Fear Is Creeping Back Into Markets Again. Stocks Fell the Most Since March.

After months of optimistic gains fueled by a powerful mix of monetary and fiscal stimulus, fear is creeping back into markets. Virtually all riskier assets, including equities, have suffered their biggest losses since March. Is a second wave of major market panic arriving along with the second wave of coronavirus?

In recent months, financial markets have steadily risen, even though the end of the pandemic and the problems it has caused in the real economy are still nowhere in sight. Stock markets reached new highs, risky bonds quickly forgot the March sell-off and enjoyed record investor demand, emerging-market currencies stabilized, and the U.S. dollar, traditionally the safest asset, weakened to multi-year lows. It seems, however, that the trend is beginning to reverse again.

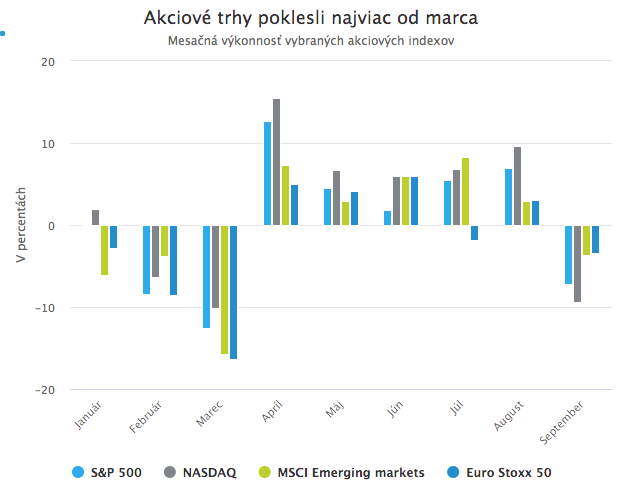

Virtually all assets that performed well in recent months suffered significant losses in September. Meanwhile, the assets that performed best during the peak of market panic are starting to rise again.

A black September for U.S. tech stocks

Perhaps nowhere is this reversal more visible than in U.S. technology stocks. They recovered from the March sell-off at rocket speed and kept rising sharply in the months that followed, reaching new highs practically every week. Their rise seemed unstoppable.

Then September arrived. In its first days, markets saw brief but sharp drops driven mainly by technical factors and excessive speculation. Tech stocks were not immune to such pullbacks in the past either. What is unusual, however, is that they were unable to shake them off over the course of the month. On the contrary, they added further losses.

It appears that this September will be their worst month since 2008. The NASDAQ index, with a large share of tech companies, has even posted bigger losses this month than it did in March of this year, when pandemic-driven market panic peaked. Moreover, the most popular NASDAQ-tracking ETF recorded on Monday the largest one-day outflow of funds in two decades, as much as USD 3.5 billion.

But it is not only tech stocks, and not only U.S. stocks, that are struggling. As the previous chart shows, the U.S. benchmark S&P 500, which is somewhat more broadly diversified by sector than the NASDAQ, is also on track for its first monthly decline since March. European equities and emerging-market equities are also heading for their largest monthly declines since March.

Worrying moves are visible everywhere

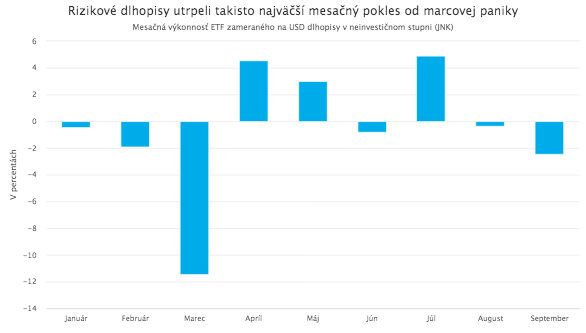

An even more ominous sign is that September’s declines are not limited to equities. They have also spread to bond and currency markets, where cracks are now appearing as well. These cracks are disrupting the apparent calm of recent months and suggest we may be heading into rougher times again.

High-yield (“non-investment-grade”) bonds also suffered their biggest decline since the March panic, despite the fact that the Fed continues to buy them. The most popular ETF tracking these bonds recorded on Monday its largest one-day outflow since February, USD 1.06 billion. Weekly outflows reached USD 4.22 billion, the third-largest weekly outflow this year.

