Will the Dollar Continue to Strengthen?

In the first weeks after the coronavirus pandemic erupted, the U.S. dollar was virtually the only major currency that strengthened amid the global panic. Once the initial shock faded, however, the trend reversed and the dollar spent most of last year weakening. That move reflected a calmer backdrop supported by a flood of dollar liquidity, which stabilized riskier currencies; renewed optimism about the euro; and later, rising hopes that the global economy was entering a recovery phase. In theory, a reopening-driven upswing should benefit higher-beta emerging-market currencies that investors had shunned during the most uncertain months.

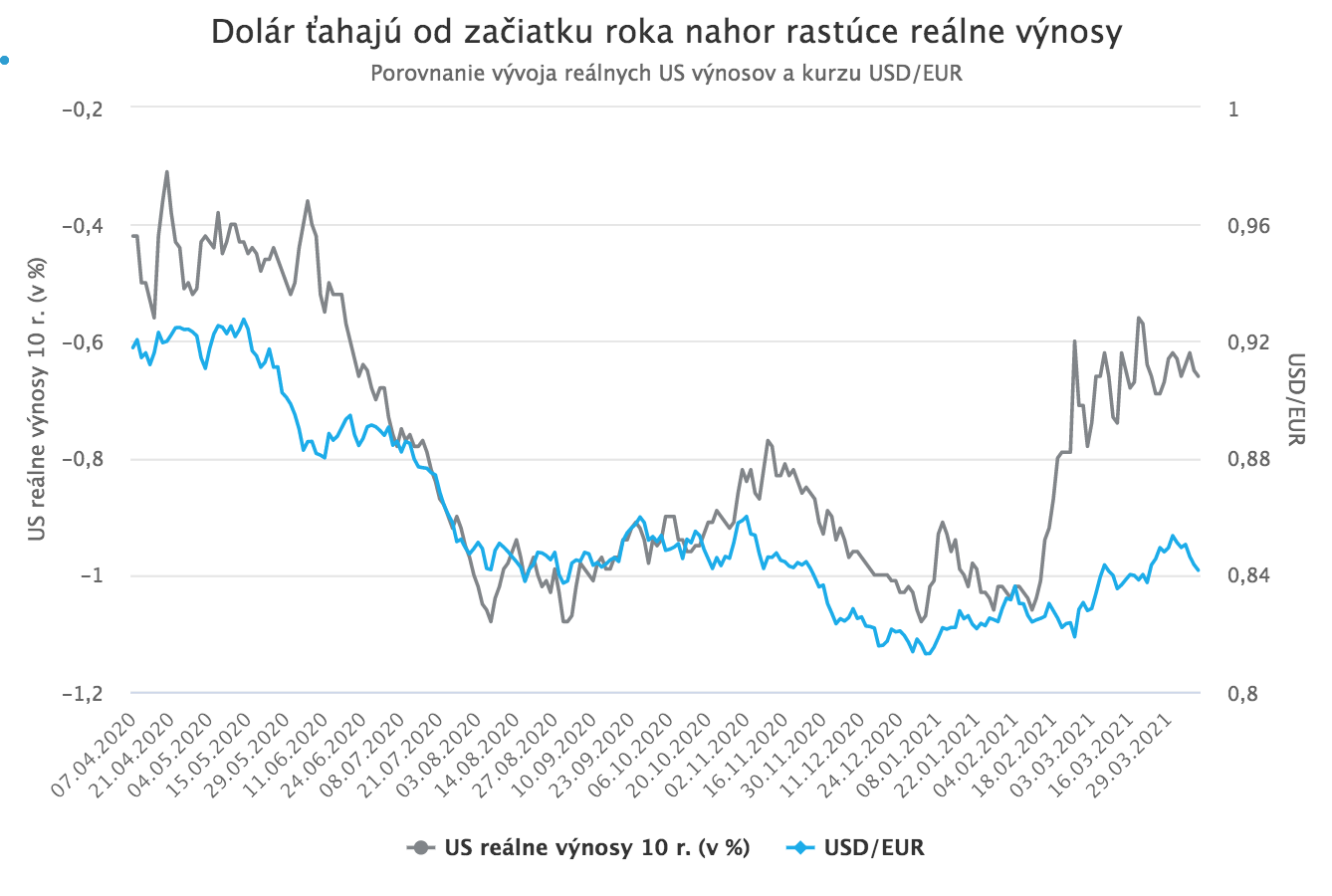

For these reasons, many major investment banks and analysts expected the dollar’s depreciation to extend into 2021. So far, the opposite has happened. Since the start of the year, the dollar has strengthened markedly, and there are few signs that the rally is losing momentum. The current upturn is being driven by the rapid rebound of the U.S. economy, which is pushing real yields higher.

The key question is whether the dollar can keep appreciating in the months ahead, or whether earlier forecasts will ultimately prove right and the currency will resume weakening.

