Oil is rising, technology stocks are falling.

Oil has had a truly wild 12 months. The outbreak of the pandemic, combined with an extremely ill-timed price war between Russia and Saudi Arabia, pulled it sharply lower a year ago. Within a few weeks, its price fell by as much as 70%. Eleven months ago, WTI crude was even briefly less than worthless and traded at negative prices. The end of the Russia–Saudi price war, a coordinated drastic reduction in production by the reconciled oil cartel, and a partial easing of panic subsequently helped stabilize prices around USD 40 per barrel.

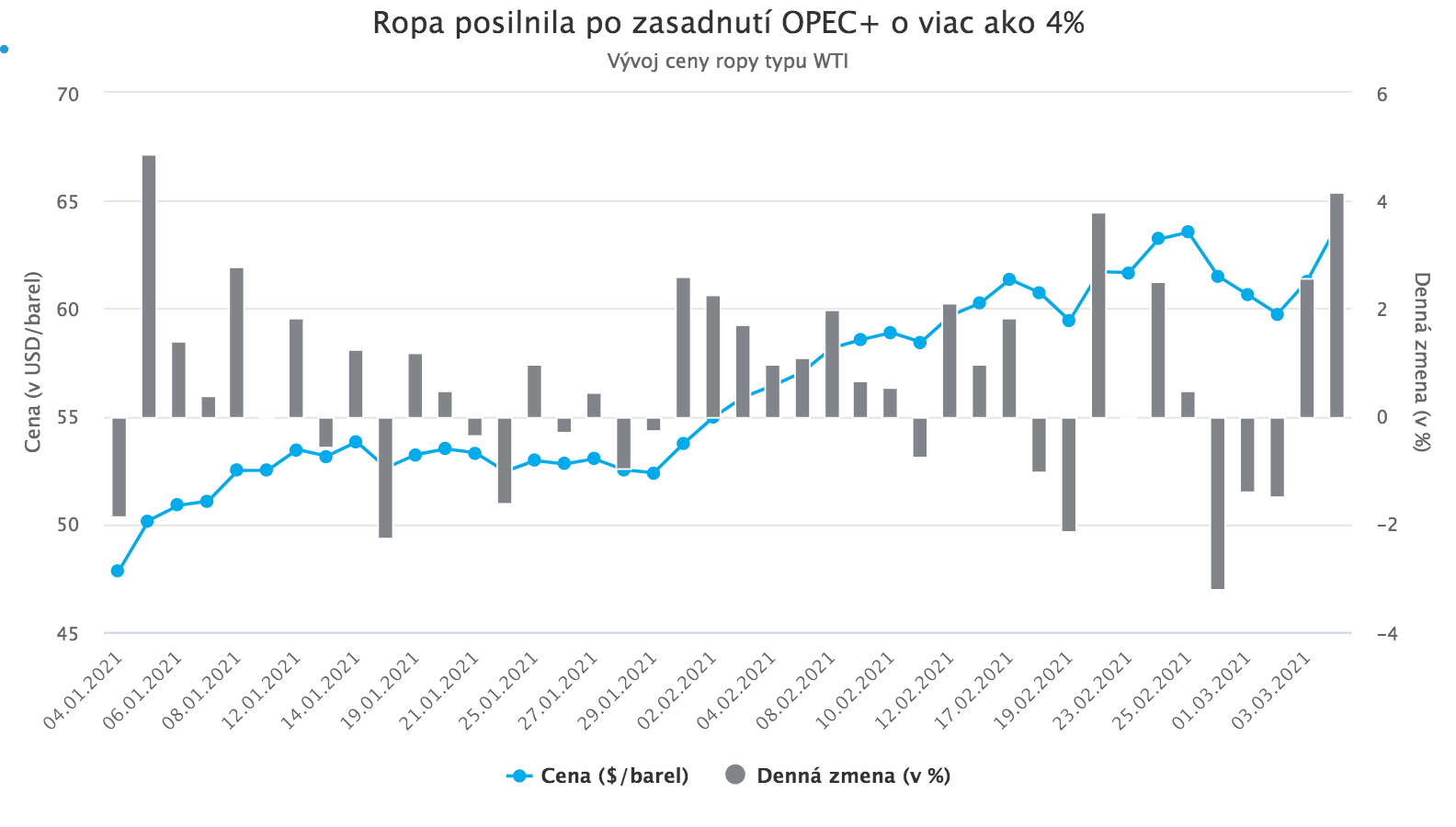

In November, however, oil began to rise sharply, and this strong uptrend has persisted to the present. It was triggered by the announcement of the first coronavirus vaccine, which brought hope for a recovery in the global economy and thus for rising demand for oil. These optimistic expectations were subsequently partly realized and continued to drive oil prices higher. This week, oil was additionally supported by an OPEC+ meeting, after which it rose by more than 4%.

