The Euro Area Has Emerged from Recession, but a Slowdown Is Already Visible in China and the US

According to the latest data, European economies, including Slovakia, recorded strong growth in the second quarter, thereby emerging from the double-dip recession caused by the pandemic. Several of them, however, are experiencing not only robust GDP growth but also rapidly rising inflation. In the United States and China, the economies that began recovering from the pandemic earlier than Europe, a slowdown is already clearly visible.

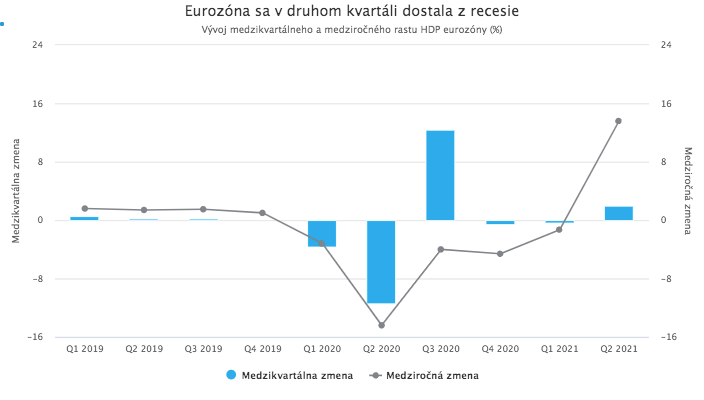

Recent days have brought a large amount of interesting macroeconomic data from Europe, China, and the United States. Some were positive, others concerning. Let us start with the positive news. The latest Eurostat figures confirmed that the euro area has emerged from the double-dip recession caused by the pandemic.

The euro area has emerged from a double-dip recession

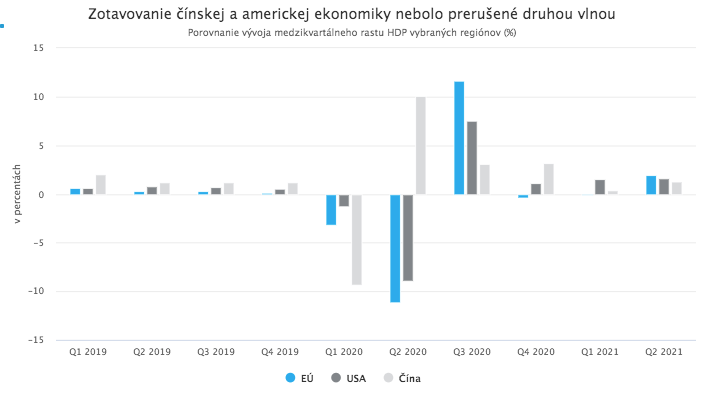

Europe was among the regions most severely hit in the early months of the year by a strong second wave of the pandemic. This naturally had a negative impact on economic performance. In the first three months of the year, the euro area suffered a second consecutive quarterly contraction and, after a strong performance in the third quarter, technically fell back into recession. By contrast, the United States and China avoided this outcome and continued to grow uninterrupted through the autumn and winter months.

A renewed acceleration of the recovery began in most European economies only in the second quarter. According to the latest Eurostat estimates, the euro area economy expanded by as much as 2% quarter on quarter during this period. On a year-on-year basis, the increase reached 13.6%; however, this elevated year-on-year figure naturally reflects, to a large extent, base effects, as Q2 of last year was the period most severely affected by the pandemic.

