Stock Markets Continue Their Strong Rally

Stock markets, unlike bond markets, continue to post strong gains. They are being driven by positive macroeconomic data from recovering economies as well as solid corporate results for the first quarter. Major U.S. and European stock indices have risen by more than 10% since the start of the year. Is this pace of growth sustainable?

U.S. stock indices at new highs

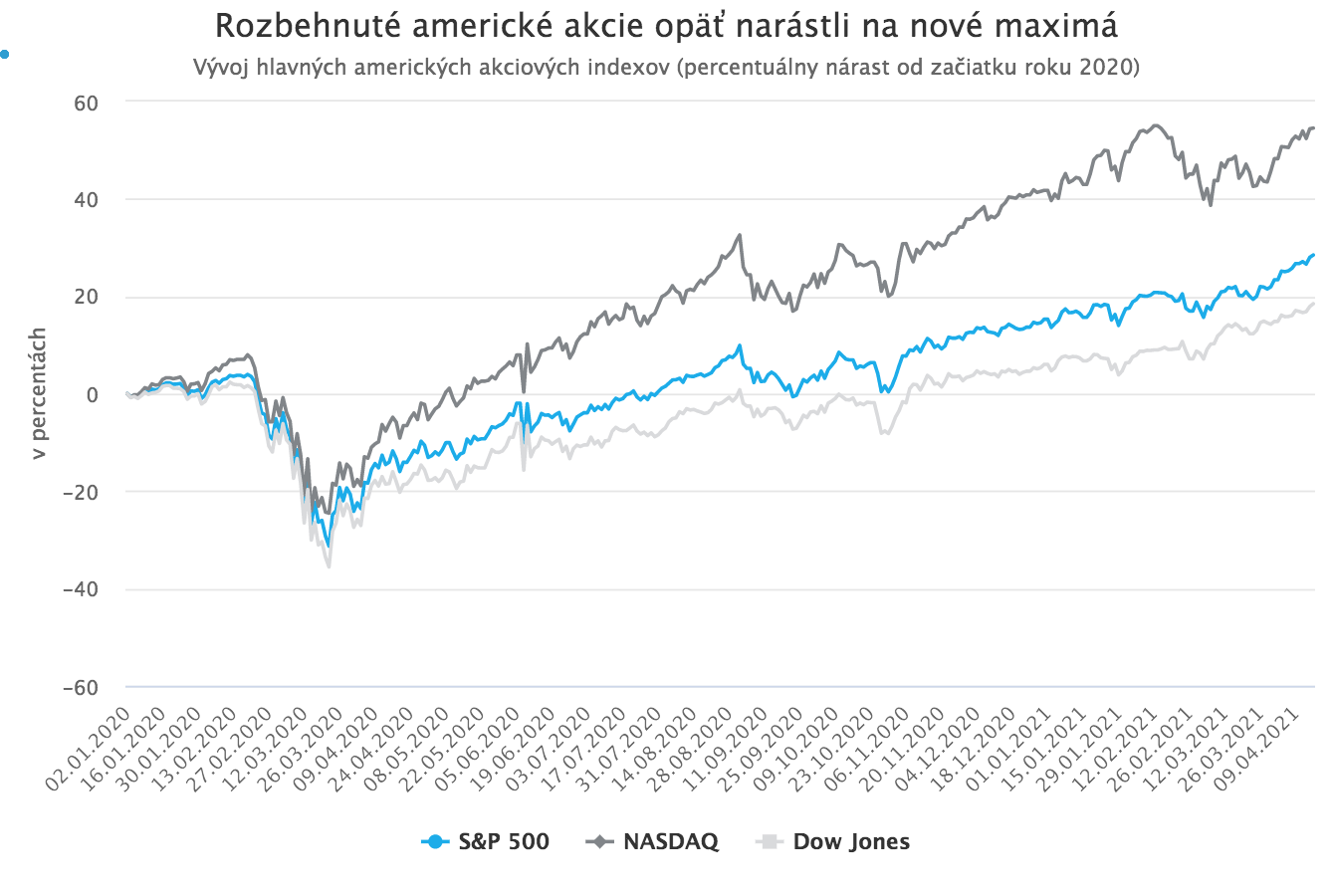

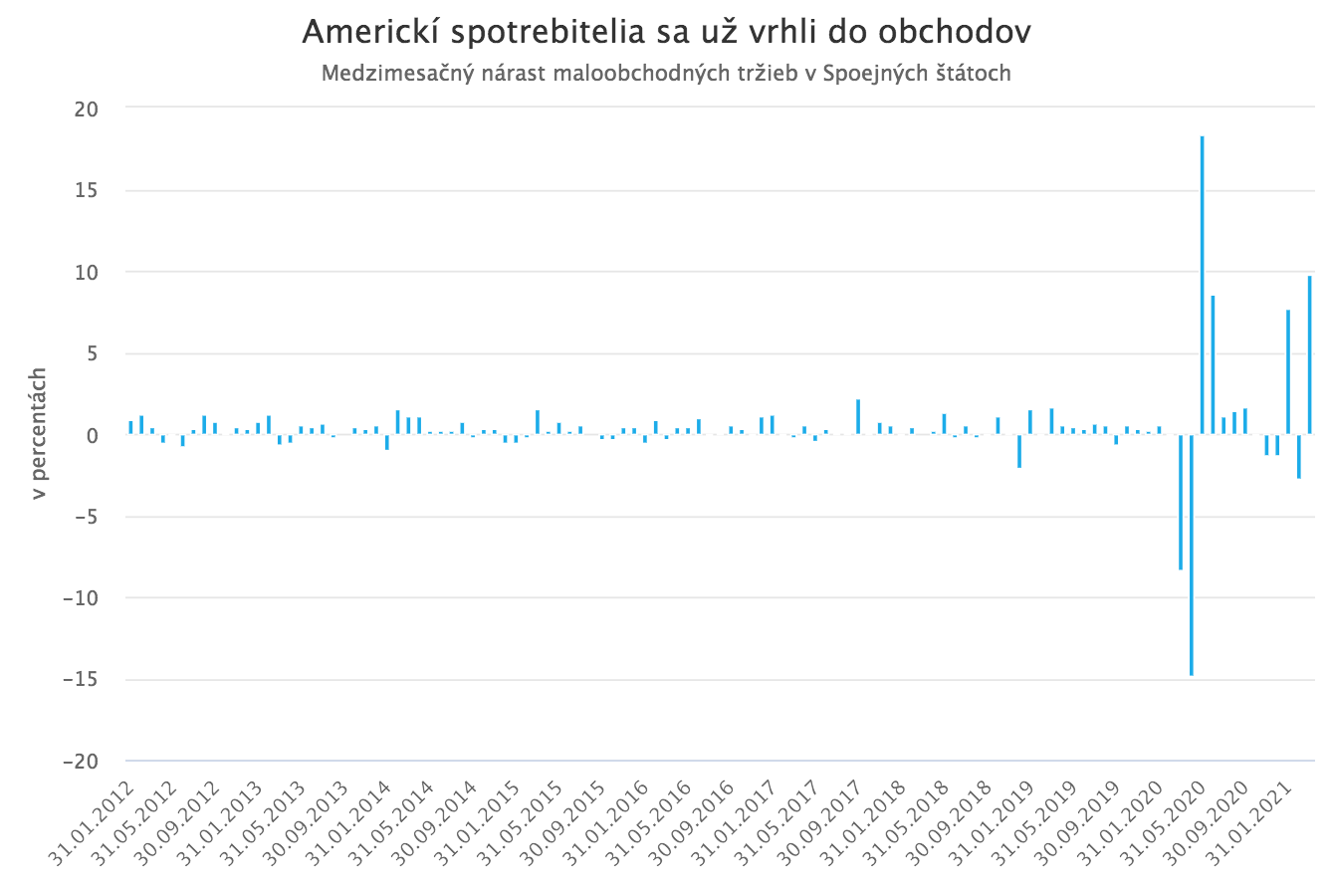

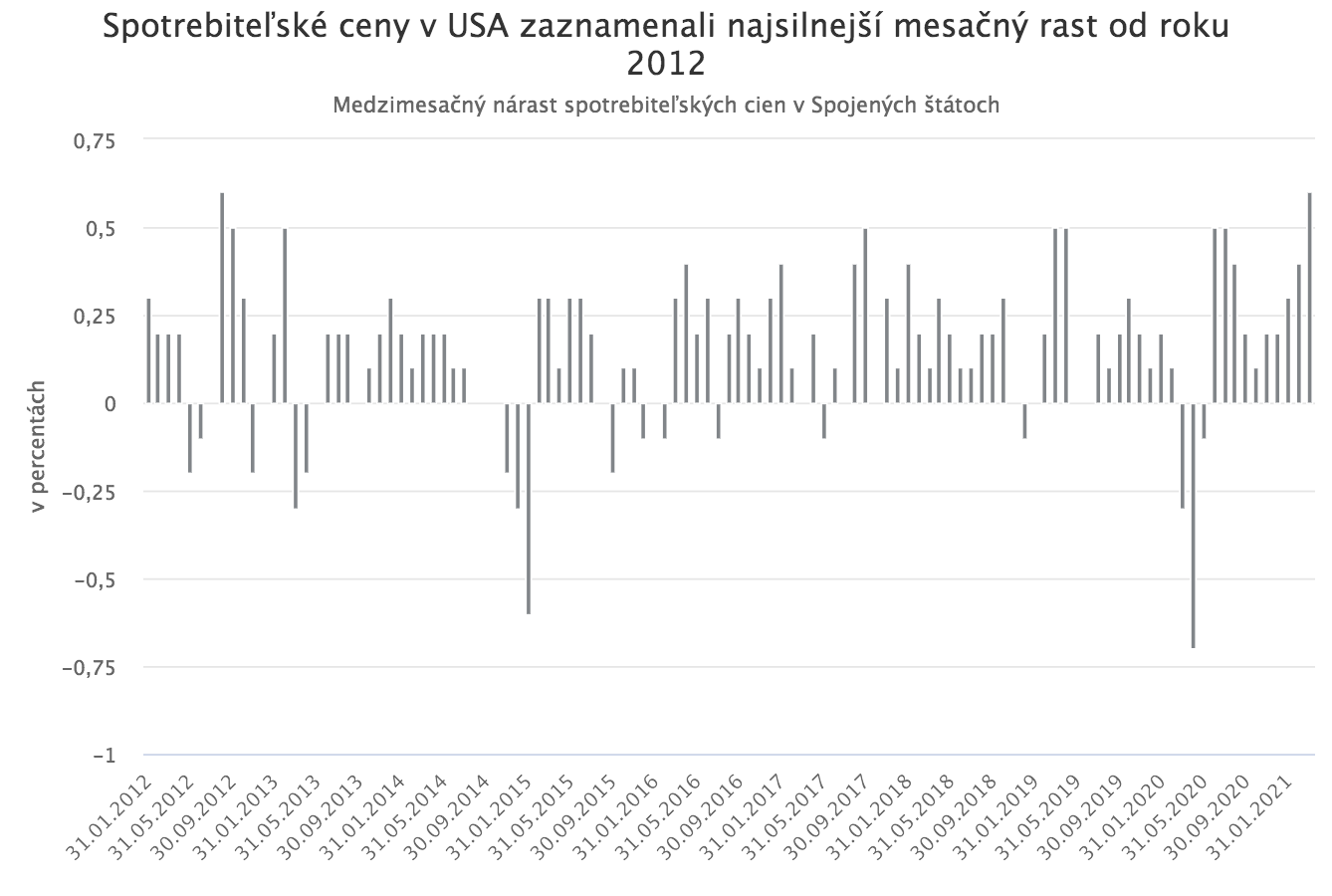

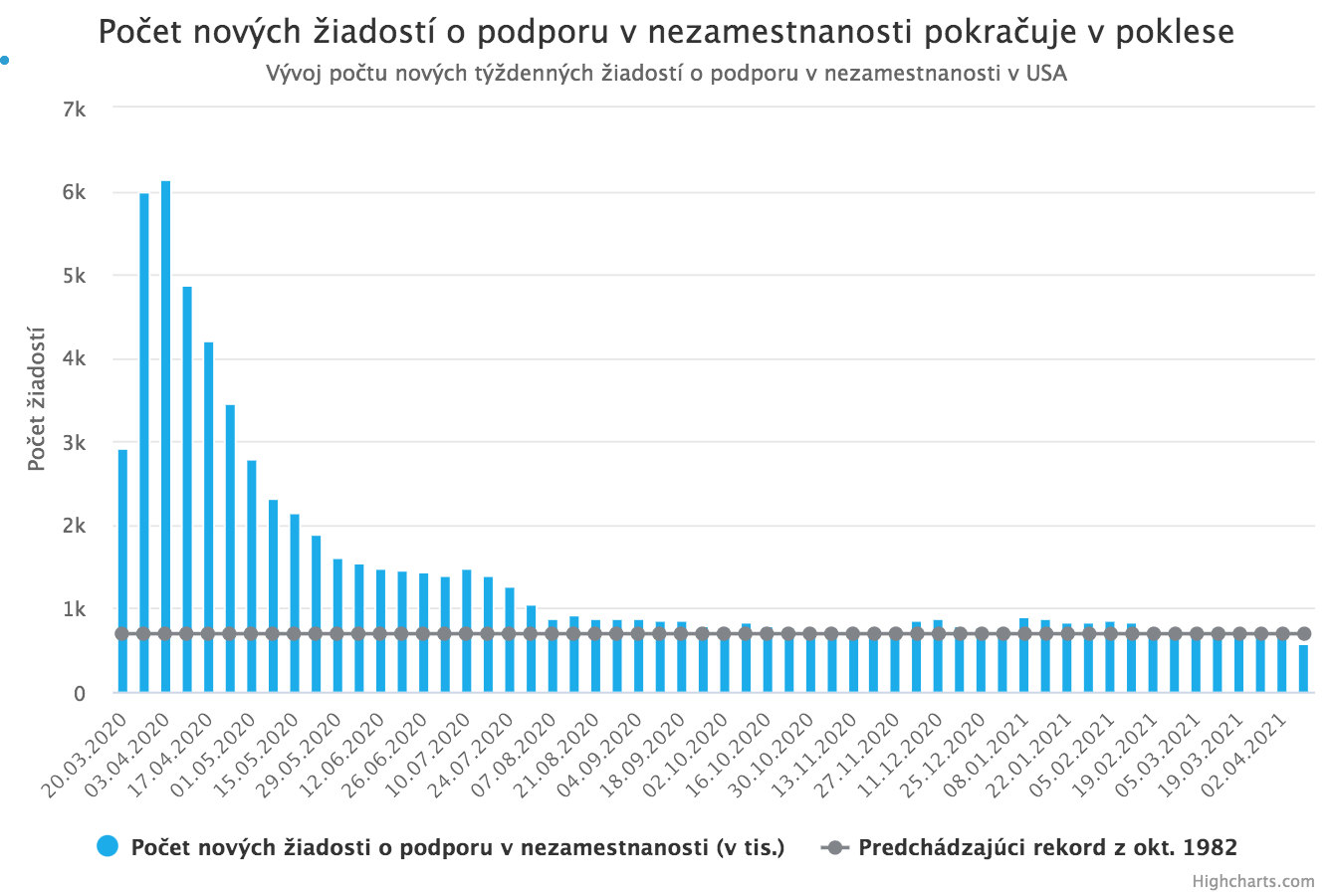