OPEC+ surprises: no production increase despite rising demand

At the meeting held on Thursday, March 4, under Saudi Arabia’s leadership, OPEC+ countries decided not to increase oil production despite rising demand for the commodity. This means that production restrictions adopted by the cartel in the middle of the pandemic remain in force, aimed at balancing supply with the sharply reduced demand. Originally, this was a cut of up to 9.7 million barrels per day, later reduced to 7.7 million and finally to 7.2 million from January. In addition, Saudi Arabia adopted a unilateral production cut of a further 1 million barrels per day in January.

Given ongoing vaccination and the beginning of an economic recovery boosting oil demand, it was expected that the oil cartel would reduce current production restrictions and increase output from the following month by at least 1.5 million barrels per day. Analysts also expected Saudi Arabia to scale back or completely abandon its additional unilateral production cut.

However, OPEC+ surprised everyone and did not implement any broad-based increase in production. Saudi Arabia also kept its additional production cut in place. Only Russia and Kazakhstan received a small exception and may increase daily production by 130 thousand and 20 thousand barrels, respectively. Prince Abdul Aziz bin Salman, Saudi Arabia’s energy minister who led the meeting, urged cartel members to be cautious and warned that despite improvements the situation remains uncertain and increasing production could prove premature: “Let us make sure first that the light we see ahead is not the light of an oncoming train.”

OPEC+’s decision not to increase production will likely result in at least a short-term demand surplus over supply. Stockpiles will decline in the coming weeks and prices will rise. In anticipation of this, oil prices shot sharply higher immediately after the cartel’s decision was announced. WTI crude gained more than 4% and climbed to around USD 67 per barrel. “Black gold” thus returned this week to pre-pandemic levels, almost exactly on the first anniversary of the start of the brief and extremely ill-timed price war between Russia and Saudi Arabia.