Aethon United, a company monitoring developments in the market, even decided this week to postpone a planned bond issuance worth USD 700 million, underscoring the worrying developments in the high-yield segment. This is the first larger canceled issuance since early July. Safe bonds, traditionally sought in times of rising risk, are enjoying increased investor demand despite record-low yields. Yield curves in developed-country bond markets fell again this week, especially at longer maturities (so-called bull flattening).

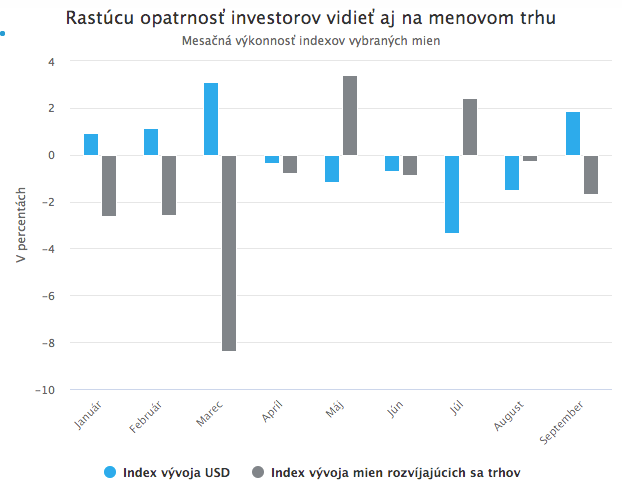

Developments in currency markets also clearly point to growing caution among investors. The U.S. dollar, which traditionally strengthens in times of rising risk and market turbulence, strengthened in September for the first time since March. Another “safe haven” in FX markets, the Japanese yen, also performed well.

Riskier currencies of smaller and emerging countries, by contrast, weakened sharply this month, again the most since March. The euro also weakened; however, currencies of other European countries outside the eurozone weakened even more sharply. The weakening of the Hungarian forint even pushed Hungary’s central bank to raise its policy rate unexpectedly on Thursday. On the same day, Turkey’s central bank took a similar step in an attempt to stop the decline of the lira.

The sharp strengthening of the dollar and simultaneous weakening of riskier currencies not only reflects rising investor fears, but also reinforces them in return, since such a situation always deepens problems and imbalances in the global economy.

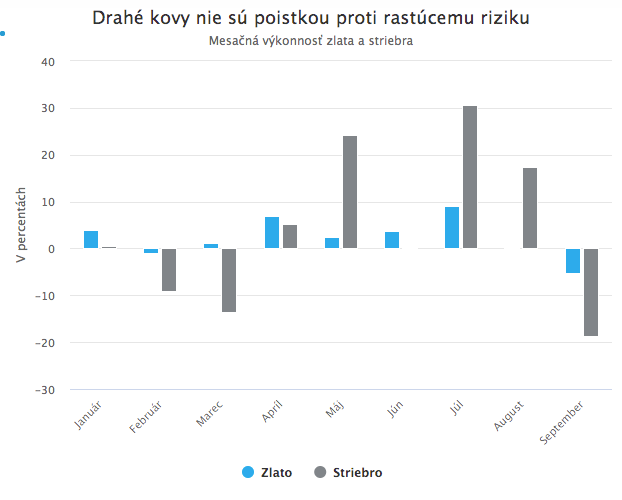

By the way, current market developments are further evidence of something we have warned about before: gold and precious metals in general are not, by themselves, a “safe haven” or “insurance against risk.” Despite rising risks, both gold and silver posted their first decline since March this month. They reacted in a more or less mechanical way to a strengthening dollar and rising real dollar yields. Those two factors have a much stronger influence on their price than overall risk sentiment.

The only true “safe haven” in times of rising risk and market turbulence therefore remains the U.S. dollar (and, to a lesser extent, the Japanese yen and the Swiss franc).

A second wave of market panic?

Does this worrying market development mean that, together with the second wave of the pandemic, a devastating second wave of market panic similar to March is also arriving? Or is this just a short, temporary correction, a necessary breather after months of overly optimistic gains?

