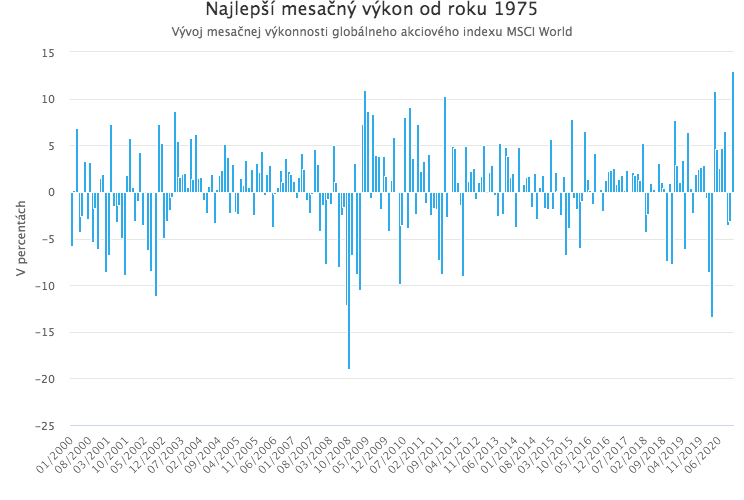

Stock Markets Are Having Their Best Month Since 1975

The procyclical rotation whose start we pointed out two weeks ago is continuing in full force. Global equities (measured by the MSCI World index) recorded their strongest monthly gain in November in 45 years. Some European stock markets even posted the best monthly performance in their history.

The MSCI World equity index, which measures the performance of stocks across 23 of the world’s most developed economies, is heading for its best monthly performance since 1975. Since the beginning of November, it has gained almost 13%. The driver of this strong rally is a massive procyclical rotation, whose onset we highlighted two weeks ago.

It was triggered by news of a promising coronavirus vaccine from Pfizer and BioNTech. This positive information sparked hope in markets that the end of the pandemic is already in sight and that economies around the world will begin to recover fully next year. Positive sentiment was then further supported by encouraging clinical-trial results for other promising vaccines from Moderna and AstraZeneca.

At the start of this week, equities were also helped by positive political news. Trump instructed his administration to begin the transition process to Biden, effectively acknowledging his election defeat. This eased fears that the transfer of power would not be calm and democratic. At the same time, information emerged that Biden plans to nominate former Fed Chair Janet Yellen as Treasury Secretary. It is expected that Yellen will form a strong team with current Fed Chair J. Powell and ensure effective coordination between the Treasury and the Fed in supporting the economic recovery.

Finally, as usual, technical factors also played a role. The easing of uncertainty around the U.S. election, and the related decline in volatility, triggered a large mechanical inflow of money into equity markets from institutional investors over the course of the month.

Records in Europe and Japan

The record November stock-market rally has the character of a procyclical rotation. That means it has favored primarily those stocks, sectors, factors, and regions that are most sensitive to developments in the real economy and therefore benefit most from growing hopes of restarting economic growth. Since these very same types of stocks had lagged the broader market in recent months and years, this can also be viewed as a catch-up move.

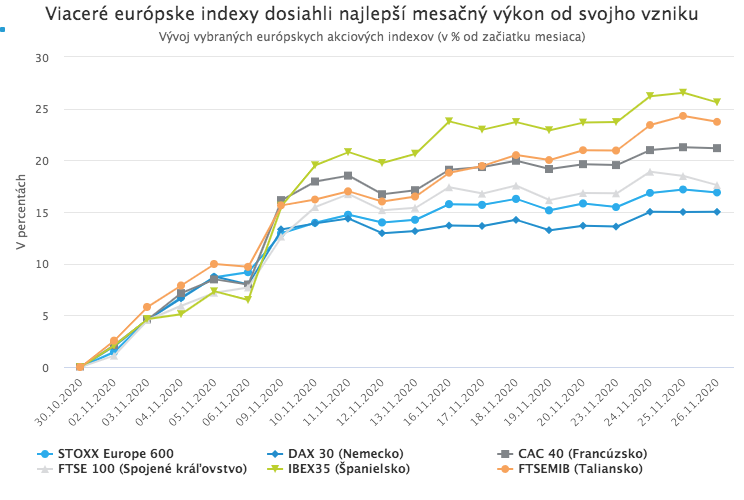

It is therefore not surprising that, from a regional perspective, the strongest gains in November were recorded by European equities, which, unlike U.S. equities, still have not fully erased their March losses and have lagged behind them over the longer term. The pan-European STOXX Europe 600 index posted its strongest monthly gain since its inception. Since the beginning of the month, it rose by as much as 16.9%. French, Spanish, and Italian stock markets did even better, with more than 20% monthly gains, also the best in their history.

