Tensions are rising, and the market remains volatile.

Inflation is rising to multi-year highs

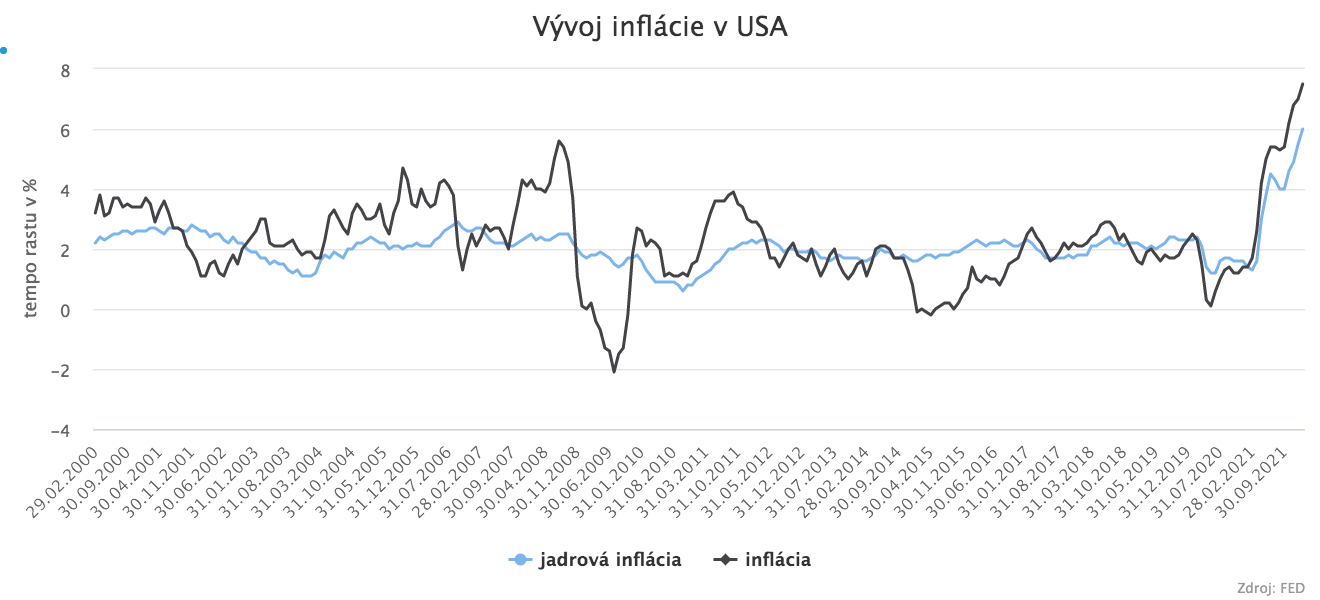

Year-on-year inflation in the U.S. reached 7.5% in January, the highest rate since February 1984. According to forecasts, this should mark its peak, and we should see it slow in the period ahead. This multi-year high is driven mainly by rising energy prices and disrupted supply chains. In recent months, these factors have begun to feed more noticeably into other components of inflation. Therefore, in addition to the typically elevated price level, we are also seeing an increase in core inflation to 6%. Core inflation excludes items such as energy and other goods that the central bank has limited or no direct influence over through its monetary tools. Alongside rising inflation, the U.S. economy has been successful in reducing unemployment, and the pace of economic growth in the fourth quarter reached 6.9%. For the full year, growth was as high as 5.7%, which represents the highest level since 1984. These positive data provide the Fed with a solid foundation to begin raising the main interest rate in the near future, thereby taking action to combat rising inflation. According to the latest reports, rate hikes could begin at the March meeting, and the expected pace of increases should be faster than in 2015. At the same time, the Fed is facing a historic gap between the inflation rate and the level of the main policy interest rate. Of course, central bankers will also need to tighten monetary policy due to strong economic performance in order to prevent the economy from overheating.

