The Turkish Lira Is Weakening Sharply Again

Central banks in the world’s largest economies are still holding off on raising interest rates despite rapidly rising inflation. Central banks in smaller and emerging economies, however, cannot afford such a “luxury” of waiting, and most of them have already moved to raise rates quickly. Many of these countries have a long-standing inflation problem, a weak currency, are vulnerable to outflows of foreign capital, and their central banks lack sufficient credibility. If, therefore, they do not respond quickly to any more significant increase in inflation, they risk rapid capital outflows, a sharp weakening of the currency, and an inflationary spiral driven by “unanchored” inflation expectations. Central banks in these countries also typically seek to maintain a positive interest-rate differential relative to developed economies in order to remain attractive to foreign investors, and therefore in principle raise interest rates earlier than the central banks of the largest economies do. Turkey is an exception in this respect. The Turkish central bank is currently not raising interest rates but, on the contrary, lowering them, despite inflation in the country reaching almost 20%. The Turkish lira is paying the price.

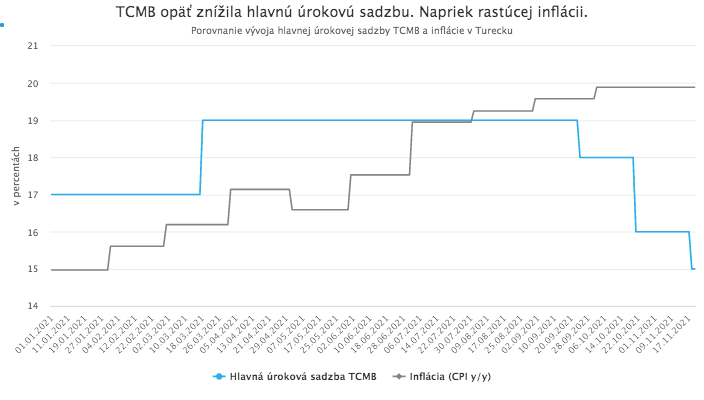

Another rate cut amid rising inflation

The Turkish central bank (TCMB), under Governor S. Kavcıoğlu, proceeded last week with another rate cut, by 1%. This is already the third consecutive rate cut, which has pushed the country’s main policy rate from 19% at the beginning of September to the current 15%.

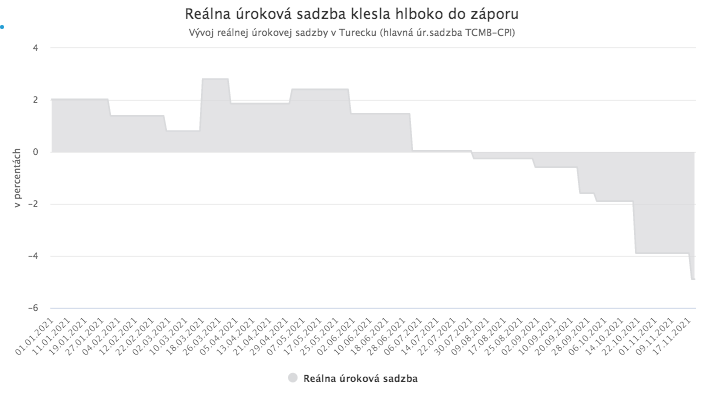

A main policy rate at the level of 15% still appears extremely high at first glance, especially compared to current interest rates in the euro area or the United States. The problem, however, is that inflation in the country rose in October to 19.89% year on year and continues to increase. This means that the real interest rate in the country is close to -5%.

Such a deeply negative real interest rate naturally cannot motivate investors to buy Turkish securities or invest in Turkish lira instruments instead of far safer euro- or dollar-denominated securities. That is also why the Turkish lira responded to this rate cut with another sharp depreciation and continues to fall, so to speak, in free fall. In addition to the rate cut itself, investors were also alarmed by the central bank’s accompanying statement, which essentially downplayed the problem of high inflation in the country and left room for further rate cuts in the future. President Erdogan also added fuel to the fire, repeating his stance on interest rates in a speech in parliament the day before the central bank meeting. He said that he “cannot be on the same path with those who defend interest.” He also pledged to “relieve the people of the burden of interest” and to “continue the fight against interest.” There is little doubt that the central bank cut rates the next day precisely at Erdogan’s wish or instruction.