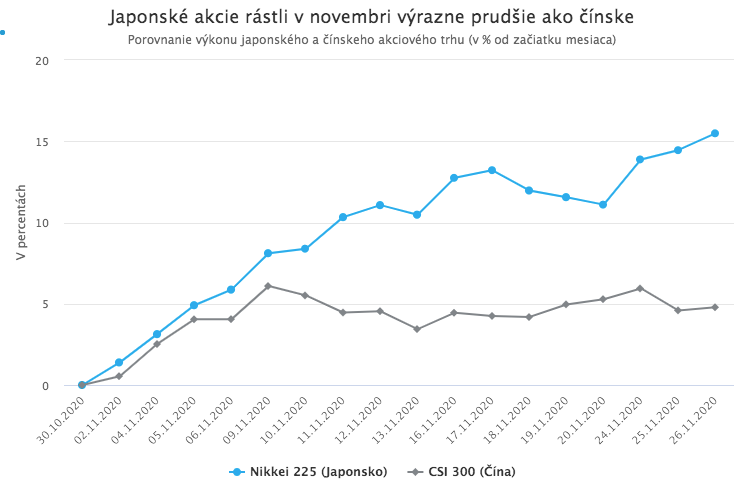

The Japanese stock market also recorded a strong gain of nearly 16%, its best monthly performance since January 1994. This is in sharp contrast to the Chinese stock market’s rise of only 5%.

The reason for this marked performance gap between the two largest Asian stock markets also lies in the procyclical character of the current rally. The Japanese stock market is simply catching up, much like Europe. Chinese equities have little to catch up on, since they erased their March losses long ago, and their initial declines after the outbreak of the pandemic were not as large as those in Japan or Europe.

