Equity markets surged

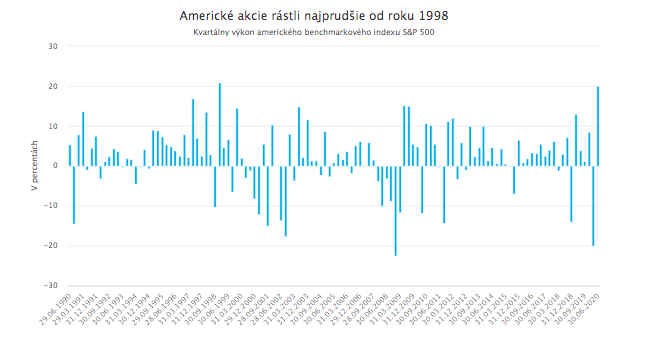

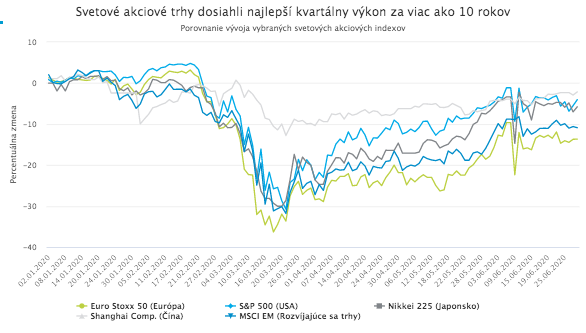

Global equities bounced back from the record sell-off in the first quarter at an exceptionally fast pace. Over the past three months, they delivered their best quarterly performance in more than a decade. U.S. equities led the move, posting their strongest quarterly gain since 1998 and effectively erasing the February and March declines.

Chinese and Japanese equities have also recouped most of their “coronavirus” losses. European equities have lagged, but still posted a solid performance, their best since 2010. Even so, they remain some distance away from fully reversing the sharp drawdown that followed the outbreak of the pandemic.

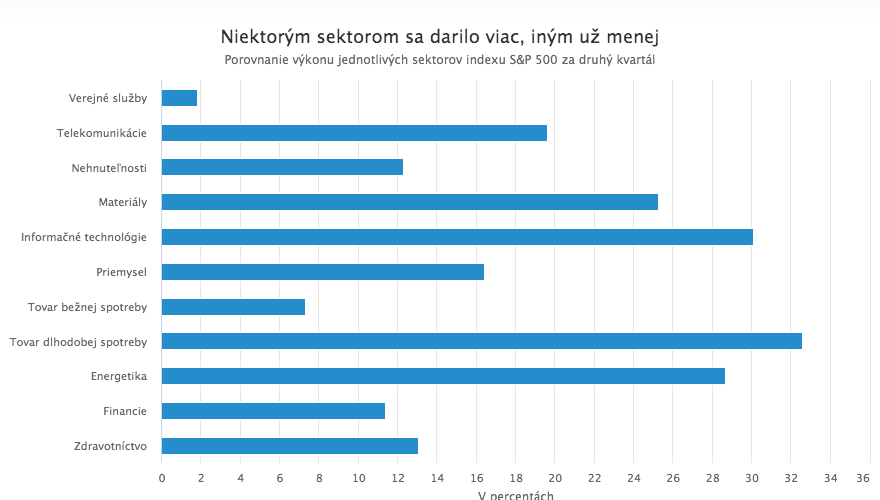

Differences are visible not only across regions, but also across sectors. The strongest performers were information technology (+30.1%), telecommunications (+19.64%), consumer durables (+32.6%), and materials (+25.3%). The energy sector also rebounded sharply in the second quarter on the back of recovering oil prices. However, given the sector’s enormous first-quarter decline (-51.6%), it still trades more than 37% below its level at the beginning of the year.

The clear winners of recent months have been large U.S. technology companies such as Amazon, Facebook, Alphabet, Apple, Microsoft, Netflix, and Nvidia. Not only have their shares recovered all initial losses from the early, volatile days of the pandemic, but in recent weeks they have climbed to new all-time highs. For perspective, the combined market capitalization of these seven firms has exceeded the combined GDP of Germany and the United Kingdom.

The contrast between the real economy and equity markets was most pronounced in April, when markets rallied sharply even as the economy was collapsing. As we discussed in one of our previous articles, the divergence between equity markets and the real economy is not, in fact, particularly surprising. Major global equity indices have little reason to track the state of the real economy as experienced by the average company or employee. They primarily reflect liquidity conditions in financial markets.

