Beneath the surface of market moves: Whales and gamma loops

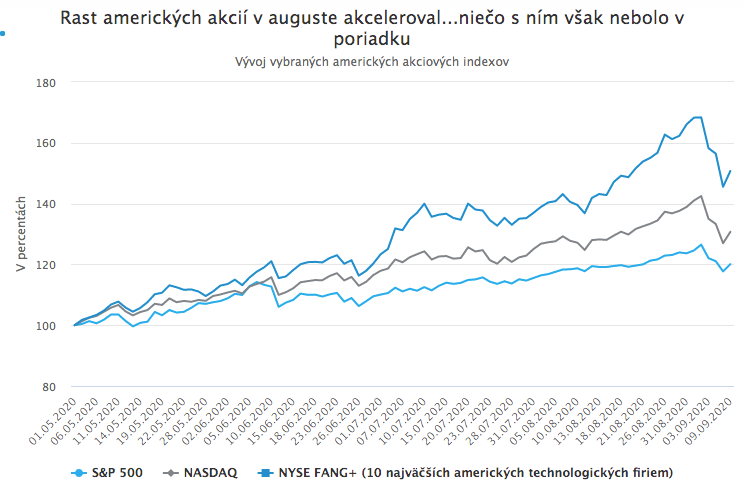

U.S. stock markets, driven higher mainly by technology stocks, have been rising almost continuously since April. In August, however, the rally accelerated even further. The indices surged sharply, and shares of some technology companies experienced a truly parabolic rise.

However, quantitative analysts (“quants”) at major investment banks warned that something was off about the August rally, that it looked unnatural, and that a short but sharp correction could be expected in the coming days. One of them was Charlie McElligott, one of the leading quant analysts at Japan’s Nomura. As early as the morning of 3 September, before markets opened, he published a note warning that Nasdaq was facing an imminent one-day drop of roughly 6% to 8%. Nasdaq did in fact turn negative that day and finished with a loss of more than 5%. The benchmark S&P 500 fell by 3.5%. Declines continued for several more days.

So what pushed markets sharply higher in August and then pulled them sharply lower at the start of September? And how is it possible that top quant analysts predicted it with relatively high accuracy? The media wrote that markets rose in August “due to better-than-expected economic data and hope for a Covid vaccine”, while they fell sharply in September “due to bad economic data”. The reality, however, is different, more complicated, and more interesting.

Traces in market data

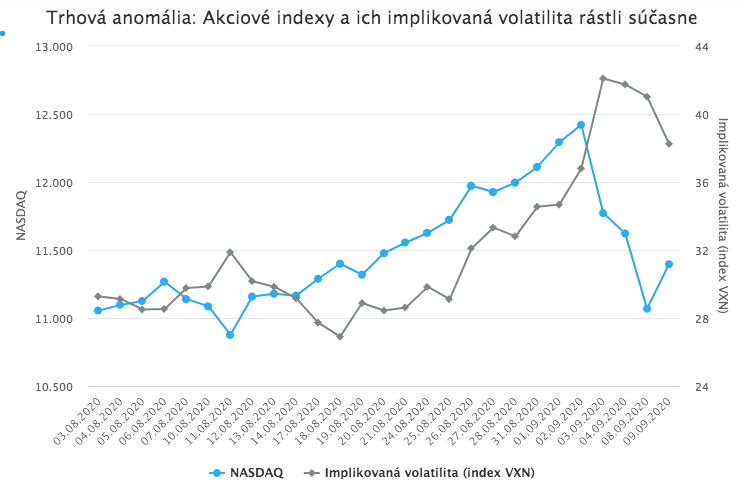

As in many other areas of life, unusual activity in markets leaves traces. That was the case here as well. Signs that something was wrong with the August rally appeared in market data. The most visible anomaly accompanying the sharp August rise was the simultaneous increase in implied volatility. Historically, this is a very rare phenomenon. Indices measuring implied volatility, calculated from option prices on the relevant asset, almost always rise sharply during market declines and, conversely, fall when markets rise. This is why they are often referred to as “fear indices.”