A stronger economy and faster vaccinations support the dollar

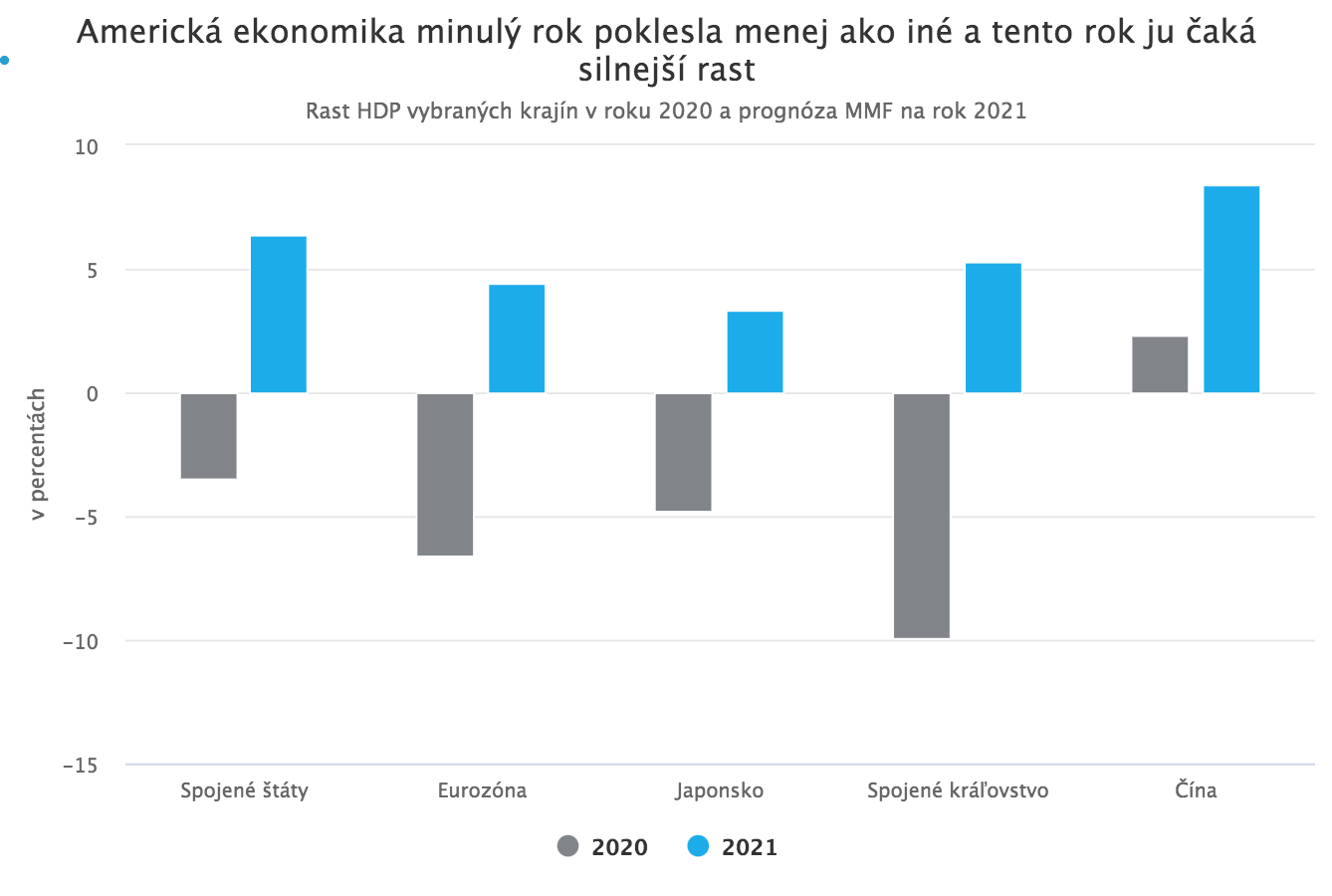

The strongest argument for further dollar gains is the expectation that the U.S. economy will outperform most peers. Last year, the U.S. suffered a smaller contraction than other major economies (with China as the notable exception), and this year it appears poised for significantly faster growth. The International Monetary Fund is forecasting U.S. GDP growth of 6.6%.