30,000 points

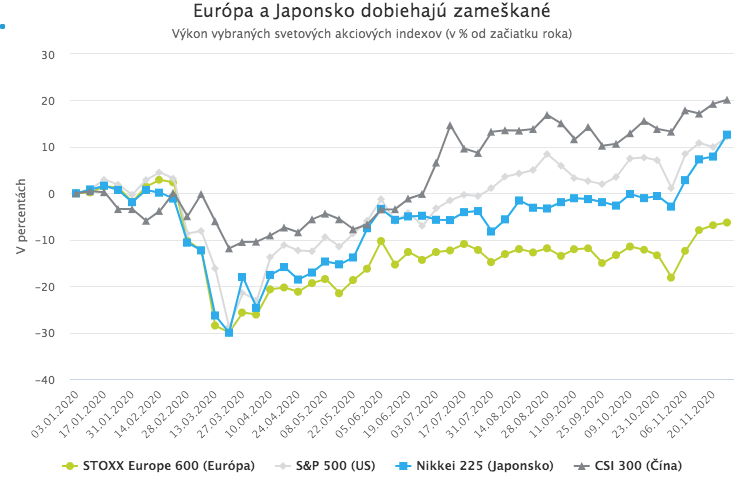

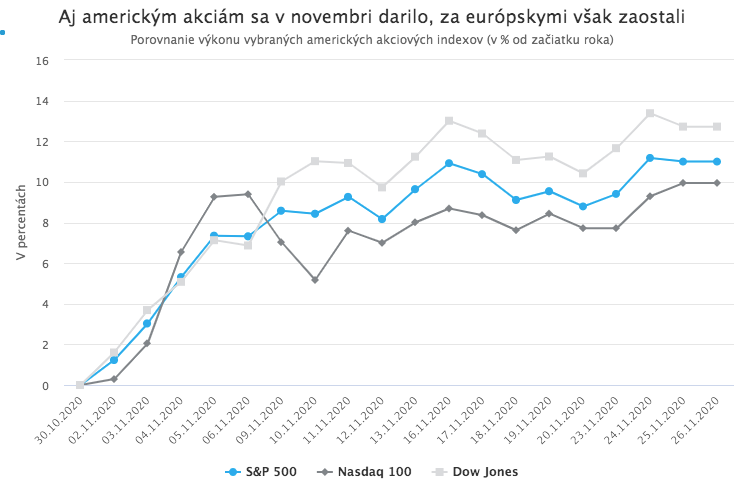

U.S. equities also posted an exceptionally strong gain in November, although they lagged not only European and Japanese equities but also their own performance in April of this year. Among the three most important U.S. stock indices, the best performance came from the long-lagging industrial Dow Jones index. The technology-heavy Nasdaq 100, the strongest U.S. index over the long term, significantly underperformed.

By the way, thanks to the strong rally, the Dow Jones crossed the 30,000-point level this week. This number, of course, has no inherent meaning by itself; what matters is percentage performance. President Trump, however, held a bizarre 60-second press conference praising the achievement of the “sacred 30,000-point level” and thanking members of his administration for the success.

The paradox is that the Dow reached this milestone on the very day Trump ordered his administration to begin the transition process to Biden and Biden announced his nominee for Treasury Secretary, whom Trump had previously fired as Fed Chair. Trump’s pre-election warnings that the stock market would collapse immediately after a Biden victory clearly did not materialize.

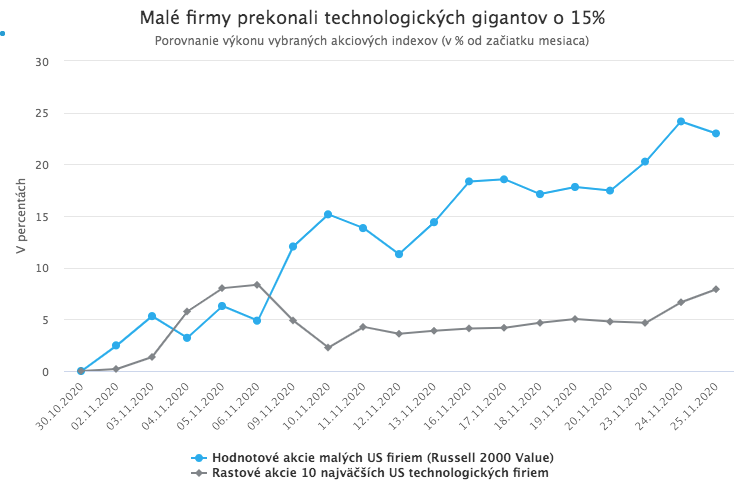

Small-cap stocks beat tech giants by 15%

Differences in performance across regional indices reflect, to a large extent, differences in their sector and factor composition. Procyclical rotation benefits primarily smaller companies in cyclical sectors and value stocks. Its “victims,” by contrast, are shares of large, growth-oriented companies in defensive sectors that had enjoyed exceptionally strong gains in previous months and years. These include above all the largest U.S. technology companies.

Value stocks of the smallest publicly traded U.S. companies outperformed the shares of the 10 largest U.S. technology firms by an astonishing 15% this month.

It is precisely the high weight of the largest technology companies that explains the Nasdaq’s underperformance relative to other U.S. indices, especially the industrial Dow Jones. The large share of cyclical sectors such as industry and finance in European equity indices, and the smaller market capitalization of European companies, in turn largely explains the record November performance of several European stock indices.

A slowdown or continuation of the rally?

Toward the end of the month, the record November rally showed some signs of slowing. A series of weaker economic data may have played a role, as well as funds whose mandates require maintaining a fixed equity allocation. Many such funds rebalance portfolios monthly. After a month of exceptionally strong equity gains that sharply increased the value of the equity portion of their portfolios, they must sell equities at month-end to bring the equity allocation back to its original level at the beginning of the month. JPMorgan estimates the volume of these month-end selling flows at USD 160 billion.

However, the equity rally has a good chance of continuing after a brief pause in December, although likely at a somewhat more moderate pace. Positive sentiment and optimistic expectations persist in markets, volatility dynamics support inflows from large institutional investors, and additional upside momentum could be provided by the Fed and the ECB through a possible expansion of quantitative easing programs at their December meetings, or by further positive news about coronavirus vaccines.