Equities Kept Rallying Despite Rising Risks. What Awaits Them in 2022?

The current macroeconomic backdrop is far from ideal. Risks have been building, and equity markets were already trading at historically stretched valuations in the first half of the year. Yet in the second half they continued to grind sharply higher. What pushed equities to fresh highs? Can the rally extend further? What kind of year might 2022 be for stocks?

In the second half of the year, the macro environment was shaped by concerns over a sharp acceleration in inflation and uncertainty about the next steps of central banks, alongside growing risks from a slowing China and the early stages of an energy crunch. From the summer onward, investors were additionally unsettled by the notion (partly confirmed) that the pace of GDP growth, fiscal and monetary stimulus, and corporate earnings growth had already peaked.

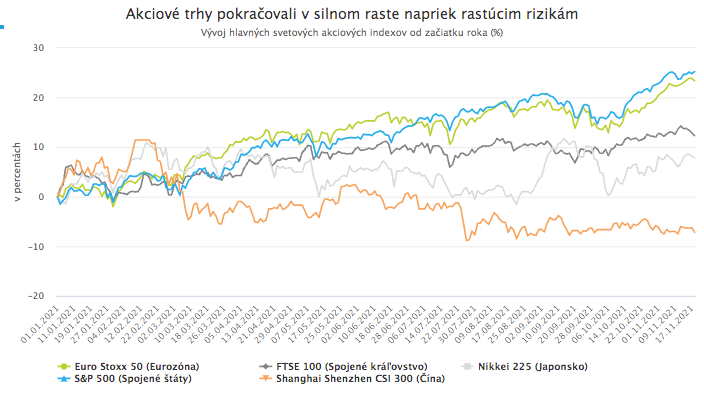

Despite this complicated backdrop, global equities continued to advance strongly through much of the second half. US and European stocks led the way, up more than 20% year-to-date. Japanese and UK equity markets also posted solid gains.

Among major equity markets, only Chinese stocks fell into negative territory this year, pressured primarily by aggressive regulatory intervention from Beijing.

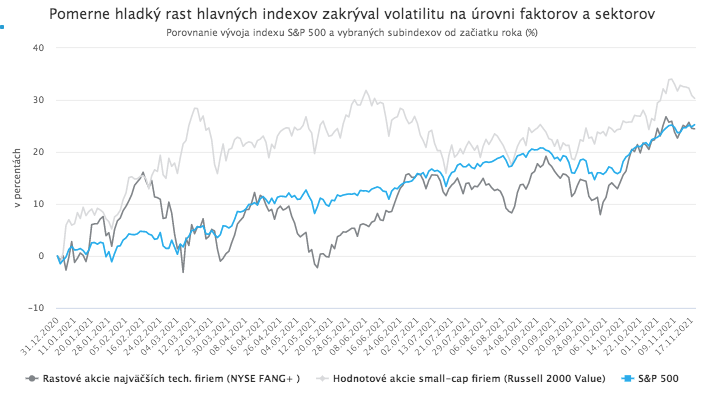

The steady, relatively smooth ascent of the main US and European indices in recent months masked significant volatility beneath the surface, at the level of styles, factors, and sectors, driven largely by shifting expectations around inflation and central bank policy.

In any case, the steep rise in headline indices over the past 20 months has heightened bubble concerns. But is the market truly in a bubble, or does the rally still rest on rational foundations?

The fundamental underpinnings of the equity rally

Equities have indeed been buoyed by speculative forces, and certain corners of the market look like outright irrational bubbles inflated by mania.

Even so, the strength of equity markets in the second half of this year cannot be dismissed as mere speculation. Despite the accumulation of macro risks, stocks have continued to benefit from supportive fundamentals.

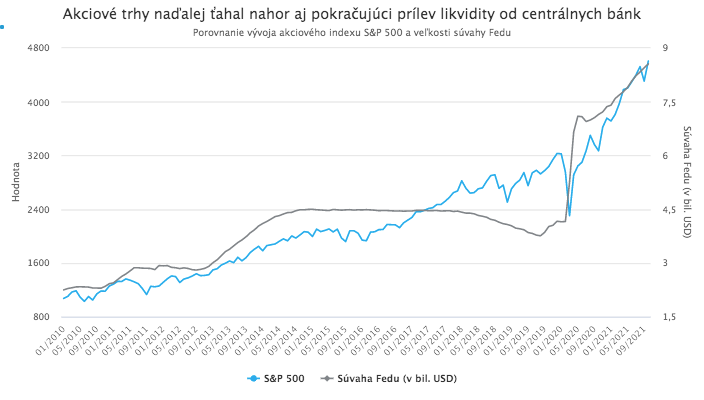

Key factors include the still-accommodative stance of major central banks, which are slowing asset purchases but are not yet preparing imminent rate hikes, the emergence of promising antiviral COVID-19 treatments from Pfizer and Merck, and, importantly, robust corporate earnings for the third quarter.