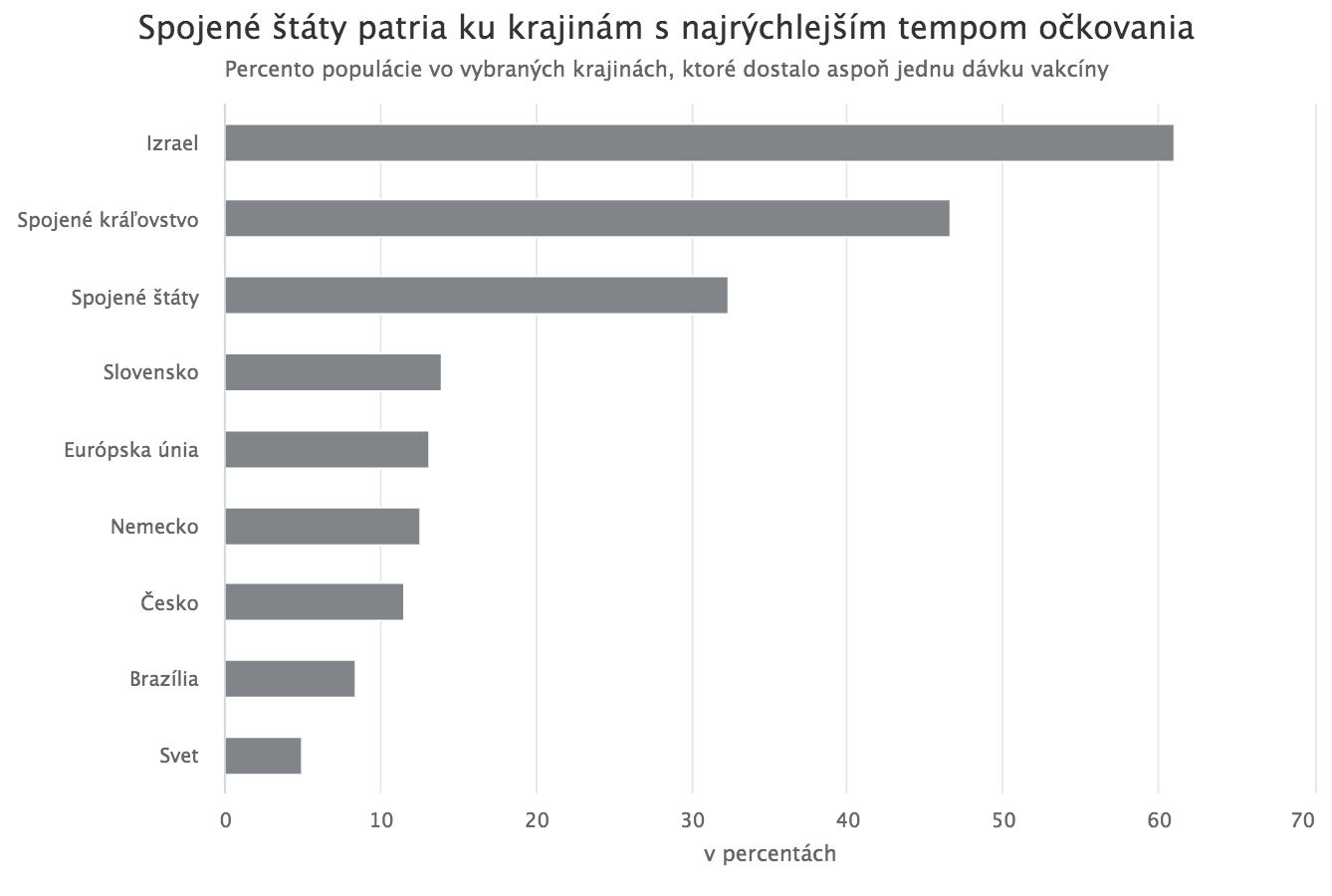

The U.S. is currently benefiting from massive fiscal support aimed at sustaining economic activity and consumer demand, as well as from a rapid vaccination rollout. The daily average number of vaccinations has recently reached around three million, and it is plausible that within weeks the country will have vaccinated the entire adult population willing to receive the shot. The pace stands in sharp contrast to the slower rollout in Europe and in most developing economies.

Faster vaccinations reinforce expectations that the U.S. economy could reopen fully before summer. Pandemic-weary consumers, many of whom remain in relatively solid financial shape thanks to extensive government support, may then begin to spend accumulated savings. Add to this the recently unveiled USD 2.25 trillion infrastructure plan proposed by President Joe Biden, along with discussions around partial student-debt forgiveness, and the result is a plausible recipe for a powerful growth impulse.

A growth differential of this kind, especially if it contrasts with a still-fragile recovery in Europe and elsewhere, would naturally attract capital toward the United States and raise demand for dollars. Moreover, a rapid rebound combined with higher inflation could force the Federal Reserve to raise rates earlier than other central banks. Higher U.S. rates would likely lift real yields further and add to upward pressure on the currency.

Inflation and deficit concerns

The same forces that currently support the dollar also have a downside. Under certain conditions, they could instead weaken the U.S. currency. Strong growth, a surge in consumer spending, and large-scale public outlays can easily translate into a faster rise in inflation. Even if inflation were to move above the Fed’s 2% target, the central bank would not necessarily respond immediately with rate increases, especially if doing so risked derailing the recovery.

Indeed, the Fed’s new framework, known as “average inflation targeting,” explicitly allows inflation to run above 2% for some time. This raises the risk that inflation could accelerate more than expected while the Fed remains behind the curve, a scenario that would likely weigh on the dollar.