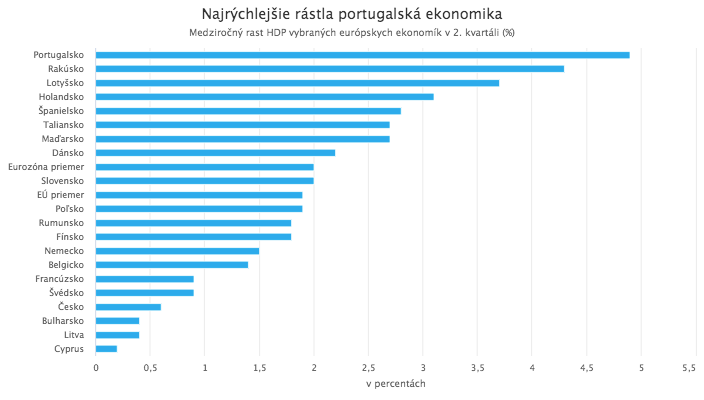

Performance differed substantially across European economies. Among the European countries that have already published their results, Portugal (+4.9%) and Austria (+4.3%) recorded the strongest quarterly growth. By contrast, Cyprus (+0.2%), Lithuania (+0.4%), and Bulgaria (+0.4%) recovered the most slowly. The Czech economy (+0.6%) also lagged significantly behind the EU average (+1.9%).

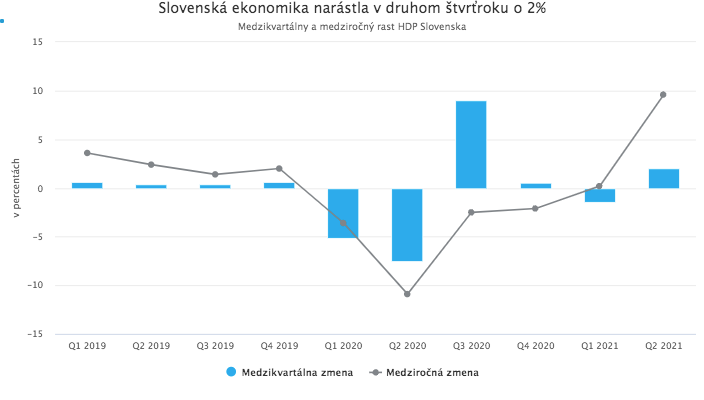

In Q2, the Slovak economy recorded solid 2% growth, exactly in line with the euro area average. Compared with Q2 of last year, it increased by as much as 9.6%, marking its best performance since 2007.

A strong recovery, driven by both external and domestic demand, took place across virtually all key sectors of the domestic economy. As a result, the Slovak economy has already erased most of last year’s decline and returned close to pre-pandemic levels. Registered unemployment stood at 7.8% at the end of Q2. This represents a slight improvement compared to the previous quarter (8%), but the Slovak labor market remains far from pre-crisis levels, where unemployment was around 5%.

The recovery is accompanied by rising inflation

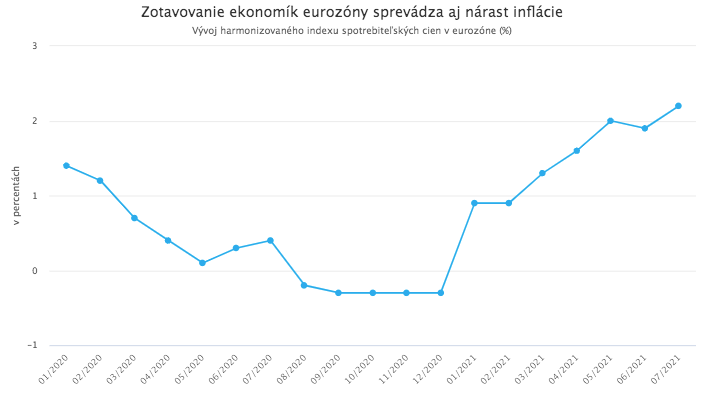

The recovery of European economies is also accompanied by rising consumer prices, although so far not nearly as pronounced as in the United States. According to the latest Eurostat data, inflation in the euro area reached 2.2% year on year last month. This is the fastest pace of price growth since October 2018. The sharp move in inflation from -0.3% at the end of last year to the current 2.2% looks rather dramatic on a chart; in reality, however, it does not yet warrant panic.