Central banks quickly stabilized the bond market

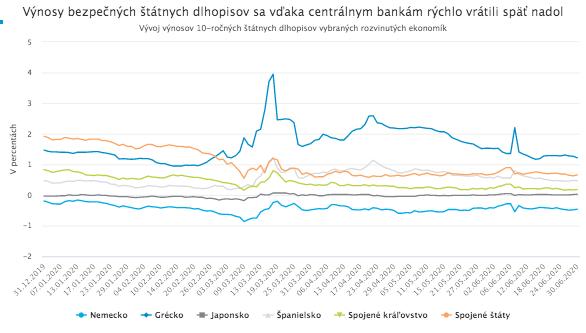

Thanks to central banks, bond markets recovered from the panic selling at the start of the pandemic even faster than equities. At the height of the market turmoil, not only did riskier corporate bonds sell off, but even government bonds in advanced economies, securities traditionally considered the safest investments, saw prices fall (and yields rise). In the scramble for cash, investors sold anything that could be sold, whether to meet margin calls on losing positions or simply to sit out the worst of the storm. Massive central-bank purchases, however, quickly pushed government bond yields back toward pre-crisis levels.

A particularly sharp spike in yields was seen in March in the debt of Europe’s “periphery,” especially Greece and Italy. Every major crisis is also a test of European solidarity and inevitably raises the question of whether wealthier and more fiscally conservative countries will leave others to the mercy of market forces.

Ultimately, the ECB’s large-scale bond purchases, with an outsized share allocated to peripheral debt, as well as the planned EUR 750 billion recovery program to support the European economy (to be financed through the issuance of common European bonds), reassured markets that the “core” would not allow the “periphery” to fail. As a result, yields on peripheral sovereign debt gradually declined over the second quarter, returning close to pre-pandemic levels.

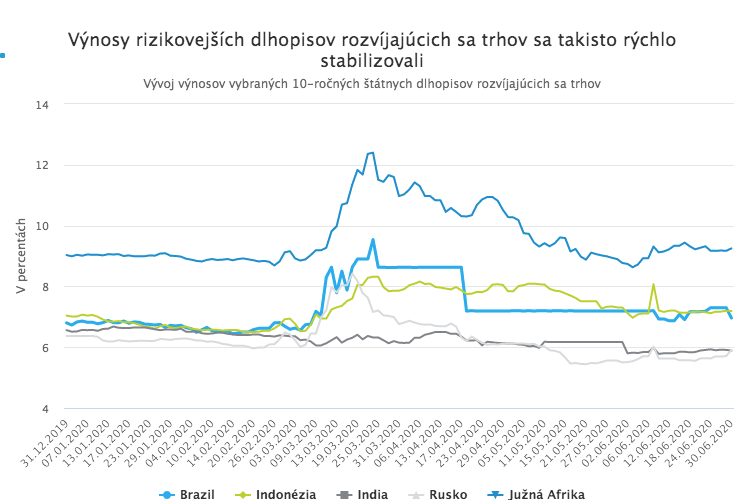

Yields on even riskier emerging-market bonds also stabilized relatively quickly. Support from domestic central banks helped, but the key factor was the U.S. Federal Reserve. Aware of its responsibility as the issuer of the world’s reserve currency, the Fed flooded not only the U.S. system but also emerging-market financial systems with dollar liquidity.

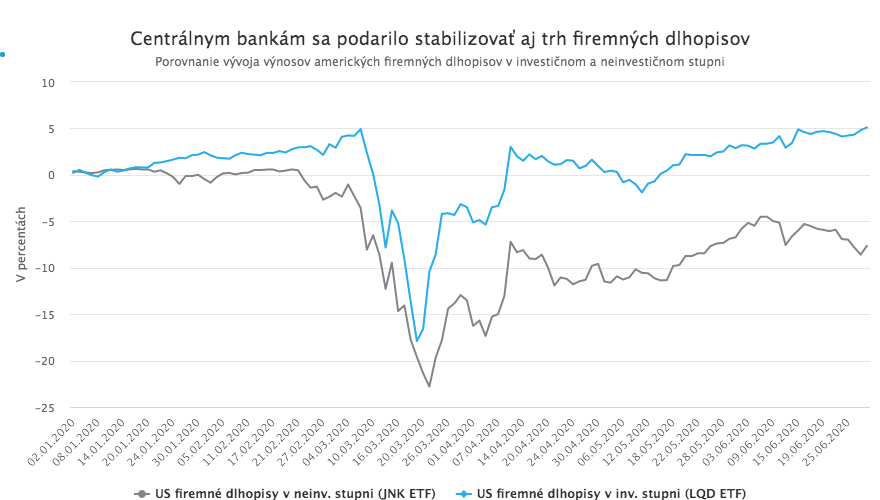

In addition to government bonds, central banks also managed to stabilize corporate bond markets quickly, even though the volumes of corporate bonds purchased were negligible compared with the scale of sovereign bond purchases. In practice, clear communication of intent was largely sufficient.

This is visible in the price performance of U.S. corporate bonds across both investment-grade and high-yield segments. Prices in both categories, particularly among higher-quality investment-grade bonds, largely normalized by the second half of March and early April. This happened despite the fact that the Fed did not begin actual purchases until May, and even then only in limited amounts. In other words, it was enough for the Fed to announce in March that it would also buy these instruments.