To answer this question, we first need to look at the causes of September’s troubling moves. U.S. technology stocks experienced their first problems already at the beginning of the month. As mentioned, however, that initial decline was caused mainly by technical factors and did not, by itself, signal a shift in market sentiment, nor did it spill over into other markets.

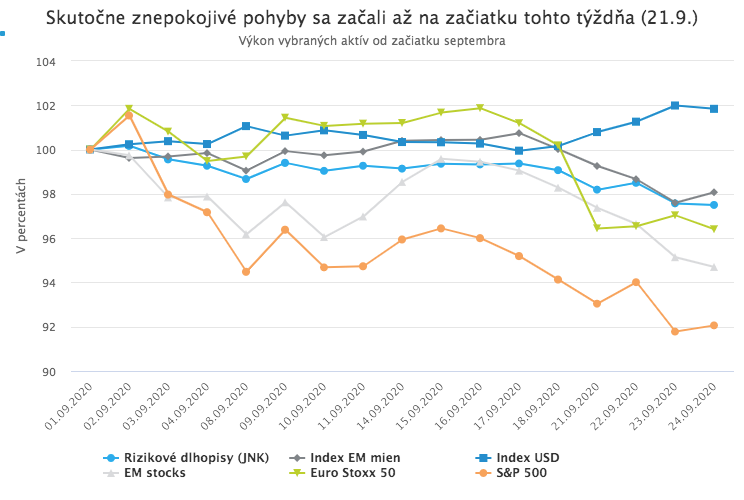

Truly worrying moves began only at the start of this week (21 September). On Monday, all major equity markets started to fall, while at the same time the dollar strengthened sharply and riskier bonds, along with smaller and riskier currencies, began to weaken significantly. These moves were a reaction to a combination of risk factors that, by coincidence, escalated on the very same day, creating a “perfect storm” that has been raging in markets for a week. At the center of this storm are current problems on the U.S. political scene, which were sharply intensified over the weekend by the death of Supreme Court Justice Ruth Bader Ginsburg.

From the standpoint of political developments, her death came at the worst possible time: the presidential election is approaching and negotiations on another economic relief package are still stalled. Republicans led by Trump announced that they want to appoint their nominee to the vacant seat and want to do so before the November election (even though many of them had previously repeatedly ruled this out, and even the late justice had expressed the wish that her successor be chosen only after the election).

Democrats sharply criticize this plan, since “Trump’s people” would thereby gain a clear majority on the Supreme Court at a time when there is a real risk that the outcome of the November election will be decided by the Supreme Court. This development not only increases the risk of election unrest and controversy, but also reduces the chances that Democrats and Republicans will finally agree on another desperately needed support package for the U.S. economy and the population affected by the coronavirus crisis, a package markets have been expecting for a long time.

Even if this factor alone might have been enough to unsettle markets, additional factors were added on Monday: the reintroduction of coronavirus restrictions in the United Kingdom, which amplified fears that similar steps would follow in other major economies, and the “FinCEN Files” scandal, which pushed down the shares of the world’s largest banks.

Over the course of the week, this storm was further fueled by other factors such as weak data from European economies and the U.S. labor market, worrying growth in new coronavirus cases around the world, rather pessimistic comments by Fed Chair J. Powell, and Trump’s unwillingness to promise a peaceful transfer of power in the event of an election loss.

Winter is coming

September’s return of fear to markets thus has two main causes: uncertainty linked to the approaching U.S. election, and concerns that the pandemic (and its economic impact) is not yet being overcome. It is clear that neither of these risks will disappear on its own. Uncertainty about the U.S. election and a peaceful transfer of power can only dissipate once these events play out. Fears of a strengthening pandemic can likely be dispelled only by the successful development of a vaccine.

From the perspective of both risks, the next quarter will be crucial. The election will take place in November (the definitive result is expected only in December), and around that time we should also have more clarity about the next phase of the pandemic. Both events can turn out very badly (a destructive pandemic wave with no vaccine and a disputed U.S. election accompanied by violence) or very well (a successful vaccine and a peaceful transfer of power to a president with an economy-supporting agenda). Given the nature of these scenarios, it is practically impossible to reliably estimate the probability of their realization.

The only certainty is that we can definitively forget the calm that prevailed in markets during the summer months. Winter is coming. The fourth quarter will be wild and volatile.