The New CBRT Governor Raised the Policy Rate by as Much as 4.75 Percentage Points

At its first meeting under the new governor, the Central Bank of the Republic of Türkiye (CBRT, formerly TCMB) delivered a sharp increase in the main policy rate. The aim is to stabilize the lira, which has depreciated markedly this year. But will it be enough?

Naci Ağbal, the new governor of the CBRT, is seeking to halt the lira’s steep depreciation. At its first meeting under his leadership, the CBRT raised the main policy rate from 10.25% to 15%. At the same time, the Bank is trying to restore investor confidence by increasing policy transparency. It announced that it will henceforth provide all liquidity exclusively through the main policy rate.

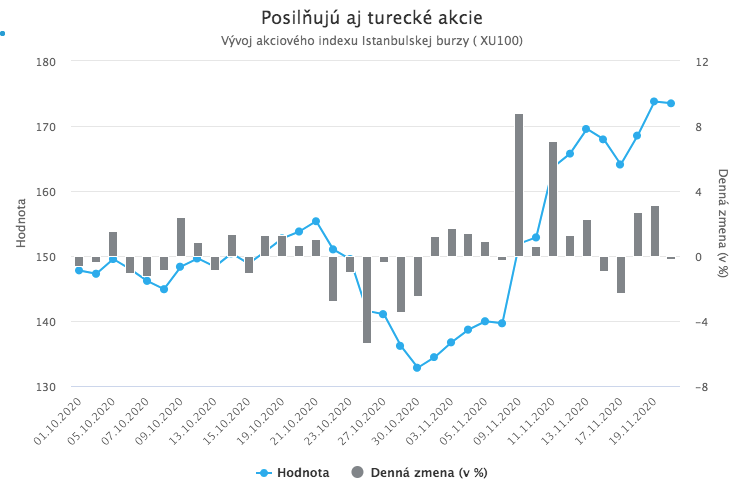

Investors welcomed these steps, and the lira began to show signs of stabilization. Turkish equities moved sharply higher. The question is whether this optimism is premature.

Problems of the Turkish lira

The change of the CBRT governor and the Bank’s decision to proceed with a massive rate hike were preceded by dramatic developments. The long-term weakening of the Turkish lira accelerated further this year due to the coronavirus crisis and problematic domestic economic policy. Prior to the governor’s replacement, the lira had been weakening for 11 consecutive weeks, and its loss since the beginning of the year reached as much as 34%. This year, the lira has been competing with the Brazilian real for the unenviable title of the weakest currency.

The lira’s depreciation reflects a combination of several factors. Ongoing efforts to stimulate the economy through credit expansion, combined with a high need for external financing, make the Turkish economy highly vulnerable to external shocks and put upward pressure on inflation. At the same time, Türkiye has long struggled to fight inflation effectively, because the economic theories of President Erdoğan, who has significant influence over the central bank’s decision-making, are notably “unorthodox” in this area. Unlike virtually all experts, the Turkish president believes that high inflation should not be fought by raising rates, as standard economic theory suggests, but by lowering them. He calls interest rates “the mother and father of all evil,” and lowering rates has long been one of the central points of his political campaign.

The lira is also undermined by Türkiye’s frequent military and geopolitical “adventures”, which regularly bring the threat of US or EU sanctions. Foreign investors are naturally also dissatisfied with repeated attacks by the president on foreign banks operating in the country, accusations that investors are trying to harm the Turkish economy, and various restrictions on cross-border capital movements, even though the Turkish economy critically needs foreign capital.

The coronavirus pandemic has only deepened these long-standing economic problems. At the same time, Joe Biden’s recent victory in the US presidential election increased the risk that the new US president would be less friendly and accommodating toward Erdoğan than Trump, and could impose sanctions on the country. Against this backdrop, the lira’s depreciation in recent weeks and months was not surprising.