Central-bank purchases of corporate bonds, especially those below investment grade, naturally raise concerns about moral hazard. Still, it is hard to dispute that without intervention, many corners of the bond market would have remained effectively frozen, and many companies would have been unable to raise funds to withstand forced economic shutdowns. Alternatively, they might have been able to borrow only at prohibitively high interest rates, creating severe longer-term problems.

By stabilizing credit markets, central banks enabled companies to secure additional financing on favorable terms to bridge the crisis, and companies took full advantage of this opportunity. U.S. investment-grade issuers placed record volumes of bonds in April and May. By late May, they had already surpassed USD 1,000 billion (USD 1 trillion) in issuance, a level that in previous years, even in strong issuance cycles, was typically reached only toward year-end. As a result, 2020 is likely to be a record year for corporate bond issuance.

Of course, stabilization of the bond market does not mean that every company with access to capital markets will avoid bankruptcy or serious financial stress. In recent weeks, alongside the surge in new issuance, corporate bankruptcies have also risen sharply (though they have not yet reached levels seen during the previous crisis). This has been most visible among companies that entered the crisis with already high leverage and non-investment-grade ratings.

Oil rebounded, but remains well below early-year levels

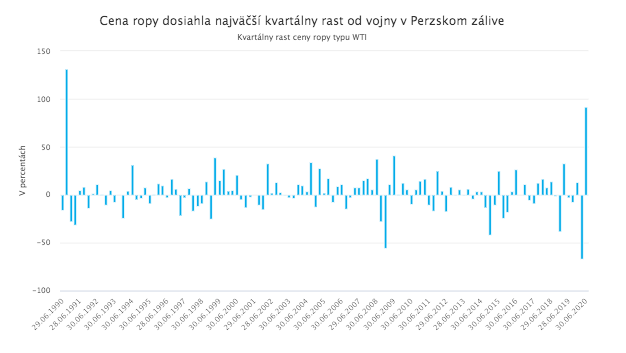

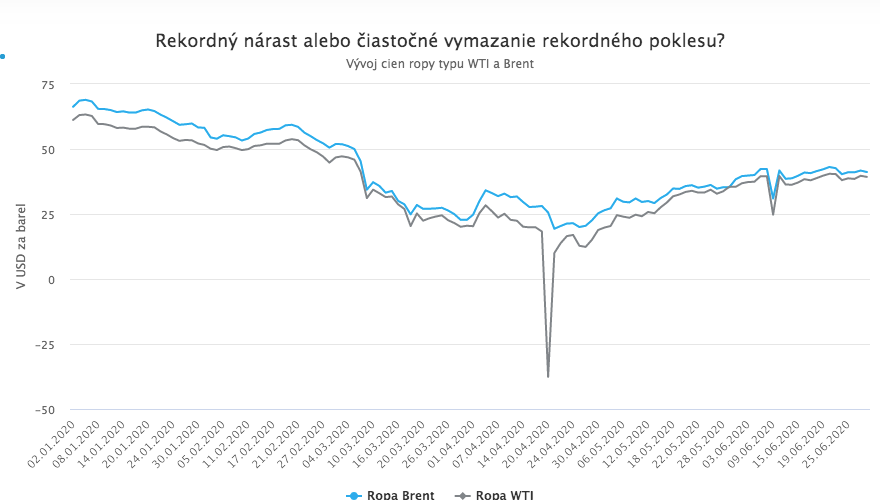

These figures sound somewhat less impressive once we consider that, despite the rally, oil prices remain far below their levels at the beginning of the year. The first-quarter collapse, driven by an exceptionally ill-timed combination of the pandemic shock and the onset of a price war between Russia and Saudi Arabia, was even more dramatic than the subsequent rebound.

The strong recovery in oil prices in the second quarter (in other words, the partial unwinding of first-quarter losses) was supported by a gradual return in demand, particularly from China, as well as the end of the brief Russia-Saudi price war and a renewed OPEC+ agreement to limit production.

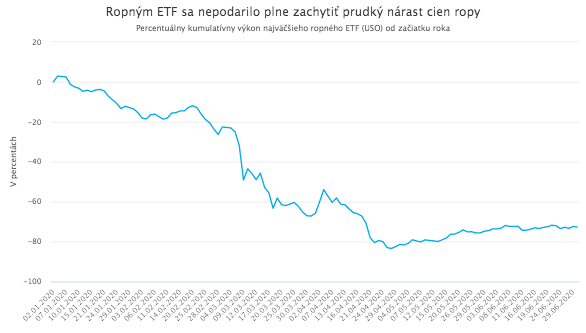

Incidentally, retail investors benefited far less from the oil rally than headline price moves might suggest. The reason was extreme contango, together with changes in futures-roll methodology prompted by fears of prices turning negative, which sharply reduced the potential gains of oil-focused ETF products.