For U.S. equity markets, the market panic that followed the outbreak of the pandemic is now only a distant memory. From the bottom in March last year, they have risen by more than 80%, and it seems nothing will stop them from continuing to climb. All three major stock indices reached new highs again last week. The benchmark S&P 500 has gained more than 11% since the beginning of the year. The industrial Dow Jones posted a similar result, and the tech-heavy Nasdaq is slightly behind with “only” a 9% gain. U.S. stocks have been lifted in recent months mainly by optimistic expectations of a strong recovery in the U.S. economy supported by massive fiscal stimulus and a fast pace of vaccination. Last week’s series of macroeconomic releases reassured investors that these expectations have a realistic foundation and that the U.S. economy is indeed on track for a rapid recovery. The data show that U.S. consumers, tired of the pandemic and sitting on accumulated savings, have returned to shopping as businesses reopen. Retail sales surged by as much as 9.8% last month, far exceeding expectations. This is one of the best figures on record. Rising consumer spending, naturally, also pushes consumer prices higher. Inflation thus recorded a 0.6% increase last month. This was the highest month-on-month increase since 2012, which in the current situation is viewed as healthy and even welcome. It shows that deflationary pressures caused by the economic shutdown are easing and that consumer demand is recovering quickly. Signs of the U.S. recovery can also be seen in the latest labor market data. Although conditions are still far from ideal, there is visible improvement. New unemployment claims have been falling for several weeks in a row, and last week they dropped for the first time since the pandemic began below the previous record from October 1982. An excellent start to the first-quarter earnings season also shows that not only macroeconomic indicators are recovering, but corporate profits as well. The biggest U.S. banks in particular stood out, with results that significantly exceeded all expectations.

