Turkey in a Currency Crisis Again

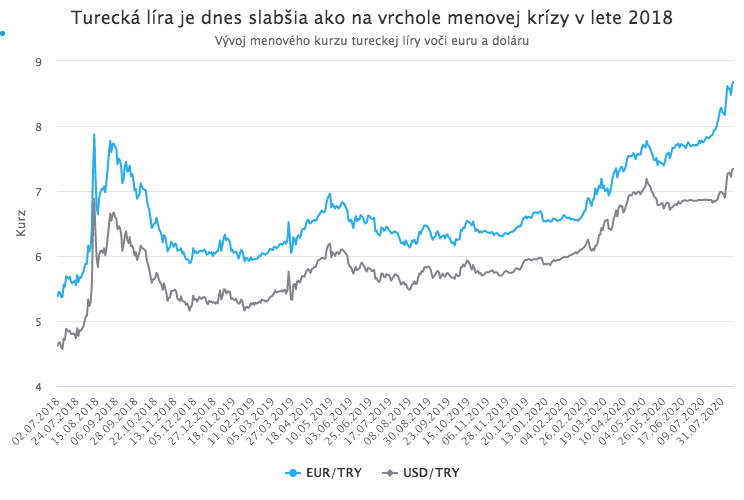

In one of our previous articles from mid-May we warned that Turkey was at risk of a currency crisis. Today, unfortunately, it seems that the risk has already turned into reality. The persistent weakening of the lira in recent weeks has accelerated and pushed the Turkish currency to its weakest level on record. Against the euro it has fallen by more than 22% since January, and against the dollar it has lost a full fifth of its value. The lira is now weaker than it was at the peak of the currency crisis in the summer of 2018.

The immediate trigger for this depreciation was the coronavirus pandemic, which deepened economic problems worldwide and led to capital outflows from riskier markets. The deeper causes of the crisis, however, lie primarily in long-standing economic and political problems in Turkey that make the lira one of the most vulnerable emerging-market currencies, highly sensitive to external shocks. The economic impact of the pandemic, the largest external shock in modern history, therefore hit the lira far harder than many other currencies.

Incompatible goals

The main source of instability in the Turkish economy is the combination of constant stimulus through credit expansion and a high need for external financing. President Erdogan has long sought to achieve economic growth faster than Turkey’s real economic capacity by continuously encouraging private-sector borrowing. One negative consequence of this economic model is, of course, persistently high inflation. High inflation naturally creates pressure for the currency to weaken. That is a problem because Turkey, given its persistent current-account deficit and private-sector debt denominated in foreign currencies, needs a stable exchange rate and an inflow of foreign capital. But a stable exchange rate cannot be maintained over the long term with high inflation. Reducing inflation, meanwhile, generally cannot be achieved without raising interest rates. And high growth stimulated by credit expansion cannot be achieved with high interest rates and without generating inflation. A currency weakening due to high inflation combined with relatively low interest rates, however, triggers capital outflows from the country rather than inflows, further amplifying depreciation. Under this style of economic policy, recurring currency crises are inevitable. The last such crisis occurred in the summer of 2018, when the lira fell by almost 40% in just a few weeks. The central bank eventually managed to stop the collapse and stabilize the currency by sharply raising interest rates, which halted the rise in inflation and restored investor confidence.

The road to trouble

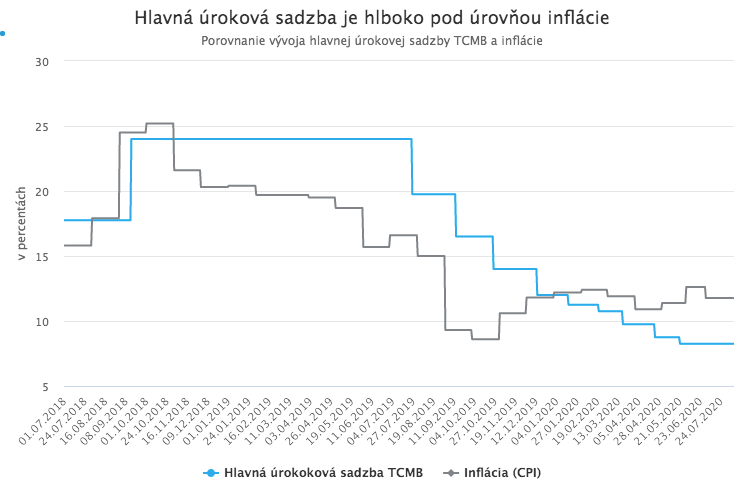

President Erdogan, however, clearly did not learn from that episode. Immediately after the crisis was contained, he began demanding significant rate cuts from the central bank governor, and when the governor did not comply, he replaced him with the more loyal Murat Uysal. Upon taking office, Uysal began cutting rates quickly as the president wished. At the same time, credit expansion resumed. In less than a year, Governor Uysal cut the main policy rate by a record 15.75 percentage points, from 24% to today’s 8.25%.