Yet this time they were rising even as the market was going up. This pointed to unusual activity in the options market. A closer look at the options data indeed showed an exceptionally sharp increase in call option volume on the shares of the largest technology companies, which today carry a dominant weight in U.S. equity indices. Call options give investors the right to buy a selected stock by a specified future date at a price set in the option contract. The investor must pay an option premium for this right. It is therefore a bet on a further rise in the stock price. Compared with buying the stock outright, however, it has the advantage that in an adverse scenario the investor does not risk losing the entire principal, but only the paid option premium.

Option dealer hedging

The sharp rise in the prices of precisely those technology stocks for which call option volumes surged suggested what was likely happening in the market. A key role was played by so-called “gamma hedging” by options dealers. In short, every call option that an investor buys has to be written by someone. The writer receives the option premium and becomes the counterparty to the contract. If the price of the underlying stock rises above the strike price agreed in the option contract, the call option holder profits, while the writer loses. The largest Wall Street investment banks, acting as market makers, also serve as options dealers. This means that when investors want to buy call options, these banks write the options for them in exchange for a premium.

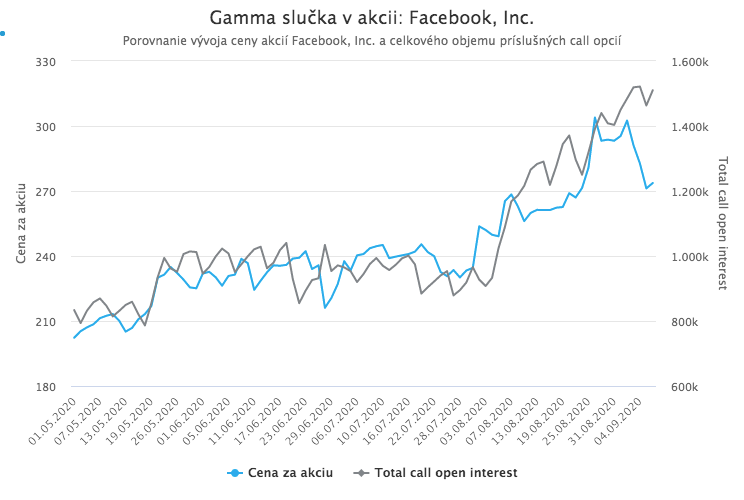

Because they do not want to speculate on market direction, but rather earn fees and the bid-ask spread with minimal risk, they always hedge their options exposure. If, for example, an investor buys a large amount of call options on Facebook shares and the stock begins to rise, the investor will profit and the options dealer will incur a loss. To protect against this risk (hedge), the dealer buys the underlying asset itself, namely Facebook shares. That means that if the share price rises, the dealer earns a profit on the stock while simultaneously recording a loss on the written call option. Ideally, these gains and losses offset each other.

The gamma loop

So if someone buys a large amount of relatively near-dated call options on a particular stock, the options dealer must also buy a large volume of the shares on which those options were written in order to minimize its own risk. However, these purchases also push the stock price higher, which increases the potential losses on the written call options, and therefore forces the dealer to buy even more underlying shares. In a mutually reinforcing feedback loop, this pushes the price even higher.

Put more technically, when the aggregate gamma of options dealers is negative, they hedge their options exposure in the direction of the market, thereby amplifying market moves and increasing volatility. (When, by contrast, dealers’ aggregate gamma is positive, they hedge against the direction of the market, dampening market moves and lowering volatility, creating a so-called gamma trap.) Everything suggests that in August markets entered exactly such a “gamma” loop, where the buying of large quantities of call options on certain technology stocks forced options dealers to buy those same stocks as part of their hedging, pushing prices higher and increasing the value of the call options written on them. Writing an enormous volume of call options on certain stocks thus became a kind of self-fulfilling prophecy.

The problem with such a gamma loop, however, is that it works in both directions. If, due to additional external factors or sooner or later simply under its own weight, this mechanism breaks down and the price of the underlying stocks starts to fall, dealers’ “gamma hedging” amplifies market moves downward as well. This leads to a sudden and sharp market drop, exactly like the one seen at the beginning of September.

