Record Volumes of Negative-Yield Bonds Push Returns Below Zero

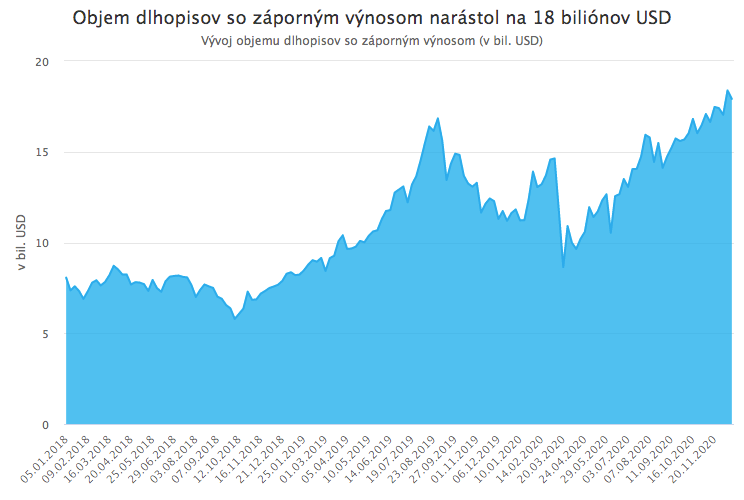

The outstanding stock of bonds trading at negative yields climbed to a record USD 18 trillion toward year-end. This implies that nearly one-fifth of all bonds globally now offer a yield below zero. What has driven this unusual situation, and what are its implications?

Negative-yield bonds were initially viewed as a curious anomaly, a by-product of the post-crisis experimental toolkit of monetary policy. Their seemingly absurd nature, paying the borrower for the privilege of lending, appears to contradict basic economic intuition. Over the past two years, however, their volume has expanded sharply, and in recent days it has reached a new record.

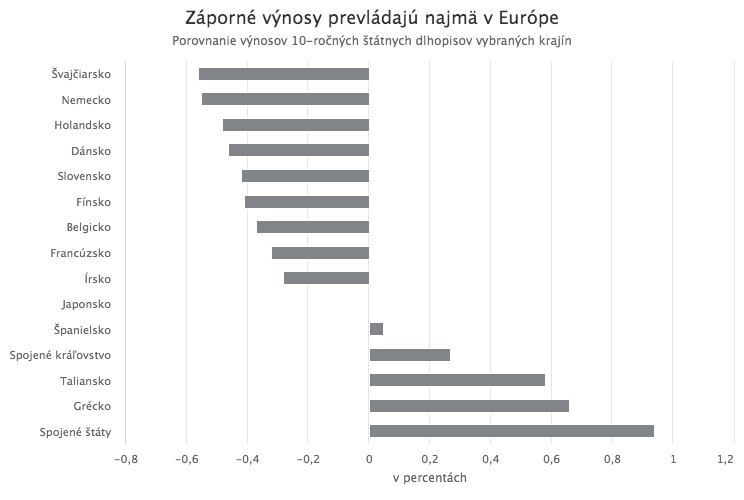

The stock of negative-yielding debt has now risen to USD 18 trillion, representing almost 20% of the global bond market and 27% of all investment-grade bonds. Negative yields are most prevalent in Europe, where they apply to more than two-thirds of euro area sovereign bonds, but they are also increasingly common in corporate credit. In general, the higher the perceived quality of the bond and the shorter its maturity, the lower its yield.

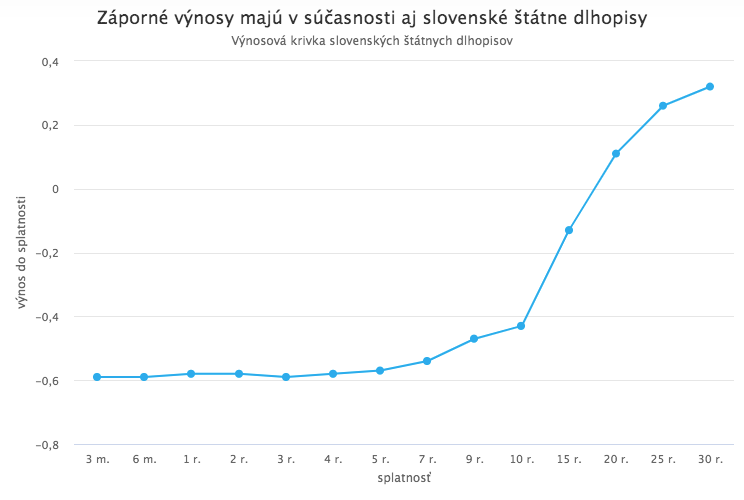

Even Slovak government bonds currently trade at negative yields, out to 15-year maturities. In other words, Slovakia can borrow in the market for up to 15 years at a yield below zero. As with other negative-yielding securities, the investors who buy these bonds are, in effect, paying Slovakia interest for the “privilege” of lending to it.

What pushed yields below zero?

This unusual environment is the result of weak economic conditions and extraordinarily accommodative central bank policies aimed at stimulating growth, above all negative deposit rates combined with bond purchases under quantitative easing (QE).

Central banks typically respond to recessions and crises by cutting policy rates to support economic activity. The 2008 global financial crisis and the subsequent euro area sovereign debt crisis, however, created risks severe enough that conventional rate cuts proved insufficient. The ECB and several other central banks therefore pushed policy rates to the limits of what was previously considered feasible.