The Eurozone has a similar problem, but with a difference

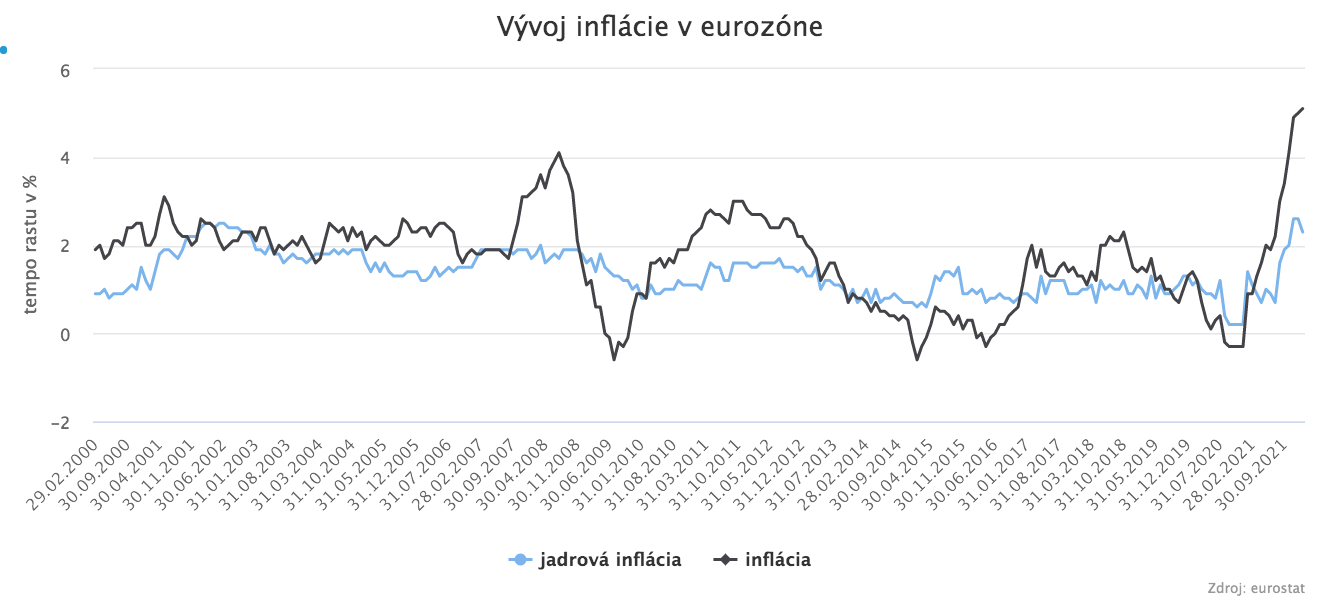

In January, year-on-year inflation in the Eurozone rose to 5.1%, which is a record high. The difference compared to the U.S. is that in the Eurozone, energy prices are passing through to other goods much less and more slowly. Evidence of this is core inflation, which in the latest reading slowed to 2.3%, and that gives the ECB little reason to significantly change its monetary policy. This is also why the ECB’s leadership says that we are in a different situation than the U.S. The difference also lies in the strength of Eurozone GDP growth, which in the last quarter of the previous year grew at a pace of only 0.3%. This is probably due to much stricter restrictions in the fight against the pandemic, which have taken their toll. Germany itself estimates that its economy lost approximately EUR 330 billion in GDP growth due to the pandemic. Not to mention that the labor market is not in as good shape as in the U.S., since the Eurozone has higher unemployment. Finally, if the ECB were to proceed with a complete halt to asset purchases, countries such as Italy, Spain, Greece, and others would come under financial strain. After the last financial crisis, these countries faced existential problems and were unable to borrow on financial markets at sustainable interest rates. The ECB, through its accommodative monetary policy and purchases of their bonds, ensured a fragile stability that would end if those purchases stopped. These states would likely again find themselves in a situation where they would face the risk of default. That would endanger the entire Union, and it is something we cannot afford after the pandemic ends.