For a long time, the ECB’s inflation target, which it traditionally struggled to meet, was defined as “below, but close to, 2%.” Inflation in the vicinity of 2% was last observed in the euro area back in 2018. Since then, the ECB has failed to get close to this target, and for most of last year the euro area even struggled with deflation, which is at least as serious a threat to the economy as an inflationary spiral. In the current environment, a certain acceleration in euro area inflation, if accompanied by economic growth, is therefore more welcome than alarming. The ECB expected it, will tolerate it, and has adjusted its policy accordingly. The definition of the ECB’s inflation target was changed just last month from “below, but close to, 2%” to a symmetric 2% target over the medium term.

This means the ECB will, similarly to the Fed, tolerate inflation above 2% for some time without prematurely tightening monetary policy in a way that could jeopardize the recovery from the crisis. The Bank assumes that the current acceleration in inflation is temporary in nature and will stabilize after several months.

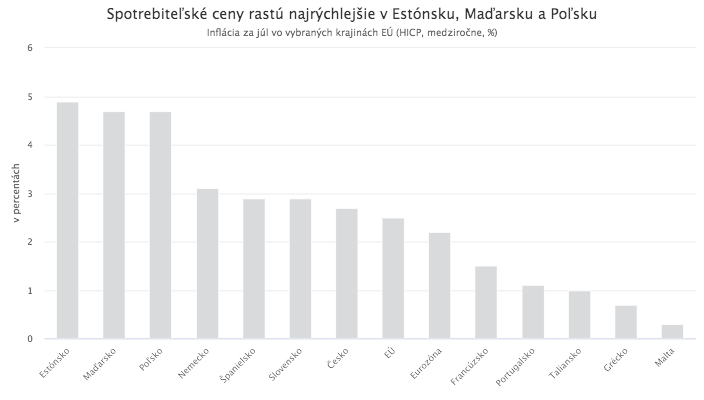

From the perspective of individual countries, however, price growth in Europe remains quite uneven, which may later prove problematic. Within the euro area, inflation is currently highest in Estonia (+4.9%) and lowest in Malta (+0.3%) and Greece (+0.7%). In Slovakia, consumer prices in July rose at a year-on-year rate of 2.9%, faster than the euro area average (+2.2%) and the EU average (+2.5%). Inflation is also running above average in Europe’s largest economy, Germany.

The current acceleration in euro area inflation is being driven primarily by energy prices, which rose by as much as 14.3% year on year in July. Prices of food, alcohol, and tobacco increased by 1.6%.

China’s economy is starting to slow

As noted in the introduction, European economies are recovering from the pandemic recession more slowly than China and the United States, where the recovery was not interrupted by the second wave of the virus.

China’s economy experienced only one quarterly contraction after the outbreak of the pandemic, in Q1 of last year. Since then, it has been expanding continuously. Year-on-year GDP growth in Q1 reached a record 18.3%, also due to base effects. In Q2 it was 7.9%. Quarter-on-quarter figures are less striking, but growth can still be described as solid.

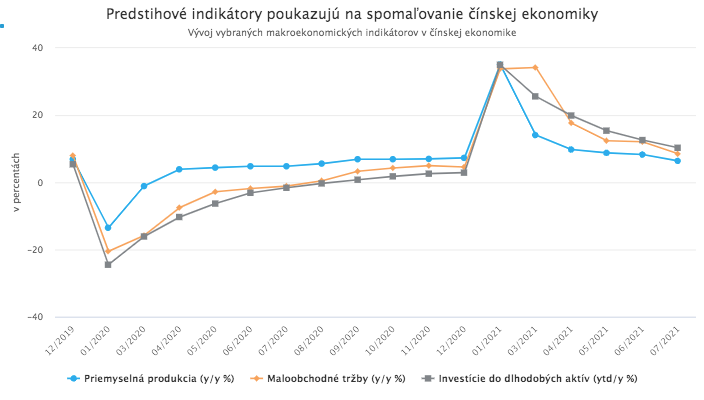

In recent months, however, China’s economy has accumulated several imbalances and risk factors. These include weak domestic consumer demand and stagnant wages, which, unlike industrial output, have not fully recovered from the pandemic; a sharp increase in input commodity prices faced by producers; and targeted credit tightening. In recent weeks, these growth headwinds have been compounded by aggressive regulatory crackdowns by Beijing on domestic technology firms and the spread of the Delta variant.