After the euro area debt crisis, the ECB cut its main policy rate, which anchors the broader structure of market rates, to zero, and drove its deposit facility rate into negative territory. In theory, a negative deposit rate is intended to discourage banks from holding excess liquidity at the central bank beyond required reserves, and instead encourage lending and investment into the real economy.

Yet even with rates at zero or below, growth remained weak and deflation risks persisted. Cutting rates deeper into negative territory risked generating more side effects than benefits. As a result, the ECB and other central banks complemented rate policy with unconventional tools, most notably quantitative easing, often loosely described as “printing money.” Under QE, a central bank purchases assets, primarily government bonds, from banks and other financial institutions, paying with newly created reserves credited to commercial bank accounts.

These purchases mechanically raise the price of the targeted bonds, pushing their yields lower. When QE coincides with elevated economic uncertainty that boosts investor demand for the same safe bonds being bought by the central bank, with low inflation expectations, and with cash holdings penalized by a negative deposit rate, yields can fall below zero and remain there.

In Europe, negative yields first emerged in meaningful scale in 2016, shortly after the ECB pushed the deposit rate below zero and launched its first round of QE. Their volume surged again in the summer of the following year when the European economy began to stagnate amid a trade war backdrop, and the ECB lowered the deposit rate further (to today’s -0.5%) while continuing asset purchases. The outbreak of the COVID-19 pandemic briefly triggered a sharp, panic-driven rise in yields as bond prices sold off for several days.

But once central banks stepped in, delivering an unprecedented wave of monetary stimulus and effectively flooding markets with liquidity, yields resumed their decline and moved back into negative territory. This is hardly surprising. Since March, the world’s major central banks have, on average, purchased bonds and other assets worth roughly USD 1.3 billion per hour. The ECB’s deposit rate remains at -0.5%, and since the onset of the pandemic it has purchased more than EUR 700 billion of euro area sovereign bonds under its Pandemic Emergency Purchase Programme (PEPP). The stock of negative-yield debt rose decisively above USD 18 trillion last week, following the ECB’s decision to expand the program further.

Why would anyone buy bonds with negative yields?

In certain circumstances, it is possible to profit even from negative-yield bonds, if yields fall further into negative territory and the investor sells at a capital gain. Such positioning is, of course, speculative and entails risk. In most cases, negative-yield bonds deliver a negative return to hold-to-maturity investors. Yet demand remains strong, and not only from central banks executing QE.

Alongside central banks, major buyers include institutional investors such as banks, insurers, and pension funds. These institutions are often required, by regulation and investment mandates, to allocate a substantial share of their assets to high-quality, low-risk instruments, a category that includes safe sovereign bonds even when yields are negative.

In principle, such investors could choose to hold cash instead, using it gradually to meet liabilities, rather than locking in losses in bonds. In practice, however, that option can be even less attractive. Excess bank reserves are remunerated at the central bank deposit rate, which in the euro area is currently negative at -0.5%. This means euro area banks lose 0.5% per year on surplus liquidity held at the central bank. If they can purchase bonds with yields that are still negative but less negative than -0.5%, they may be better off buying those securities than holding idle reserves, because the loss is smaller.

Banks that face negative remuneration on their own balances often pass some of that cost on to clients with large deposits. Other institutional investors, such as insurers and certain funds with large pools of cash that must be held safely, also frequently face negative rates on uninvested balances. For them, as for banks, accepting a modestly negative bond yield can be preferable to holding cash at a bank account rate that is even more punitive. From this perspective, buying negative-yield bonds is simply a way to store liquidity in a safe form, and the negative yield is the fee paid for that safety.

Safe sovereign bonds, moreover, can still play a role in portfolio diversification and risk management, even if their yields are negative and their negative correlation with equities has weakened.

A world below zero

The explosion of negative-yield debt has meaningful implications for markets, investing, and the broader economy. One of the most direct and visible effects is an intensifying search for yield. When safe bonds offer zero or negative returns, investors become increasingly willing to allocate to almost any asset that provides some yield, often with insufficient regard for risk.

Consistent with that dynamic, the surge in negative-yielding debt has coincided with speculative-grade credit yields falling to record lows. The ability to borrow at extraordinarily low rates is, in the context of a pandemic, more than welcome. Over the longer term, however, it can incentivize firms (and, to some extent, sovereigns) to increase leverage to levels that may not be sustainable.

The search for yield has also supported a powerful equity rally and is likely a key driver behind various speculative bubbles visible in markets today.

Negative yields also pose a challenge to standard economic intuition and asset-pricing frameworks. Consider two firms identical in all respects except that one holds a large cash buffer while the other carries a large debt load. In the past, analysts would typically view the first firm more favorably and assign it a higher valuation, because cash is a safe asset and can be invested to earn a return, whereas heavy indebtedness raises concerns about repayment capacity and interest costs that depress profitability.

But what if the indebted firm’s liabilities are funded at negative rates, for example through bonds issued at negative yields? In that case, debt can, in a sense, become an asset: rather than representing a cost, it generates a financial benefit. Issuing debt may become more attractive than holding excess cash, and additional borrowing, up to a point, can increase returns. This turns familiar valuation logic on its head.

If the negative-rate environment persists, long-standing corporate valuation conventions may require adjustment. The same is true for derivative-pricing frameworks, given that many widely used models were designed with strictly positive interest rates in mind.