A new governor and a new finance minister

In early November, Erdoğan concluded, likely also in light of the US election outcome, that the lira’s depreciation was no longer tolerable and had to be stopped. The first step was the dismissal of the CBRT governor. Under normal circumstances, such a move would be entirely justified, as the central bank is primarily responsible for currency stability. In this case, however, the situation is somewhat specific, and the dismissed governor Murat Uysal may feel a sense of injustice. He was doing exactly what Erdoğan wanted. His predecessor had been dismissed precisely because he did not comply with Erdoğan’s requests to cut interest rates and fought inflation (successfully) by raising rates and keeping them elevated until inflation began to decline.

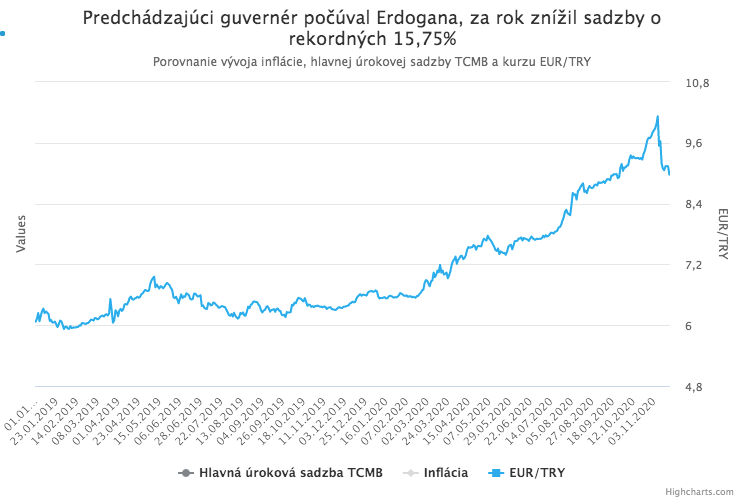

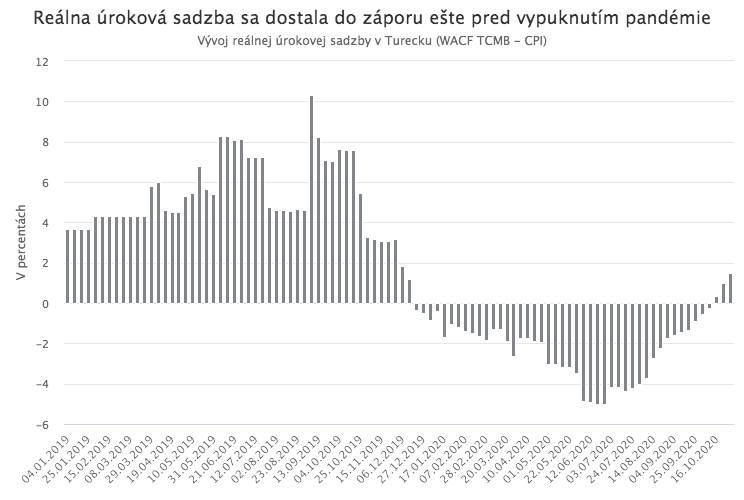

Murat Uysal clearly took lessons from his predecessor’s “mistakes” and willingly complied with Erdoğan’s calls to cut rates. In less than a year, he reduced the main policy rate by a record 15.75 percentage points. Initially, such rapid cuts were not a problem, because gradually declining inflation created some room for rate reductions, supported also by the easing stance of the world’s major central banks. Uysal, however, continued cutting even after inflation stopped declining. The country’s real interest rate thus moved deep into negative territory even before the coronavirus crisis began.

When the pandemic then hit, Türkiye, unlike the vast majority of countries, could not afford to support the economy by cutting rates, as doing so would only have intensified the lira’s depreciation and accelerated inflation, thereby damaging the economy even more. To stop the sharp fall in the lira, it was necessary, on the contrary, to raise rates.