The volatility loop

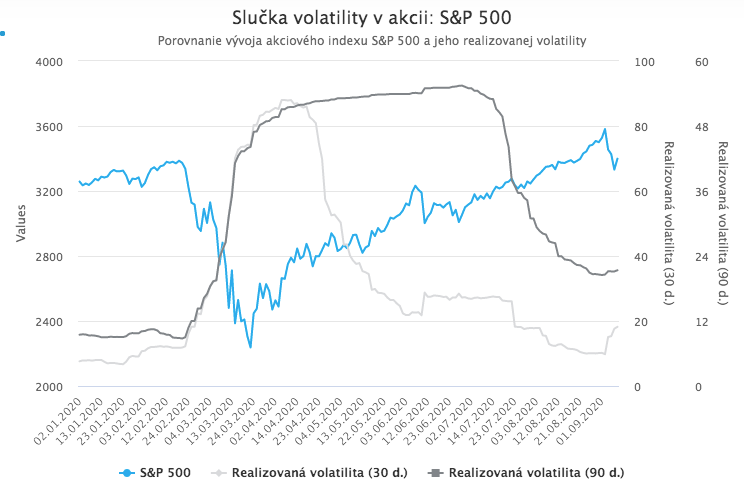

Modern market infrastructure also means that price moves triggered by a gamma loop can, in some cases, be further amplified by another similar mechanism driven by market volatility. Among the most popular investment strategies used by large funds today are so-called “vol control” or “vol target” strategies. Their goal is to keep the overall portfolio’s volatility within a pre-set range. This means that when market volatility starts to rise, funds following this strategy automatically sell the more volatile components of the portfolio, such as equities, in order to keep overall volatility within the targeted range. Conversely, when market volatility declines, these funds automatically buy.

The result is another feedback loop that amplifies existing moves. When markets rise, volatility typically falls, and these funds, controlling hundreds of billions, buy more, pushing markets further up and dampening volatility. Conversely, when markets fall and volatility rises, they automatically sell large volumes, deepening market declines and simultaneously increasing volatility. This volatility loop was also at work during the August market rally and the subsequent sharp sell-off at the start of September, further amplifying the effects of the gamma loop.

The sharp rise in the shares of the largest technology companies at the beginning of August led to a decline in the correlation between the rapidly surging technology sector and the stagnating shares of other sectors. This, in turn, reduced the realized volatility of equity indices (in contrast to rising implied volatility). The subsequent decline in realized volatility then triggered automatic buying by vol control funds, pushing markets even higher. When technology stocks fell sharply at the beginning of September and volatility rose, these funds began selling, which deepened the sell-off.

The whale unmasked

It can therefore be argued that the strong August rally and the subsequent sharp drop in technology stocks (and with them the broader market, due to their large market capitalization and index weight) was to a significant extent driven by the purchase of a large volume of call options on these stocks at the start of August. The situation is even more interesting because, according to market rumors, these massive call option purchases were made by a single large buyer. Traders began referring to this mysterious large investor as the “Nasdaq whale”. The Financial Times revealed the identity of the Nasdaq whale on 4 September: Japan’s SoftBank Group.

During August, SoftBank bought call options on the largest U.S. technology companies such as Apple, Amazon, Facebook, Tesla, Netflix, and others for USD 4 billion, with total notional exposure of up to USD 30 billion. Unlike index options, the options market for individual stocks is not accustomed to such large one-off volumes, especially in the middle of summer when overall market liquidity is typically weaker. The whale’s large purchases also attracted additional investors, who copied the whale’s positions and opened call options on the same stocks, further distorting the market.

It is entirely possible, however, that the whale merely jumped with a big splash onto a wave that had already been set in motion by small retail investors months earlier. According to Bloomberg, these investors had already recognized the potential of the gamma loop and have been more or less successfully spinning it up in selected technology stocks for several months. The whale simply took it to another level.