Companies in the S&P 500 delivered nearly 40% year-on-year net income growth in Q3 on average, and roughly two-thirds beat analyst expectations by more than one standard deviation. Particularly encouraging for investors is the fact that firms managed to protect margins even in a challenging environment characterized by supply-chain disruptions and rising input costs.

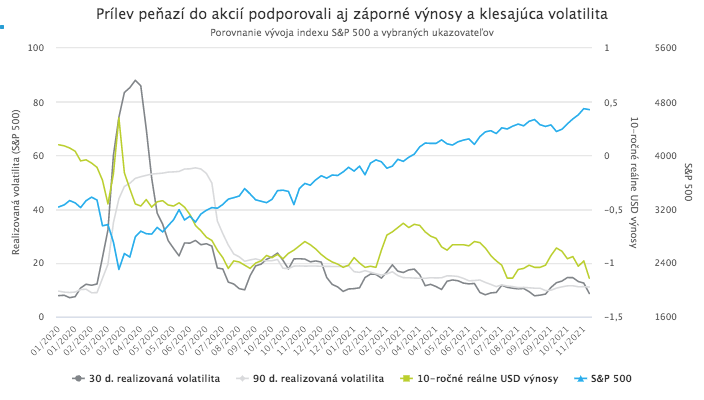

Equities have also been supported by declining realized volatility, which mechanically increases equity allocations among volatility-targeting strategies, as well as by extremely low real yields, which leave investors with limited alternatives. Dollar real yields hit a new all-time low in the first half of November at -1.17%. Against that backdrop, it is not surprising that inflows into global equity funds reached a record USD 900 billion this year.

Finally, interest rates in advanced economies remain near the lowest levels in 5,000 years, despite rising inflation. Meanwhile, asset purchases by major central banks are still ongoing, albeit at a slower pace. “Slower” nonetheless still means roughly USD 840 million per hour on average since the pandemic began.

Retail speculation is playing a growing role

It is true that, alongside these more “objective” drivers, speculative activity by retail investors has increasingly contributed to equity gains, a dynamic the Fed has recently flagged as a risk. Initially, this speculative impulse was concentrated in so-called “meme stocks”, popular among younger users of new trading apps who often have limited investing experience and coordinate activity on social media.

These investors learned that coordinated “pumping” could push meme names such as GameStop and AMC up by hundreds of percent within days, often without any rational justification. Several months ago, they even drove up shares of bankrupt Hertz, whose equity was effectively worthless, despite the company itself warning investors.

Over time, retail traders also learned to influence prices of large-cap stocks through a more sophisticated mechanism known as a “gamma squeeze,” or “weaponized gamma,” which we described in more detail in an earlier article. In essence, retail investors purchase large quantities of near-dated, out-of-the-money call options on mega-cap stocks. Dealers, in turn, must hedge by buying the underlying shares, reinforcing upward momentum.

This dynamic intensified markedly in November, affecting the largest US technology names and contributing to Tesla’s sharp rise, a stock particularly favored among retail investors. Single-stock call option volumes reached record highs, while the put-call ratio fell to a 20-year low.

Because these flows have pushed up the largest US technology companies, which now account for an exceptionally large share of major US and global equity indices, the broader indices have continued to rise alongside a small handful of mega-caps.

As a result, the S&P 500 keeps printing new highs and trades near record valuation levels, yet only 16% of its constituents are at 52-week highs. That is far below May’s readings, when the figure reached 45%. The rally is therefore standing on increasingly fragile foundations, driven by a shrinking set of names and amplified by retail-driven option mechanics.

Constructive conditions for further gains

The near-term macro outlook is highly uncertain. Beyond the familiar pandemic risk, markets are particularly concerned about the potential escalation of the energy crisis, the threat of a sharper slowdown in China, complex domestic political dynamics in the United States, and persistently rising inflation, which could force major central banks into more aggressive tightening.

If none of the extreme downside scenarios materialize, however, advanced-economy GDP could continue expanding at a solid pace broadly consistent with current forecasts, none of the looming crises would spiral out of control, and inflation could begin to normalize after a few more months of pressure without triggering an abrupt central bank response. Under such conditions, equities would retain reasonable fundamental support, reinforced by continued inflows from institutional and retail investors.

Authorized buybacks have reached a record level this year, exceeding USD 1 trillion. At the same time, money-market funds still hold roughly USD 5.5 trillion, about USD 1 trillion more than before the pandemic. That represents ample “dry powder” that could continue to fuel equity upside.

European and Japanese equity indices, moreover, may have a higher chance than they have had in a long time to outperform US equities. US benchmarks, given their heavy concentration in mega-cap technology, are structurally better suited to an environment of lower inflation, lower interest rates, and slower growth. The ECB and the Bank of Japan are also in less of a hurry to tighten policy than the Fed. Finally, by standard valuation metrics, European and Japanese equities are not as richly valued as US stocks today.