Inflation in the Eurozone Continues to Rise. The ECB Is Not Changing Policy Yet.

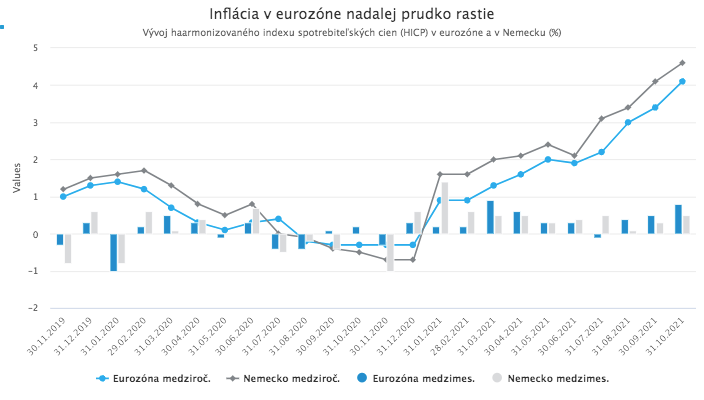

Inflation in the eurozone continues to rise rapidly. According to Eurostat’s preliminary estimate, it increased in October to as high as 4.1%. It is therefore not surprising that inflation was the main topic of the ECB’s October meeting. ECB President Christine Lagarde admitted after the meeting that the period of elevated inflation will last longer than the bank originally expected; however, she expects price pressures to ease over the course of next year. The ECB is therefore not changing its policy for now.

The ECB’s October meeting was closely watched. It came at a time when several major central banks responded to rising inflation with unexpectedly rapid monetary tightening, triggering sharp moves in money and bond markets.

Inflation leads central banks to change policy

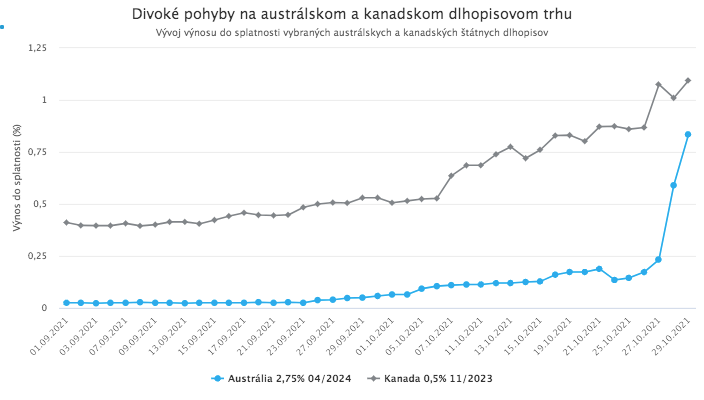

In addition to the Bank of England, the Reserve Bank of New Zealand, and Norges Bank, which we wrote about last week, the Canadian and Australian central banks also joined in shortly before the ECB meeting. The Bank of Canada announced on Wednesday an abrupt end to quantitative easing and signaled future rate hikes, citing persistently rising inflation. Markets reacted sharply to this unexpected decision. The front end of the Canadian yield curve recorded a move equivalent to 15 standard deviations.

Similarly dramatic moves occurred in the Australian market after quarterly data released on Wednesday pointed to a surprisingly rapid rise in inflation in the country. This led investors to expect that the Reserve Bank of Australia would also soon raise rates, even though it had not previously signaled such a step.

The Australian central bank, which had been implementing yield curve control, indirectly confirmed these expectations when it then refused to “defend” the target yield level. Yields on 3-year bonds jumped within a few hours to eight times the targeted level.

The European Central Bank is now facing a situation similar to that of the central banks mentioned above. Inflation in the eurozone is rising quickly and persistently. In September it climbed to 3.4% year-on-year, and in October it reached as high as 4.1% according to Eurostat’s preliminary estimate, the highest reading since July 2008. In previous months, however, the ECB had insisted that this rise in inflation is only temporary and therefore does not require any tightening of monetary policy.

Nevertheless, given the actions of other central banks, investors in recent weeks began to expect that the ECB would also take steps toward tightening its extremely accommodative monetary policy in response to rising inflation, even though it had so far rejected such a move. Ahead of the October meeting, the euro money market reflected expectations that the ECB would raise the deposit rate by 20 basis points by the end of 2022.

Investors therefore watched closely on Thursday to see whether the ECB would change its rhetoric in light of rising eurozone inflation and announce, or at least hint at, possible future tightening.

Higher and more persistent, but still only temporary

At the press conference after the meeting, ECB President Christine Lagarde acknowledged that inflation was indeed the central, and practically the only, topic: “We talked about inflation, inflation and inflation.” She also admitted that inflation would continue to rise over the remainder of this year and that the current period of higher inflation will last longer than the bank had originally expected. Despite that, the ECB did not announce any tightening at the October meeting, as it does not yet see a reason to do so.

After further thorough analysis, the bank continues to argue that the current rise in inflation is driven primarily by three factors that are temporary in nature and will fade within a few months. These are the sharp increase in energy prices (this component accounted for as much as half of last month’s price rise), the rebound in demand associated with reopening economies after the pandemic, and base effects related to the reinstatement of VAT in the euro area’s largest economy.