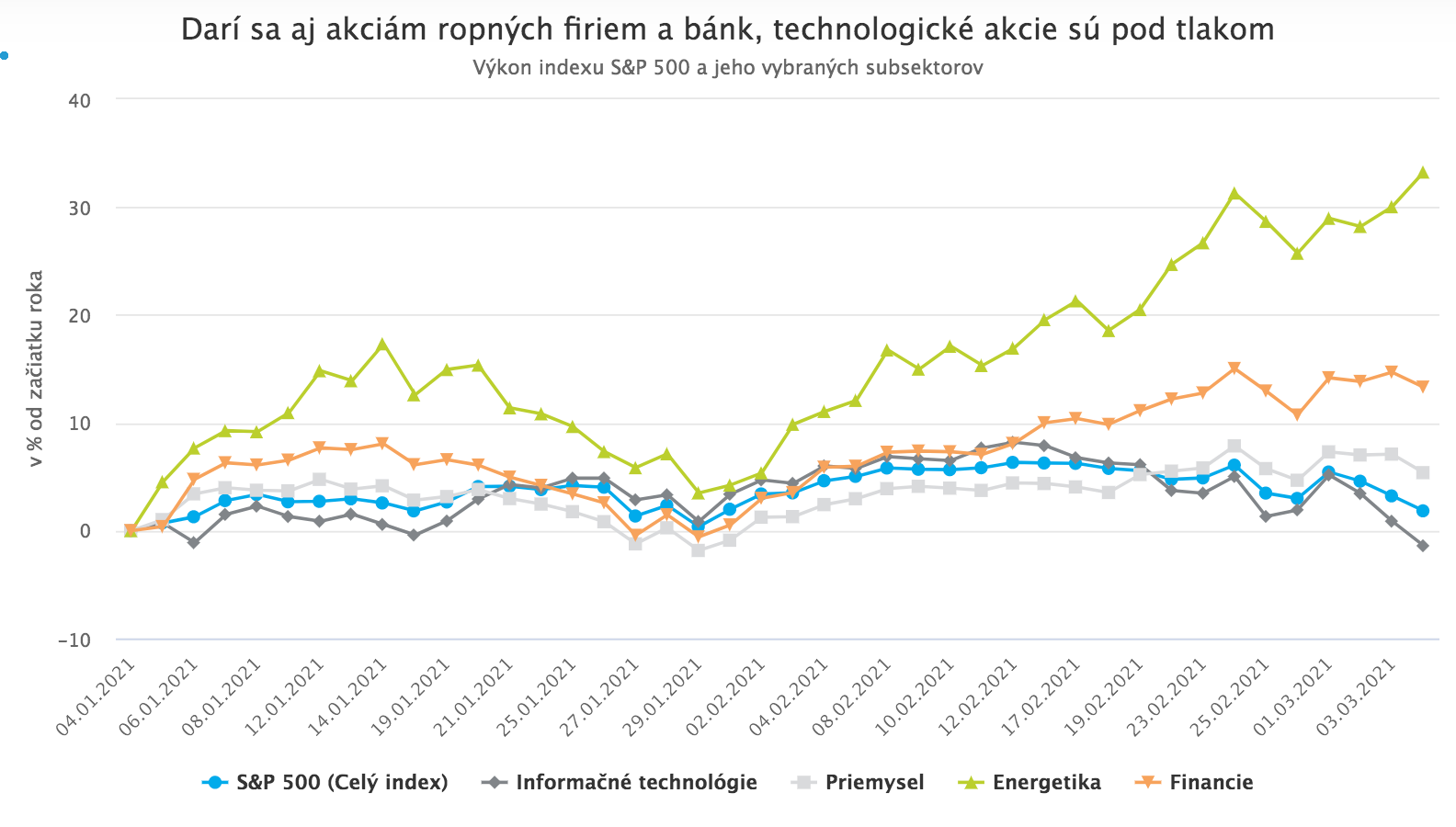

Shares of energy companies and banks are rising, while tech stocks are falling

Along with oil prices, shares of oil companies and the entire energy sector continue to rise sharply. Companies in the S&P 500 energy sub-index have risen by an incredible 33% on average since the start of the year.