The V4 is in a worse situation

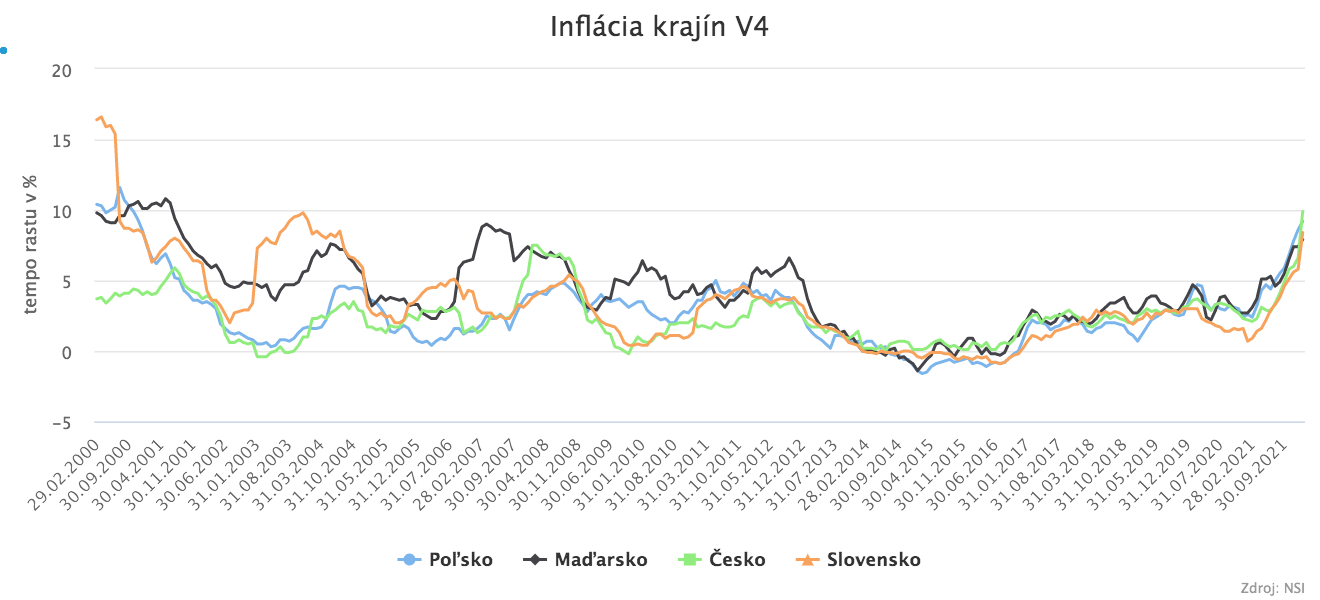

The economic area of the V4 countries is suffering from some of the highest inflation rates in the EU. Specifically, Hungary has inflation at 7.9%, Slovakia at 8.4%, the Czech Republic at 9.9%, and Poland at 9.2%. The problem in these countries is that core inflation is also rising significantly and its pace is not slowing, as it is in the Eurozone. Therefore, the V4 countries that have their own currencies have begun raising interest rates, aiming to bring inflation under control. By contrast, Slovakia is part of the Eurozone and does not have this option, so it will be interesting to watch whether rate increases in neighboring countries cause not only an economic slowdown but also a decline in inflation. Honestly, we have to admit that these countries are not economic superpowers, and a large part of this inflation is imported from abroad. According to the latest forecasts, we should see peak inflation in Slovakia at around 10% in the coming months. Another problem for these countries is their border with Ukraine, which is facing the threat of a military conflict with Russia. This topic is significantly unsettling equity markets, and the whole world fears conflict. However, Russia has not chosen the path of diplomatic solutions and is escalating tensions. Russia recognized the independence of two separatist republics in eastern Ukraine and at the same time signed agreements with them. These agreements allow Russian troops to enter “their” territory, and they even allow Russia to build bases there. Putin used the approved agreements immediately and ordered the deployment of “peacekeeping troops.” Such steps only escalate an already extremely serious situation. Of course, Western allies can no longer wait and have announced the imposition of economic sanctions. The U.S. immediately imposed a ban on investing or trading in and with the separatist territory. In addition, it also imposed sanctions on Russian banks and oligarchs. The United Kingdom imposed sanctions on five Russian banks and three individuals. The EU unanimously approved a package of sanctions against Russia. Other allies such as Japan, Canada, and Australia took similar steps. In essence, the first package of sanctions aims to prevent Russian sovereign debt from being financed on Western financial markets. A major problem is also fossil fuels, since a conflict with Russia could lead to a halt in the flow of commodities and another extreme surge in energy prices. This is also suggested by the move of the German Chancellor, who suspended the Nord Stream 2 project. By contrast, the Russian president is reassuring global markets that energy commodities will continue to be exported from his country. However, the question is whether the West would, in the event of an open conflict in Ukraine, still be interested in energy commodities from Russia. Following the latest developments, the main Russian stock index fell by more than 20%, and from its peak it had lost almost 35%. Energy stocks are no exception and are suffering significant losses. By contrast, Western energy companies are holding their value even in these turbulent times.

Oil at multi-year highs, OPEC+ is losing momentum

After the pandemic low, when demand for oil was weak because population mobility fell sharply at the time, things look very different today. Oil is reaching nearly USD 100 per barrel, both Brent and WTI. The oil cartel OPEC+ is increasing oil production quotas, but several countries are unable to produce more because they have not invested in extraction technologies. Some OPEC members’ capacities are therefore already at their limits, and demand for oil remains strong. As a result, the world is urging OPEC countries that are able to increase production to do so, and not to wait for an oil shock. Because of this, a number of analysts believe the price of “black gold” could break the psychological level of USD 100 per barrel and subsequently reach as high as USD 150. Gas prices are also rising; however, they are still more than 100% below their recent peaks. That does not rule out a dramatic increase if tensions in the East escalate. This scenario would be very realistic if a military conflict were to arise on the EU’s eastern border. At the moment, it appears that diplomatic talks so far have not led to any result. The EU is the most economically at risk, as it is highly dependent on Russian gas and oil. As much as 43% of imported gas and almost 30% of imported oil comes from Russia. The positive news is that the EU is making enormous efforts so that, in the event of a complete disruption of fossil fuel flows from Russia, it would be able to import these commodities from other countries.

Markets are losing support after a small correction

Equity markets are waiting to see how all of the issues mentioned above will unfold. As far as companies are concerned, most major corporations delivered solid numbers in the earnings season for last year and the most recent quarter, so from that perspective there is nothing preventing markets from continuing the growth seen last year. However, today it is not about corporate results, but about monetary policy and geopolitical risk. The pandemic appears to be receding, and most countries are announcing plans to roll back all anti-pandemic measures. Let us hope, then, that an armed conflict does not occur and that the world manages to deal with elevated inflation without triggering another recession.