The ECB expects price pressures, after a few more months of growth, to ease over the course of next year as these three factors weaken. According to the bank, inflation will therefore remain below its symmetric 2% target over the medium term. Since the ECB targets 2% inflation over the medium term, this means it currently sees no reason to tighten monetary policy by raising interest rates:

“In order to support its symmetric inflation target of 2% and in line with its monetary policy strategy, the Governing Council expects the key ECB interest rates to remain at their present or lower levels until it sees inflation reaching 2% well ahead of the end of its projection horizon and durably for the rest of the projection horizon, and it judges that realized progress in underlying inflation is sufficiently advanced to be consistent with inflation stabilizing at 2% over the medium term. This may also imply a transitory period in which inflation is moderately above target.”

During the subsequent press conference, Lagarde stressed that, based on the ECB’s analysis, the conditions for raising rates would still not be met in the second half of next year. The Governing Council also decided, citing favorable market and financing conditions, that the ECB would continue net asset purchases under the PEPP program at a moderately slower pace, as it did last month, than in the second and third quarters of this year.

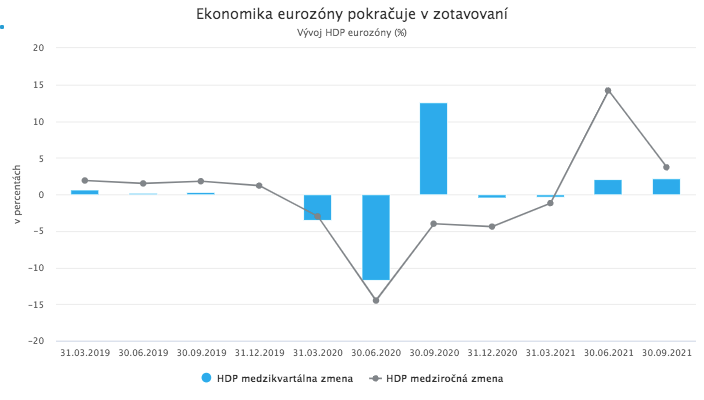

According to the ECB, the economic outlook remains favorable and the eurozone economy continued to recover strongly in the third quarter despite some moderation in growth. GDP figures published the next day confirmed the bank’s view. The eurozone economy is expected to return to pre-pandemic levels by the end of the year.

Investors still expect rate hikes

Thus, at its October meeting, the ECB acknowledged that price pressures are stronger and more persistent than it originally expected; however, it still views them as temporary and expects them to weaken next year. It therefore did not implement any unexpected tightening and emphasized that it currently sees no reason for such a step.

Market moves after the meeting, however, suggest that investors continue to expect the ECB to tighten monetary policy soon.

At the post-meeting press conference, Lagarde did not use several opportunities to explicitly rule out a rate increase next year and also declined to comment on money-market moves signaling expectations that the ECB would raise rates by 0.2% over the course of next year. She said it is not her role to comment on market moves and expectations.

Investors, accustomed in recent years to being “guided by the hand” by central banks and parsing every word from Lagarde, interpreted her comments, or the lack of them, as meaning that earlier monetary tightening by the ECB is still on the table. This interpretation is not necessarily correct. It may also have been an attempt by Lagarde to give the ECB a bit more independence from markets and greater operational flexibility in a highly uncertain macroeconomic environment.

In recent years, investors have grown used to central banks, including the ECB, effectively consulting markets on every step and signaling every policy change far in advance in order to avoid any sharp market moves. Today’s dynamic macroeconomic environment, characterized by hard-to-predict inflation developments and other risks that cannot be forecast precisely, requires central banks to remain flexible and to prioritize macroeconomic risks over the risk of heightened volatility in financial markets.

In any case, money markets after the meeting continue to point to expected ECB rate hikes of 15 to 20 basis points in the second half of next year. Eurozone bond yields rose in line with these expectations, the yield curve continued to flatten, and the euro strengthened quite noticeably.

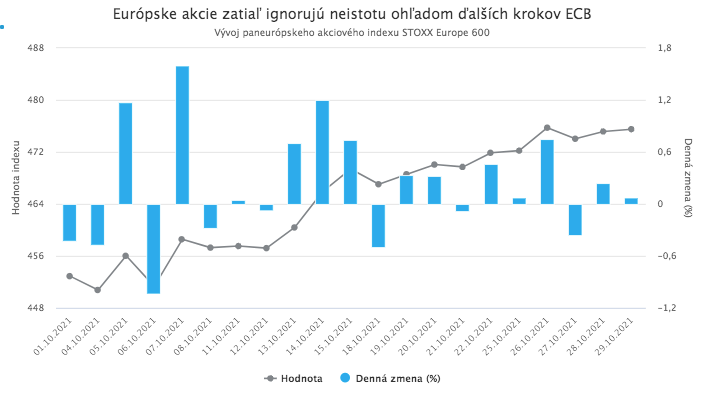

European equities rose this month despite persistently rising inflation and some uncertainty around monetary policy. The ECB meeting did not change that.

European equities, like U.S. equities, are currently benefiting mainly from a renewed systematic reallocation after a volatile September, continued inflows (inflows into global equities have reached a record USD 839 billion year-to-date; in the past week they totaled USD 28.1 billion), and strong corporate earnings. Of those European companies that have already reported third-quarter results, as many as two-thirds delivered earnings per share above expectations.