Unusual theories about the relationship between rates and inflation

It is precisely Erdogan’s economic theories (especially regarding interest rates) and his influence over the central bank that explain why the Turkish lira has been depreciating sharply for the ninth year in a row. President Erdogan holds “unorthodox” economic views, according to which rising inflation should not be fought by raising rates, as standard economic theory argues, but rather by lowering them. It should be noted that some serious, though more fringe, schools of economics also question the effectiveness of rate hikes in fighting inflation, but only in the case of large, monetarily sovereign economies with strong currencies, such as the United States. Turkey, as an emerging economy that has a chronic problem with high inflation, low central-bank credibility, a volatile currency, deficits, high private-sector indebtedness in foreign currencies, and a need for foreign capital inflows, has no choice. Standard economic theory regarding the relationship between inflation and interest rates simply applies in its case, and practice confirms it. Erdogan, however, is adamant. He considers interest rates the “mother and father of all evil” and continually pushes for lower rates while simultaneously seeking to stimulate the economy through credit expansion. The result is persistently high inflation and a constantly weakening lira.

President Erdogan blames the consequences, in the form of high inflation and a weak lira, on dark foreign forces that want to harm the Turkish economy, and lowering interest rates is one of the main points of his political campaign. Formally, the central bank is of course responsible for the level of interest rates and currency stability. As several governors have learned in recent years, in Turkey the central bank is independent only on paper, and Erdogan has the final say. Governors who did not respect this quickly lost their jobs. Those who did respect it but caused predictable problems by cutting rates also lost their jobs. It is highly likely that the same fate awaits S. Kavcıoğlu.

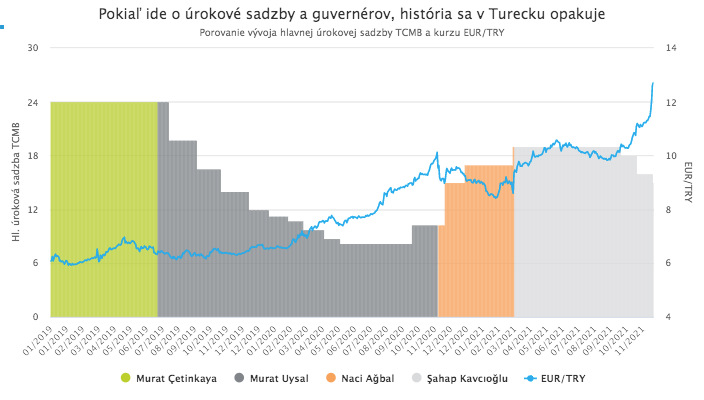

History repeats itself

Şahap Kavcıoğlu, the current governor of the Turkish central bank, is already the fourth in two and a half years. He was appointed in March of this year after his predecessor, Naci Ağbal, raised the policy rate by 2%, which clearly angered Erdogan and earned him an immediate dismissal. Ağbal’s task was to stabilize the rapidly weakening lira, which he indeed managed to do. Erdogan apparently felt, however, that he had gone unnecessarily far with the rate hikes. Investors had expected only a 1% rate increase ahead of the TCMB meeting that turned out to be Ağbal’s last. A 2% increase was too much. Ağbal had been appointed after the dismissal of the previous governor, Murat Uysal, who faithfully fulfilled Erdogan’s wishes and cut rates by a record 15.75% over 10 months, which quite predictably resulted in a sharp depreciation of the lira, for which he was ultimately dismissed. Murat Uysal had in turn replaced the previous governor, Murat Cetinkaya, in July 2019. Cetinkaya managed to curb inflation and stabilize the lira through persistent rate hikes, but subsequently did not cut rates quickly enough to satisfy Erdogan, and so he was replaced by Uysal.

History has thus been repeating itself in Turkey in recent years. It is therefore not difficult to imagine that the current governor Kavcıoğlu will end up similarly to Governor Uysal and will soon be dismissed for the current sharp depreciation of the lira, which is a predictable and logical consequence of obedient rate cuts amid rising inflation. His successor will then proceed with a modest rate increase, but as soon as the situation stabilizes, he will again be replaced by someone who quickly cuts rates.

Another recurring reaction by President Erdogan, in addition to dismissing central bank governors, is raising political tensions vis-a-vis foreign countries. Whenever the lira weakened sharply in recent years, Erdogan triggered some geopolitical or diplomatic conflict, which temporarily deepened the lira’s decline, but then calmed the conflict, triggering a “relief rally” that strengthened the lira to a level stronger than it had been before the conflict began. It is likely that Erdogan will resort to this proven recipe again in the coming days. If he manages to carry out this “maneuver” successfully once more, the lira may erase part of its current sharp losses in the coming weeks. Over the longer term, however, it is likely to face further persistent depreciation accompanied by periods of heightened volatility.