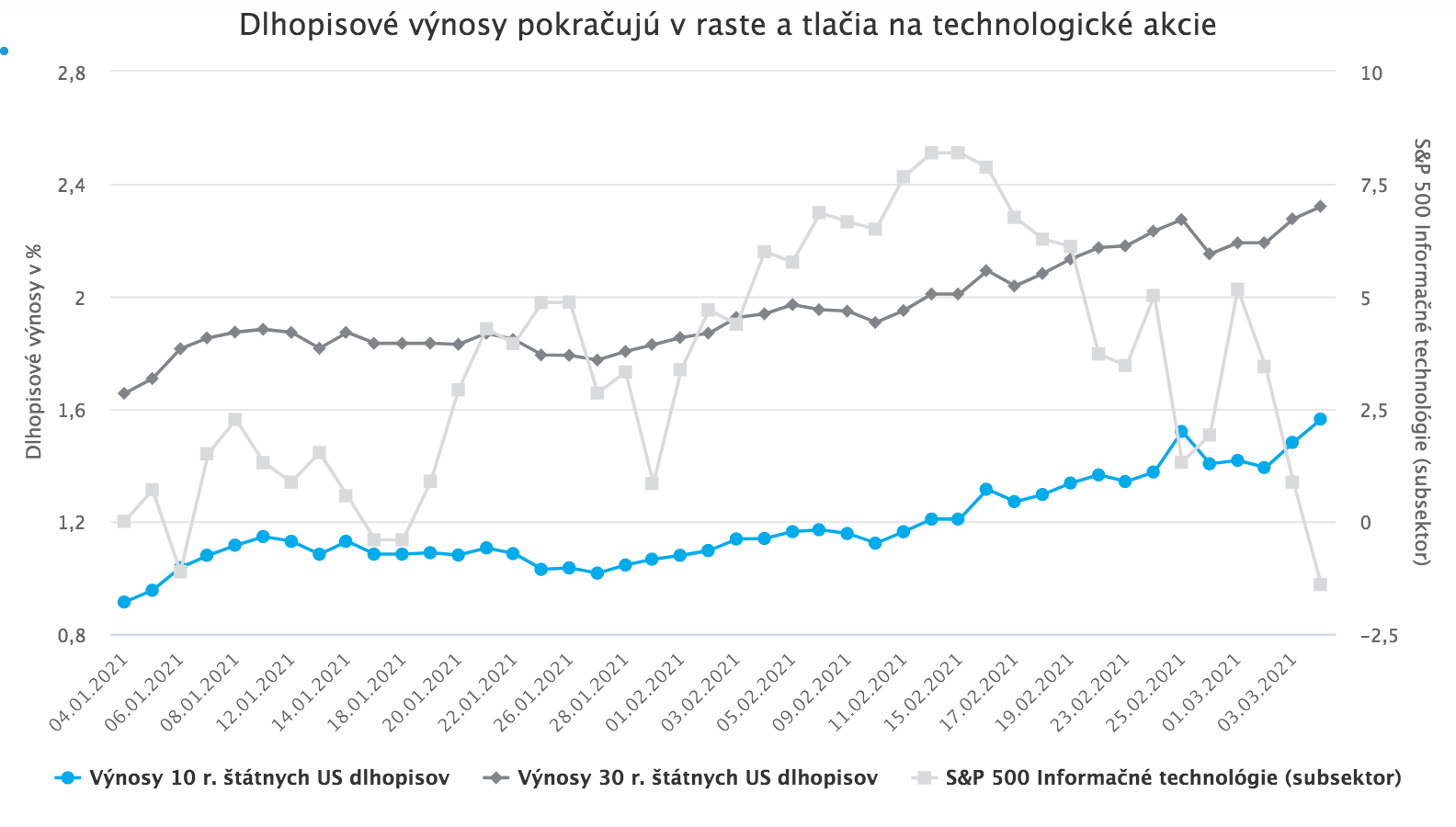

Bank and insurance stocks are also performing well. They are being lifted by rising US bond yields, which, like rising oil prices, are a result of optimistic expectations about the recovery of the global economy. A steepening yield curve typically helps banks improve net interest margins, which have recently been under pressure due to record-low rates and yields. Higher yields also help banks, and especially insurers, generate sufficient returns on assets to cover long-term liabilities.

However, rising yields have a negative impact on other sectors. The worst effect is on shares of large technology companies, which performed best in an environment of falling interest rates and sluggish growth. The shutdown of economies due to the coronavirus and the shift of many activities to the online world also supported their sharp rise for most of last year.