European stocks are also doing well, but Chinese stocks are falling

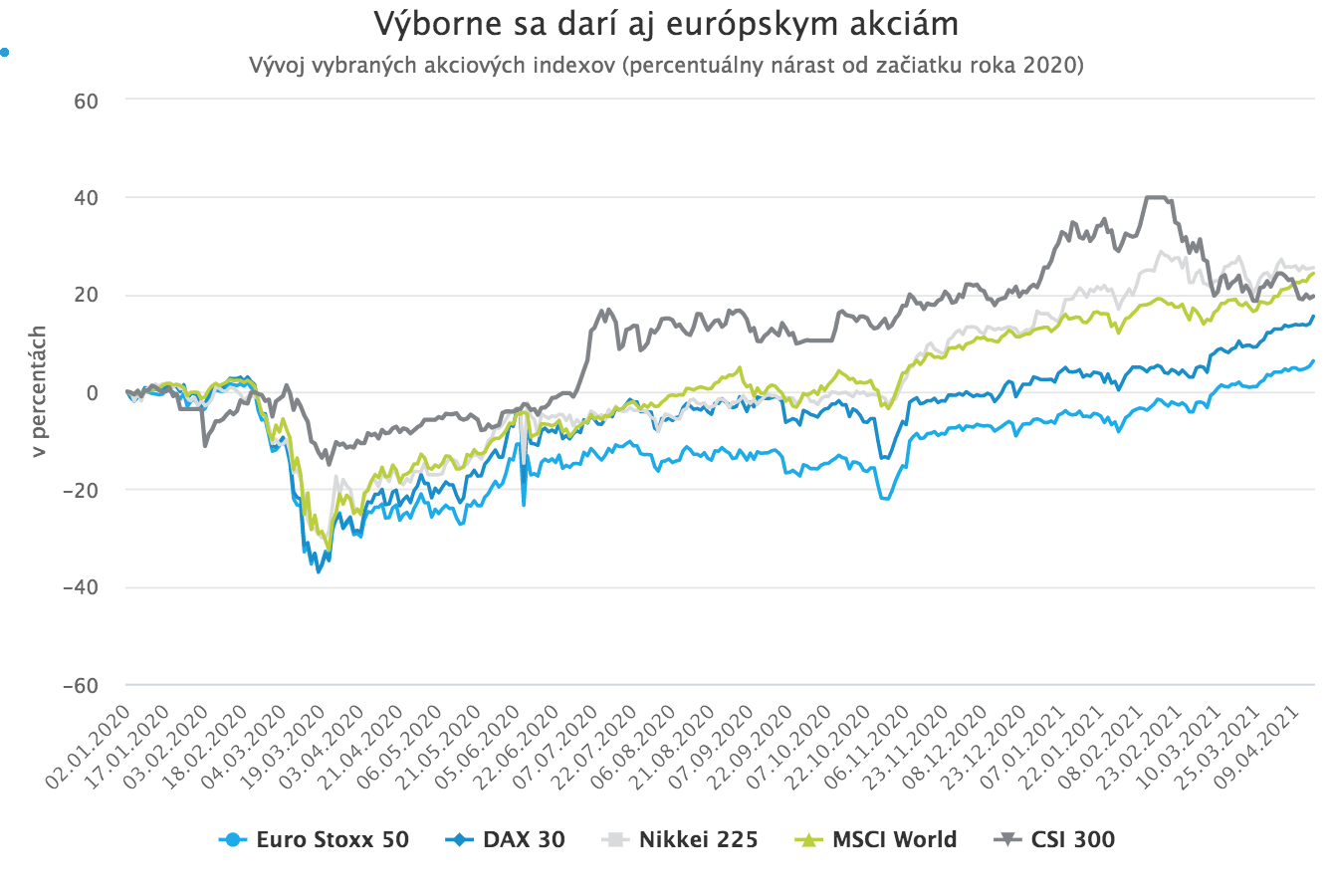

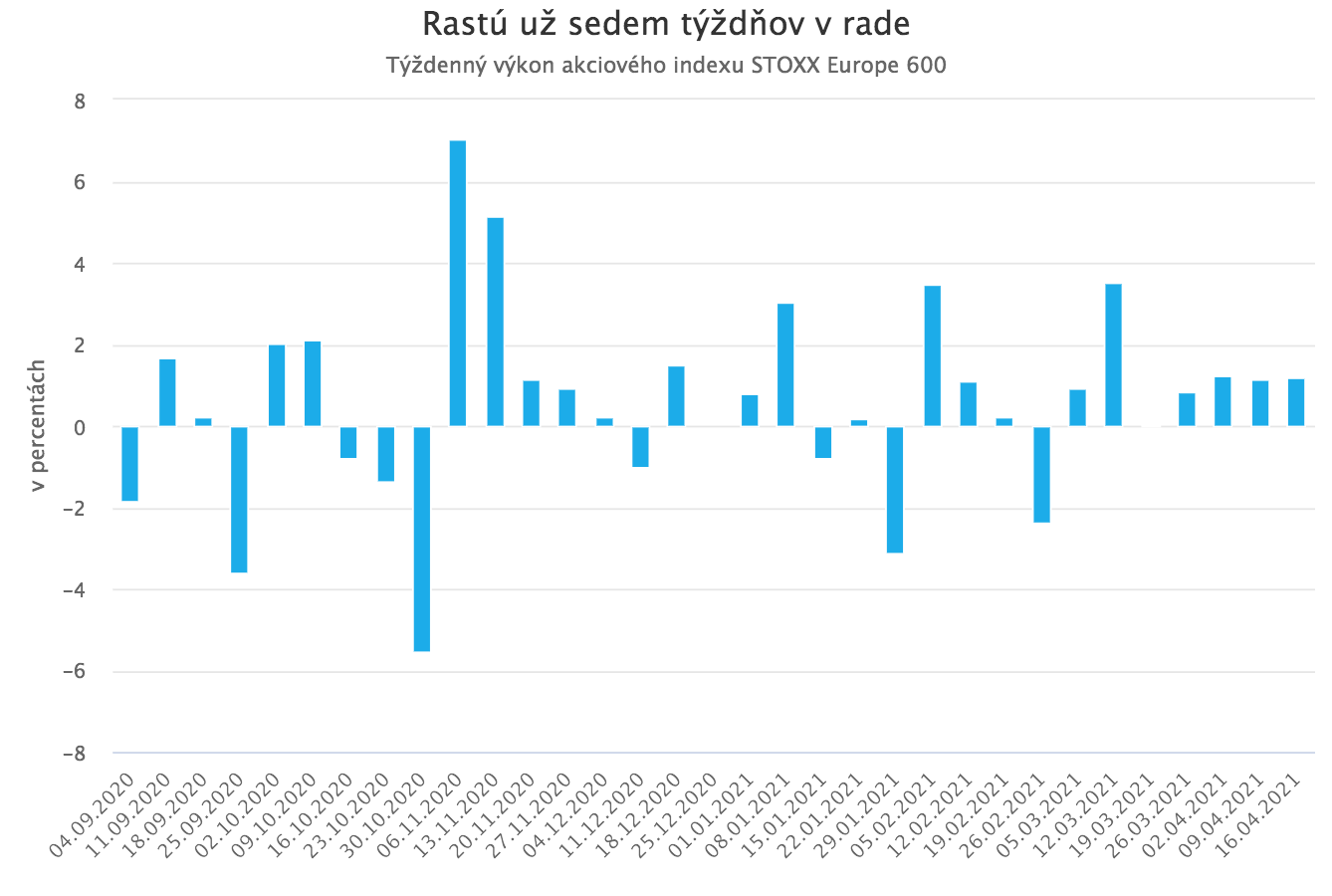

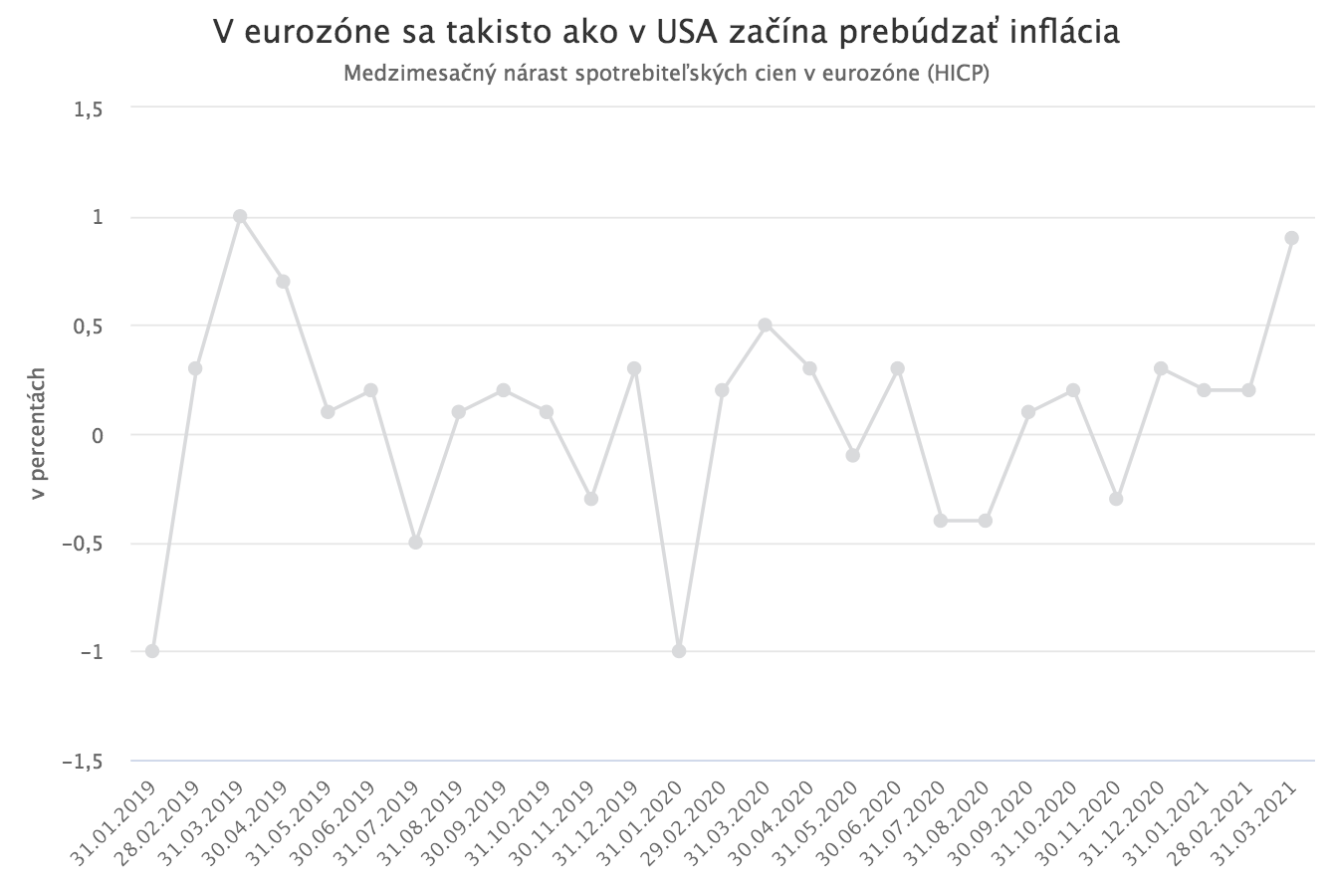

Strong growth is also continuing in stock markets across many other countries. One interesting exception, however, is China. Despite the strong performance of the domestic economy, Chinese stocks have been declining quite sharply since February and have lost almost 5% compared to the start of the year. The main reasons behind the declines are steps by the Chinese government aimed at tighter regulation of technology companies and the central bank’s intention to slow credit growth in the economy. Growth this year is expected to be the slowest pace in 15 years. In other markets, however, the development has been much more favorable. The global MSCI World equity index has risen by 10% since the start of the year. European stocks have been performing even more strongly. They lagged behind U.S. and Chinese markets for most of last year and are only now returning to pre-pandemic levels, but that makes their growth this year even more pronounced. The pan-European STOXX Europe 600 has risen for seven consecutive weeks, and its gain since the beginning of the year has already exceeded 11%. Some European regional indices have improved by as much as 15%. European stocks, like U.S. stocks, have also been supported in recent days by a strong start to the earnings season. A particularly positive surprise was the results of Daimler. Over the long term, however, European equities have been driven mainly by optimistic expectations about a recovery in the European economy, which so far are not as strongly supported by data as in the case of the U.S. economy. The recovery and the pace of vaccination have been significantly slower in Europe. Inflation data for March, published last week, also showed a strong increase in consumer prices in the eurozone. Prices rose by 0.9% month on month.

Is a market correction coming?