China continues to pursue a zero-tolerance policy toward Covid-19 and imposes drastic measures with negative economic effects even in response to a small number of cases. Last week, it partially closed the world’s third-busiest container port following the detection of a single asymptomatic coronavirus case.

The combined negative impact of these factors is now starting to show up in China’s economy. Early this week, new readings of three important leading indicators were published. All came in well below expectations and point to a slowdown. This impression is reinforced by political signals. It therefore appears that China has already moved past the phase of rapid post-pandemic recovery.

Inflation and Delta concerns are also weighing on the US economy

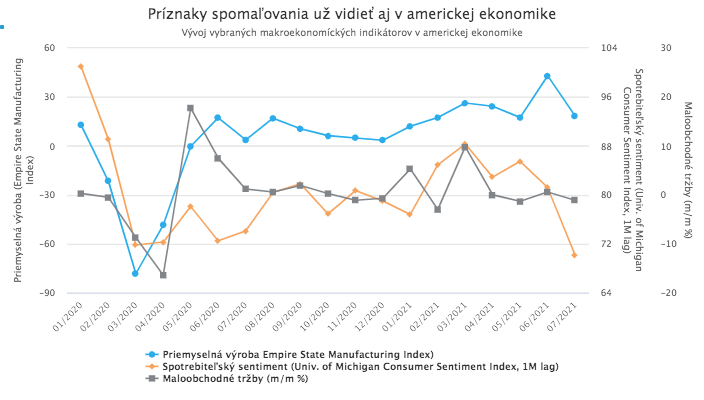

Signs of slowing are now visible in the US economy as well. A trio of important leading indicators released this week also came in significantly below expectations, much like in China. The consumer sentiment index, in particular, was disastrous, falling to its lowest level since 2011. Weak retail sales figures suggest that negative consumer sentiment is already spilling over into the real economy. Economists expected retail sales to decline by 0.3% in July; the actual figure was -1.1%.

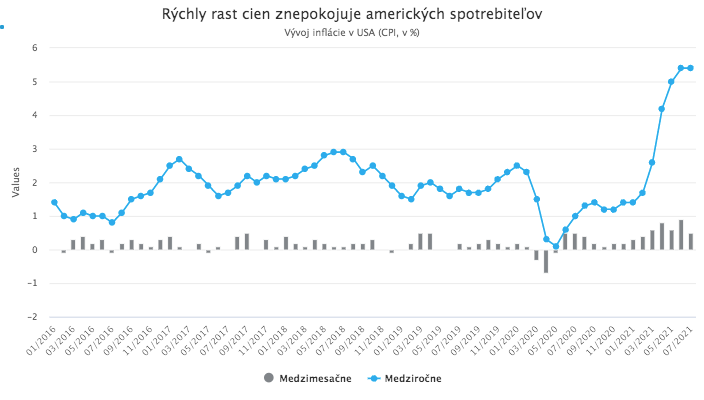

In addition to Delta-variant concerns, deteriorating sentiment among US consumers is being driven to a significant extent by rising prices. The United States recorded a sharp rise in inflation over the course of this year, with the first signs of moderation appearing only last month. However, consumer price growth is still running at a year-on-year pace of 5.4%, a level that until recently would have been difficult to imagine.

Part of this increase is, as the Fed argues, likely driven by transitory factors that will fade within a few months. The problem, however, is that no one can say with certainty which inflationary pressures will prove transitory, and it is also unclear whether a Delta wave may turn some temporary factors into more persistent ones. July data, for example, showed that used car prices, which had surged in recent months and driven the index higher, have stabilized. Given current challenges facing Asian automakers, however, a renewed increase cannot be ruled out. Price growth for food and restaurant meals, meanwhile, has not eased at all. It is therefore understandable that persistent inflation is unsettling consumers and dampening demand.

The world’s two largest economies are therefore currently showing concerning signs of slowing. This is also a problem for European economies. There is a risk that their recovery will be curtailed before it has had the chance to fully gain momentum.