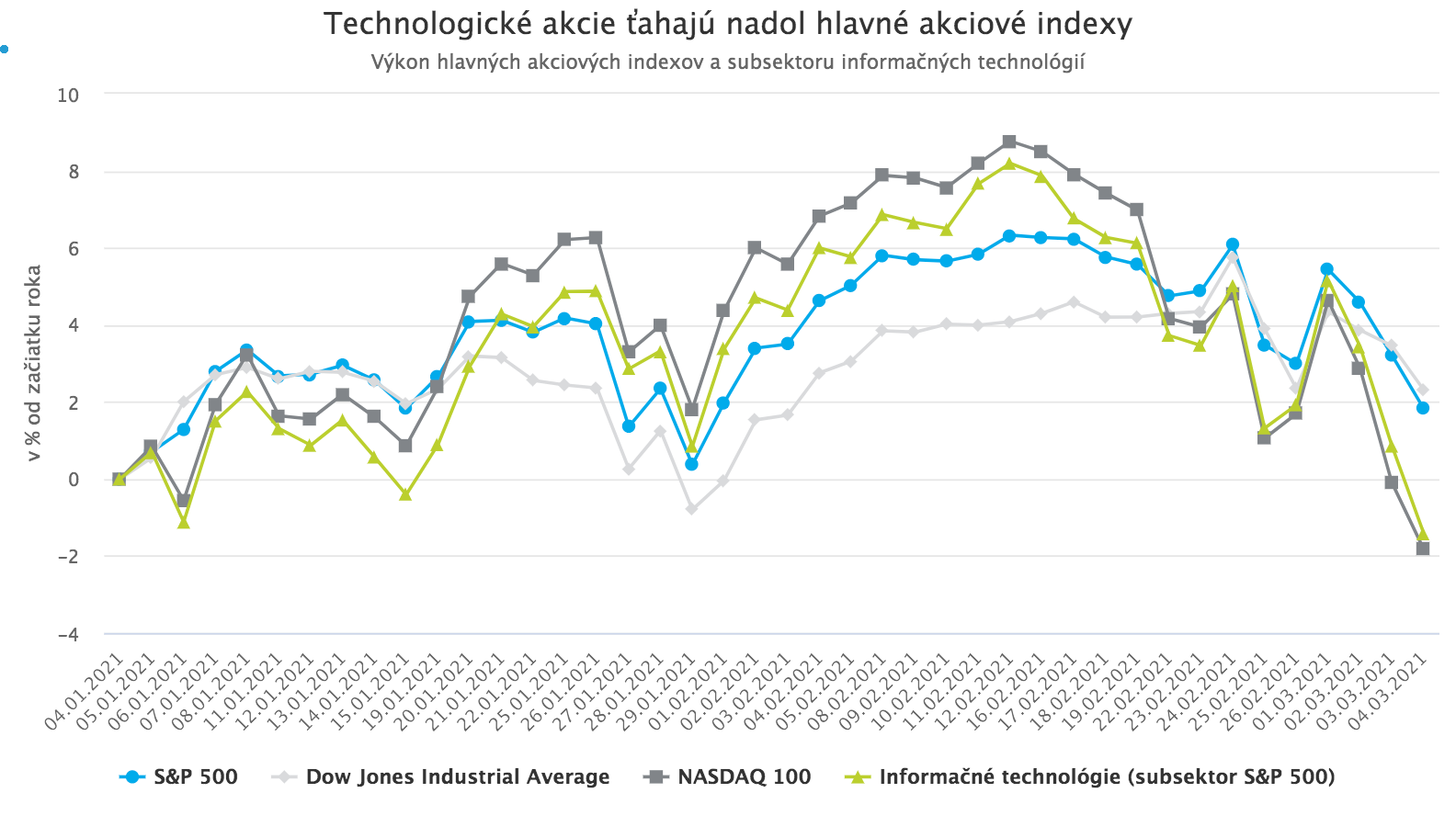

It is therefore no surprise that when the situation turned around, yields started to rise, many economies began reopening and recovering, and the shares of the largest technology companies came under pressure. Because these companies have a high weight in the main global equity indices, it has the effect that, superficially, “the whole stock market” appears to be falling in recent days. In reality, however, the main global equity indices have been dragged down in recent weeks mainly by technology companies, and the indices where tech stocks have the largest weight have therefore fallen the most.

The performance of the three major US equity indices clearly illustrates this. The biggest losses in recent weeks have been suffered by the NASDAQ, where the five largest technology companies account for more than 40% of the index. By contrast, the Dow Jones Industrial Average has performed relatively best, as it is more focused on industrial companies and technology stocks make up only a small share of it.

The benchmark S&P 500, with the five largest technology companies accounting for almost a quarter of its weight, is somewhere in the middle in terms of performance. More than 50% of its decline over the past week was driven by just five technology companies (Apple, Microsoft, Amazon.com, Tesla, and Nvidia).

