Commodities are breaking records

Chinese companies are also adding fuel to the fire, as they have received orders to build up large stockpiles of all essential raw materials needed for their operations. It is possible that most companies around the world have taken similar steps, and in doing so they are unknowingly driving raw material prices to new highs. Equity markets are in a similar situation: Germany’s DAX index has lost almost 20% since the start of the year, the EURO STOXX 50 about 19%, France’s CAC 40 around 17%, and the U.S. S&P 500 index more than 12%.

Oil, gas, and coal are at their historical highs

Brent and WTI prices approached USD 140 per barrel at the beginning of the week. Before tensions escalated, oil was trading at around USD 90. Black gold last reached its previous peak in 2008 at USD 150. After hitting that previous peak, oil literally collapsed and its price fell to around USD 40 per barrel. Even today, black gold is not being driven by extremely strong demand or a critical shortage. It is more about confusion, and therefore once the chaos ends, a major correction may follow. Price stabilization will also be supported by OPEC, which will increase production by another 400,000 barrels per day from April. The IEA is not sleeping either; its members released 60 million barrels of oil from strategic reserves. The price of natural gas in Europe was around EUR 70 per MWh before fear surged. After tensions intensified, it reached nearly EUR 350, a historic maximum. Gas from Russia has continued to flow even after the conflict began, and in some cases in even higher volumes. The price therefore mainly reflects panic in the market rather than a dramatic shortage of the commodity. The primary cause is investors who fear how far the conflict could go, and they are pricing in a total disruption of supplies from Moscow. Coal is no exception, and its price has already risen by more than 300%. In this case, it is preparation for a gas shortage, since coal is used to generate electricity and would be an alternative to electricity produced from gas. Germany uses this approach to a large extent, as it decided to reduce emissions by producing electricity from gas. On the other hand, Germans have developed an extreme dependence on Russian gas. The whole of Eastern Europe has a similar lack of freedom, and change is absolutely necessary in today’s situation. The EU must become far more energy self-sufficient and diversify energy sources in order to ensure strategic independence. In addition, Russia is threatening the EU that if it cuts off oil imports, Moscow will shut down the Nord Stream 1 pipeline that runs to Germany. That would hit the economic core of the Union. A complete ban on imports of Russian oil is something only a country like the U.S. can afford, since Russian oil accounts for only about 3% of its consumption and it also does not need to import gas. The United Kingdom reached a similar decision, but it will reduce imports gradually and end them over the course of this year. EU leaders unanimously agreed to reduce dependence on Russian energy, and this year gas transport from the Russian Federation is to be cut by two-thirds. The ambitious plan also includes ending imports of natural gas from the Kremlin by 2030. Renewables and gas supplies from the U.S. and Qatar are expected to help achieve this.

Fear is driving up commodity prices for industry and food production

Looking at commodities needed for industry, the strongest gains were recorded by nickel, steel, and aluminum. Since the start of the year, nickel has become more expensive by more than 142%, aluminum by nearly 45%, and steel has risen by around 31%. Russia is a significant producer of these metals, but it is neither the only nor the dominant player in the market. By contrast, the Russian Federation and Ukraine are the world’s most important exporters of wheat. This commodity has responded to the current situation with higher prices and has gained almost 69% since January. Soybeans also rose at a solid pace, by 27%, and corn by 24%.

Will Russia cut us off, or will we cut it off?

A scenario in which Russia would cut the West off from oil and gas is unlikely. The largest country in the world would lose its most important source of income and foreign currency. The probability that the West will cut itself off is higher, but that option would also significantly damage the EU economy. Of course, Moscow would be hurt far more by such a cutoff. However, at this time it does not make sense to damage the Russian economy at any cost. Instead, reasonable and targeted measures should be used to minimize losses for allies. The main problem for the EU is gas, which is not easy to replace in the short term. In the long term, we can handle this obstacle as well and adapt to it. Without Russian gas, the EU should survive the next winter with alternative sources, but Moscow will not survive until the next winter without our money. Putin has not yet decided to cut the West off from his commodities because he is well aware of the damage such a step would cause. Russia is in an extremely difficult situation and is literally bleeding economically. Some analysts predict a decline in the Russian economy of about 30%, which would be a bigger drop than during the Great Depression.

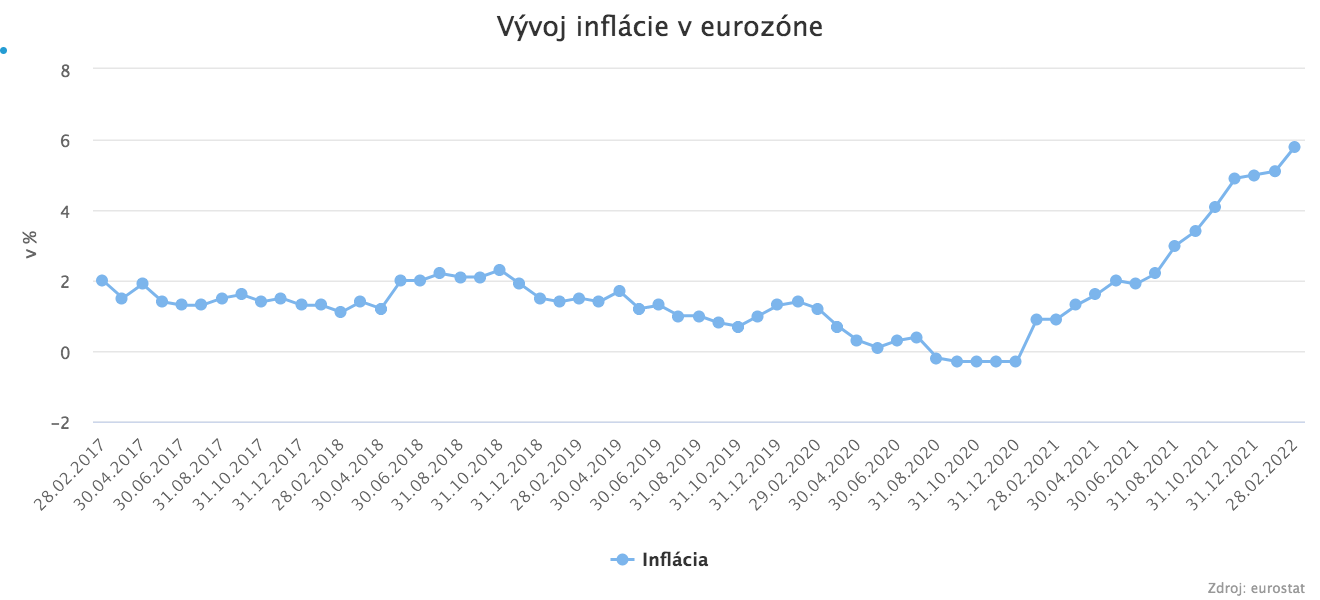

Inflation will continue to rise

The world will have to wait for the expected decline in inflation, and the EU even more so. Today’s extremely expensive commodity prices will feed into every corner of the economy, and the price level in the EU could approach 10%. Slovaks must prepare for inflation above 10%. A similar situation awaits the other V4 countries, which will be hurt not only by expensive commodities but also by a weaker currency. Real inflation deceleration will probably only be observed toward the end of this year. Original forecasts expected prices to slow during the summer months.