At first, these rate cuts were not a problem, because gradually declining inflation created some room to lower rates, supported by monetary easing from major global central banks. But when inflation (unsurprisingly) stopped falling after a while, Uysal continued cutting rates. As can be seen in the chart below, even before the pandemic broke out, the main policy rate had already dropped below the inflation rate. That meant the real interest rate fell below zero.

When the coronavirus pandemic then hit and central banks around the world began slashing rates and injecting billions to rescue their economies, Turkey’s central bank found itself in a difficult position. It had already cut rates to an unreasonable level months earlier, and double-digit inflation fueled by cheap credit left it little room to safely pump additional billions into the economy.

Nevertheless, after the pandemic began, the central bank implemented further rate cuts and credit expansion gained momentum. The volume of new loans rose by as much as 40% over the last three months. Inflation is therefore not falling even in the face of the massive deflationary shock of the pandemic, and the main policy rate now stands as much as 3.5 percentage points below inflation. Such a deeply negative real interest rate, one of the lowest in the world, is driving foreign capital out of lira-denominated investments, since even far safer investments in euro- or dollar-denominated government bonds offer a higher real return today.

Add to these problems a sharp drop in FX revenues due to stagnant tourism and Erdogan’s continuing geopolitical “adventures” (most recently a maritime conflict with Greece), and the current rapid weakening of the lira is hardly surprising.

How to stop the lira’s fall without angering Erdogan

The central bank is, of course, trying to stop the lira’s slide. But its options are limited, because the simplest and most effective tool for stabilizing the currency, raising interest rates, cannot be used. In the midst of an economic crisis, such a move would carry risks; more importantly, it would run into Erdogan’s opposition. Even today he still speaks about lowering rates, calls interest “the mother and father of all evil,” and according to his, diplomatically speaking, unorthodox economic theories, lowering interest rates leads to lower inflation, not the other way around.

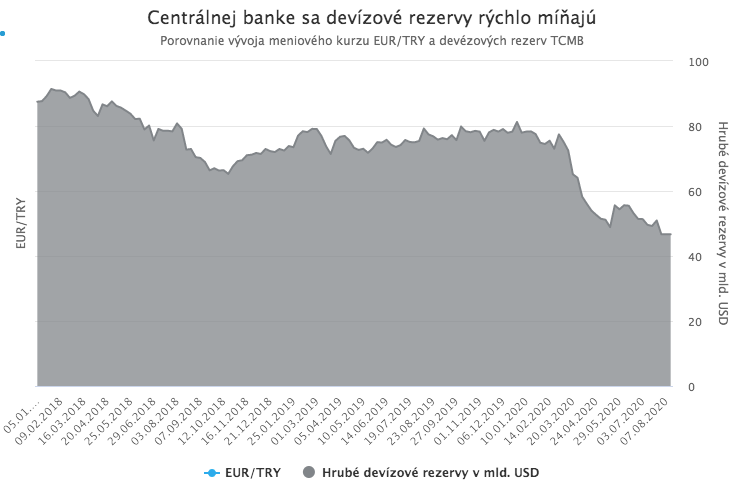

Turkey’s central bank (TCMB) is therefore trying to support the lira mainly through FX interventions. But as the chart below shows, its foreign-exchange reserves are being depleted quickly and it has little “ammunition” left. If we adjust the current level of TCMB reserves for liabilities from currency swaps, the result is a negative number.

The central bank’s depleted ammunition has, of course, not escaped investors’ attention and is further increasing pressure on the lira. Turkey also tried to secure additional foreign-currency resources via swap lines, but the most important global central banks rejected its requests. The likely reason was Erdogan’s aforementioned taste for geopolitical adventures. Only Qatar accommodated Turkey, tripling the size of an existing swap line; however, that volume (USD 15 billion) is not sufficient.

Meanwhile, Erdogan’s administration is also experimenting with capital restrictions, with mixed results. Such measures can help reduce speculative pressure on the lira, but they also deter potentially beneficial investment. The lira, meanwhile, continues to fall at a dangerously rapid pace.

The central bank therefore has to come up with something else to support the currency, and whatever it proposes must be approved by Erdogan. That is not an easy task, since there are not many options left besides raising interest rates.

In recent days, the bank has attempted to effectively raise rates without formally increasing the main policy rate. The main policy rate remains at 8.25%, but the amount of liquidity the bank provides at that rate has fallen to zero. The interest rate at the one-month repo auction, which in practice has now replaced the main one-week repo auctions, climbed as high as 10.96% on Thursday. This clever workaround may help ease pressure on the lira in the short term, but it is unlikely to stop the longer-term decline. In the end, Erdogan may have no other choice than to resort to the hated rate hikes or face a free fall in the lira.