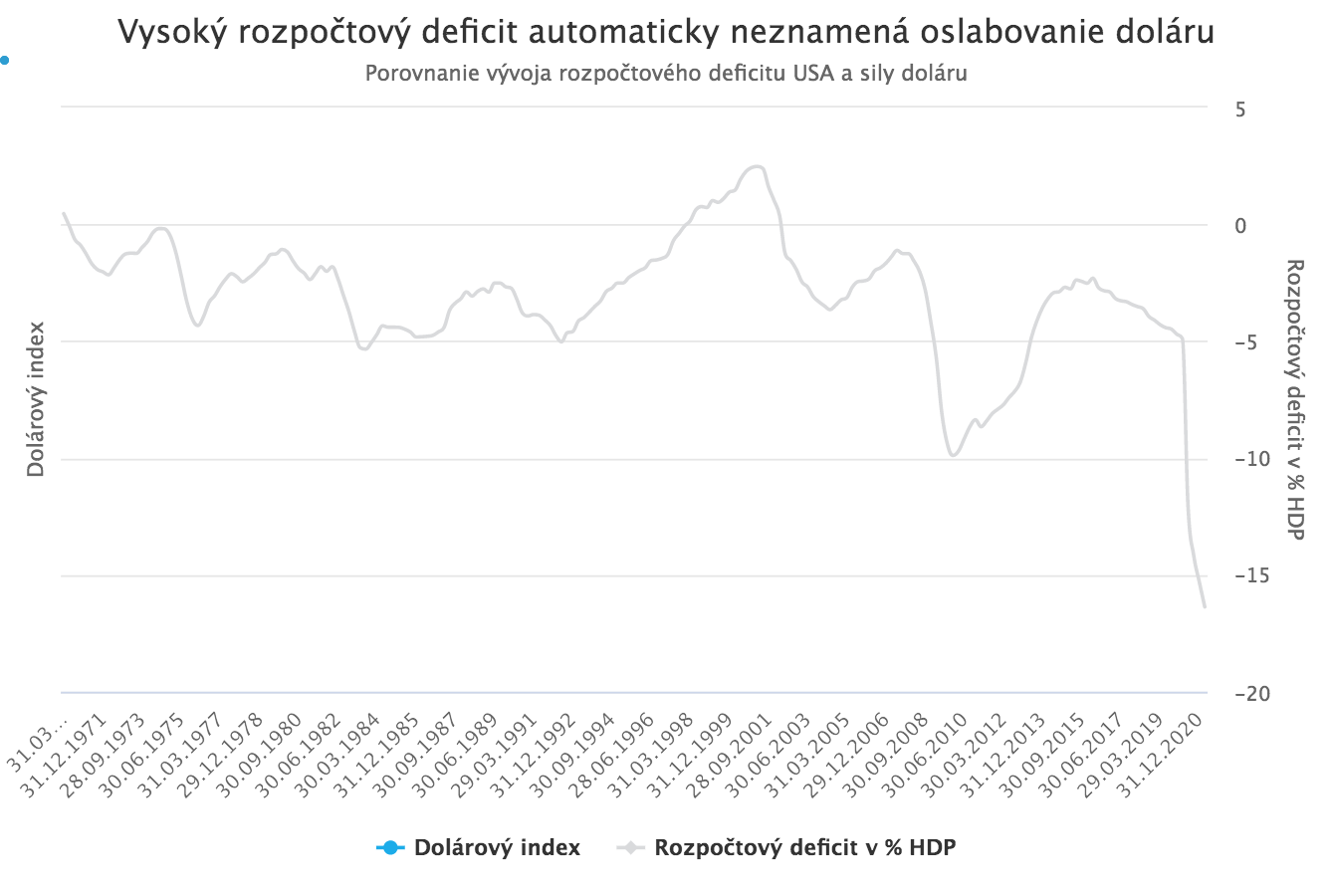

The U.S. economy’s relatively strong performance last year and its rapid recovery this year are also closely tied to an unprecedented volume of fiscal stimulus. That inevitably implies a persistent rise in public debt and a widening budget deficit. In standard textbook terms, large deficits can put downward pressure on a currency.

This, however, is not a mechanical relationship. What matters is also the origin and quality of the deficit. If higher government spending stimulates demand, raises long-term productive capacity, and strengthens medium-term growth expectations, it does not automatically weaken the currency, particularly in a monetarily sovereign economy that issues what is effectively the world’s reserve currency.

Should we worry about catastrophic scenarios?