Yet even as the lira was sliding, Governor Uysal waited too long to raise rates, most likely at Erdoğan’s instruction, as the president continued to publicly oppose rate hikes. Uysal instead tried to slow the lira’s decline using every other tool available to the CBRT, from running down foreign-exchange reserves to “stealth” tightening (the CBRT did not raise the main policy rate, but it stopped providing liquidity at that rate). These substitute measures helped slow the lira’s slide in the short term, but in the longer term they worsened the situation. Ultimately, when all other tools were exhausted, Uysal (with Erdoğan’s tacit consent) proceeded to raise rates. But it came too late and was insufficient. The lira continued to weaken, and Uysal ultimately paid the price.

The day after Uysal’s dismissal, Finance Minister Berat Albayrak, the husband of Erdoğan’s daughter, also resigned. He cited health reasons; however, the real reason was reportedly that he had been concealing the true state of the Turkish economy from Erdoğan. Surrounded by loyalists, the president had allegedly been receiving economic information in recent months only from his nephew, who embellished it significantly and told his brother-in-law that the Turkish economy was in fact undergoing a major and successful transformation. However, the falling lira, rising unemployment, and high inflation had already negatively affected the popularity of the president’s AKP party, and party colleagues reportedly decided to inform him of the true scale of the economic problems. Erdoğan was furious and forced his nephew to resign.

Genuine shift toward more responsible economic policy?

The personnel changes were accompanied by a partial shift in Erdoğan’s rhetoric. He stated that Türkiye wants to regain investors’ trust and that it respects the central bank’s independence, giving it a free hand to fight inflation. He even suggested he would accept the hated and long-rejected rate hikes: “We will not hesitate to do what is necessary, even if it is painful.”

Investors welcomed these steps and statements and appear to have believed they mark the beginning of Erdoğan’s sincere effort to restore confidence, attract foreign capital, and address the country’s economic problems more effectively. The lira strengthened immediately, and Turkish equities, especially in the banking sector, surged. The decisive rate hike at Thursday’s central bank meeting under the new governor further reinforced these expectations. The lira continues to strengthen.

The question, however, is whether investors have been carried away by excessive optimism. While recent steps do represent a positive turn in economic policy, it is unclear how long they will last. Erdoğan himself reiterated on Wednesday in Ankara that he still considers high interest rates to be the cause of inflation. It is unlikely he has truly changed his views. The current measures therefore appear more like a calculated attempt to stop the lira’s excessive depreciation, rather than a sincerely intended, long-term positive change in economic policy.

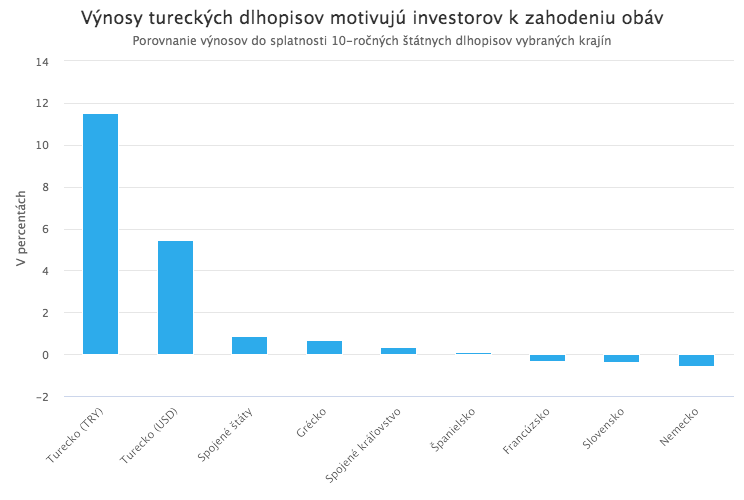

But a simple look at Turkish bond yields compared to European or US yields makes it clear that foreign investors have a strong incentive to set aside any doubts about the sustainability of the current shift toward more responsible economic policy.