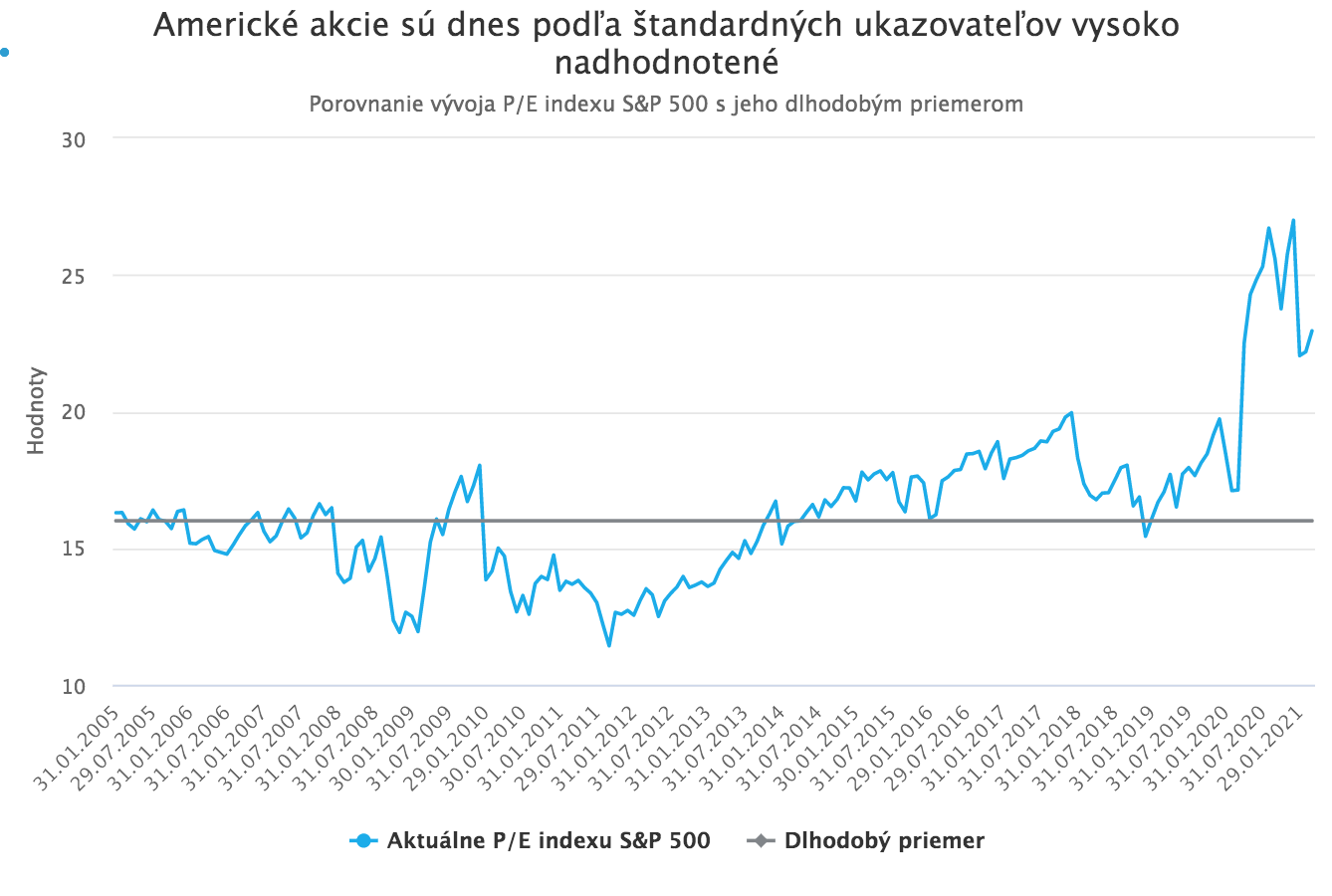

The persistent, almost uninterrupted strong rally in stock markets over recent months is generating not only euphoria among investors, but also growing concerns. It does not seem likely that it is sustainable. Major equity indices have climbed within less than four months of the new year to levels that, according to forecasts by analysts at the most prestigious investment banks, were expected to be reached over a 12-month period. In any case, history has seen few years in which stocks gained more than 10% every four months. From a sustainability perspective, U.S. stock valuations currently appear particularly problematic. All standard valuation metrics suggest that at today’s levels they are significantly overvalued. The P/E ratio (price-to-earnings ratio) of the S&P 500 is currently far above its long-term average. For this ratio to return to its long-term average, either the index would have to fall by 27%, or average earnings per share would have to rise to USD 250. Such an increase does not seem achievable in the near term even under the most optimistic scenarios. According to forecasts, year-end average earnings per share for companies in the index should reach only USD 175. In 2022 it should be around USD 200, and the year after that USD 220. It therefore seems that current U.S. stock prices already reflect profits that are not realistically achievable in the near term even under the most optimistic scenarios. Of course, that does not automatically mean U.S. stocks are headed for a 27% drop. Such a decline is, on the contrary, rather unlikely. Stocks can remain at overvalued levels for a long time, especially in today’s environment shaped by extremely loose monetary policy. Nevertheless, it is hard to shake the impression that equity prices (not only in the U.S.) already incorporate the most optimistic expectations regarding economic recovery and rising corporate profits. Any disappointment, such as a series of weaker macroeconomic releases or a weaker quarter of corporate results, could bring a correction. Not to mention the potential emergence of new virus variants resistant to vaccines.