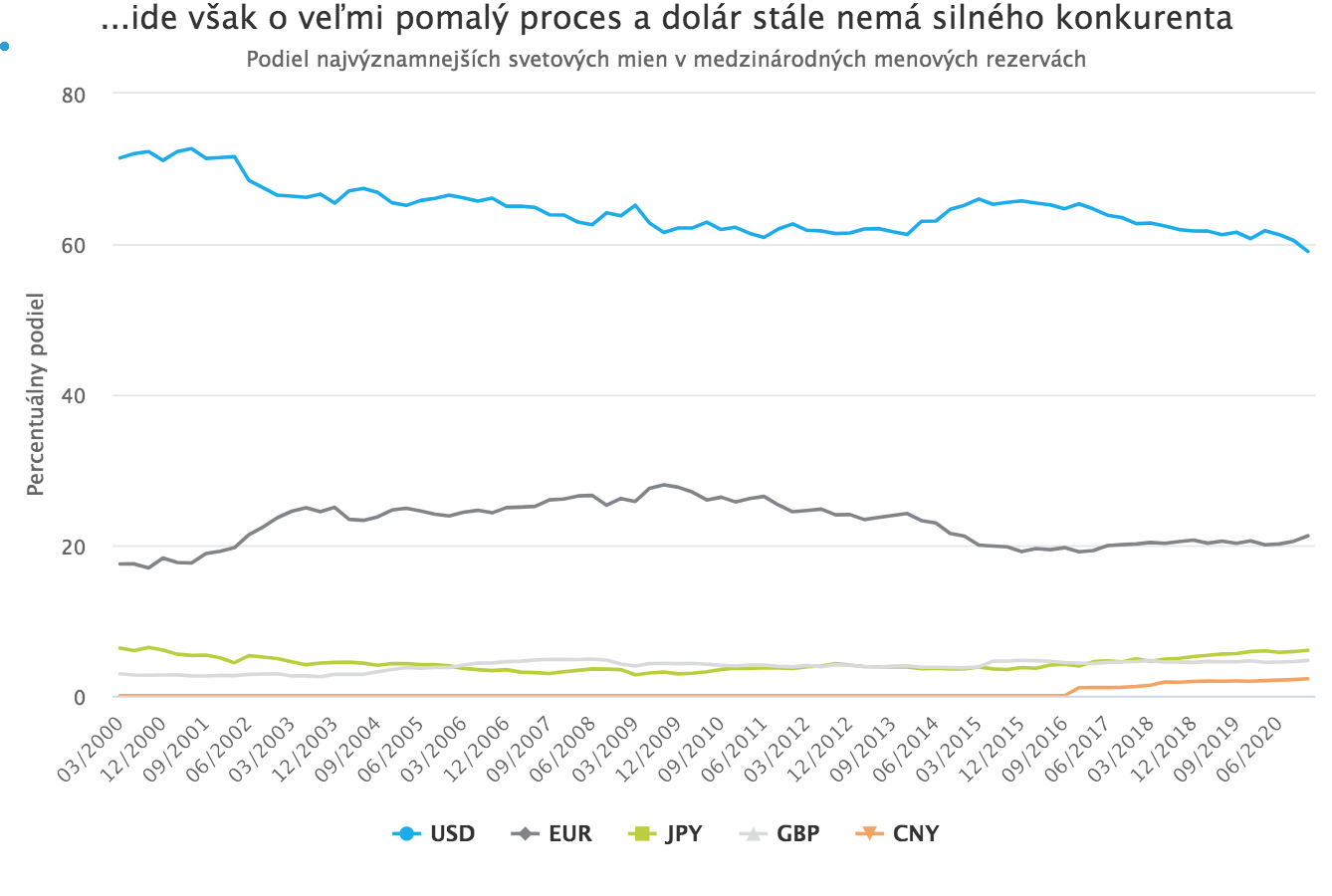

Rising U.S. debt alongside the Fed’s aggressive liquidity provision has led a small but vocal segment of investors to predict a collapse in confidence in the dollar, the end of its dominant role in the global financial system, and even hyperinflation. These arguments often cite the fact that the dollar’s share of global foreign-exchange reserves has fallen in recent months to its lowest level since 1995. Plotted with the “right” scale, the decline can look dramatic.

In practice, however, shifts in the international monetary system occur at a glacial pace. The dollar still has no credible rival. Despite the recent decline in reserve share and the broader reassessment of U.S. monetary-policy priorities, a meaningful loss of the dollar’s global status in the foreseeable future appears highly unlikely.

Catastrophic narratives also include warnings of “incoming hyperinflation” due to excessive “money printing.” These fears, whether sincerely held or often used as marketing to sell gold or cryptocurrencies, do not appear justified at present. A short-term rise in inflation above the Fed’s 2% target is certainly possible, as discussed above, but that would still imply single-digit inflation marginally above 2%, not double-digit or runaway price growth.