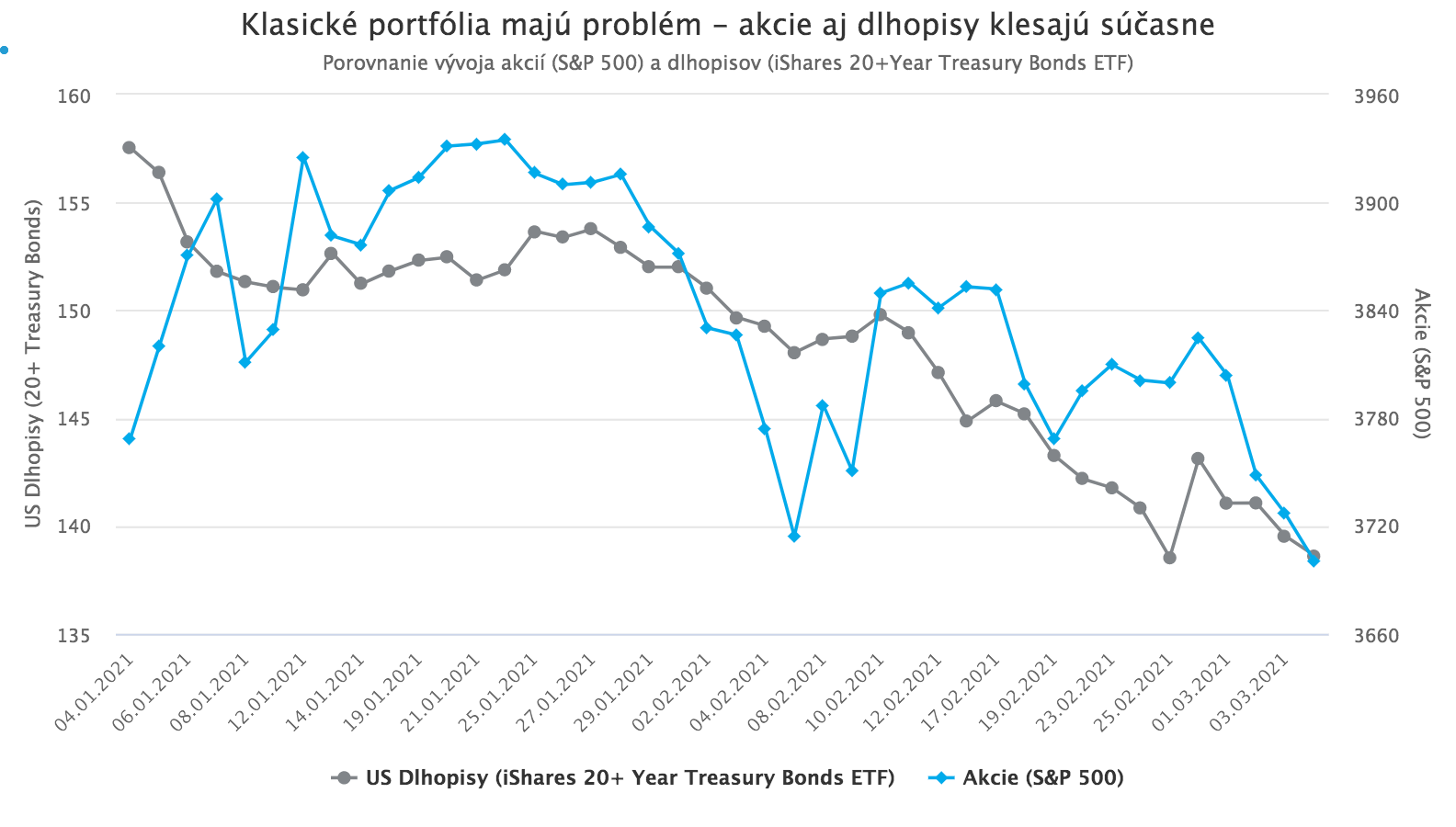

Traditional portfolios have a problem

Because of this dynamic, rising (especially US) bond yields are becoming a problem for the entire equity market. Their positive impact on financial stocks, and partly also on commodity-related companies, is simply not enough to offset their negative impact on technology firms, which currently have the largest weight in the major equity indices. The stock market has thus entered a peculiar situation in which the economy is beginning to recover, pushing yields higher, and those higher yields in turn push equity indices lower.

The current simultaneous decline in stock prices and US Treasuries (remember that rising yields mean falling prices) is a problem for traditional portfolios composed of a mix of an equity component, usually represented by the S&P 500, and a bond component consisting largely of US Treasuries. Historically, there has been a mildly negative correlation between the two components, stocks and bonds. This means that when constructing such a portfolio, it is assumed that any decline in equities will be at least partly offset by rising bond prices, and any decline in bond prices will in turn be offset by gains in the equity component.

But when both components fall at the same time, this basic building-block assumption of the entire portfolio no longer holds. Volatility increases, and performance suffers.

At present, pressure on the US Fed is increasing to slow the rise in US Treasury yields. Jerome Powell, the Fed Chair, had a good opportunity on Thursday to calm the markets. It would have been enough to vaguely suggest that the Fed is considering using its tools to curb bond yields if they continue to weigh on the stock market. However, Jerome Powell did not take that option. He did note that the Fed is aware of rising yields, but he also emphasized that it does not yet view them as a problem and reminded markets that during an economic recovery after a crisis, some short-term increase in inflation should be expected.

As a result, US Treasury yields rose by a few more basis points again on Thursday, and technology stocks dragged down the major equity indices. If yields continue to rise further, however, the Fed will have no choice but to intervene so as not to jeopardize the economic recovery.