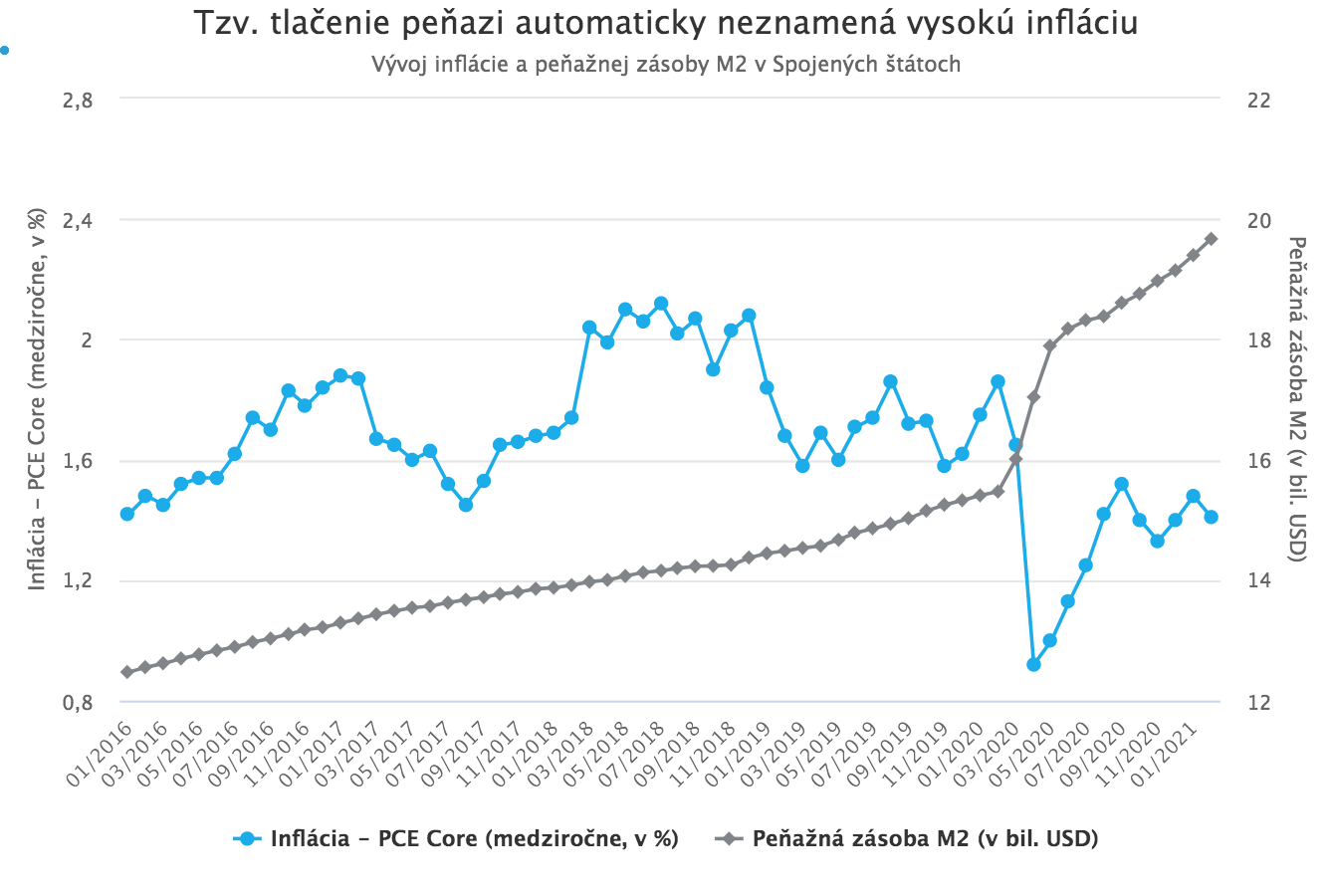

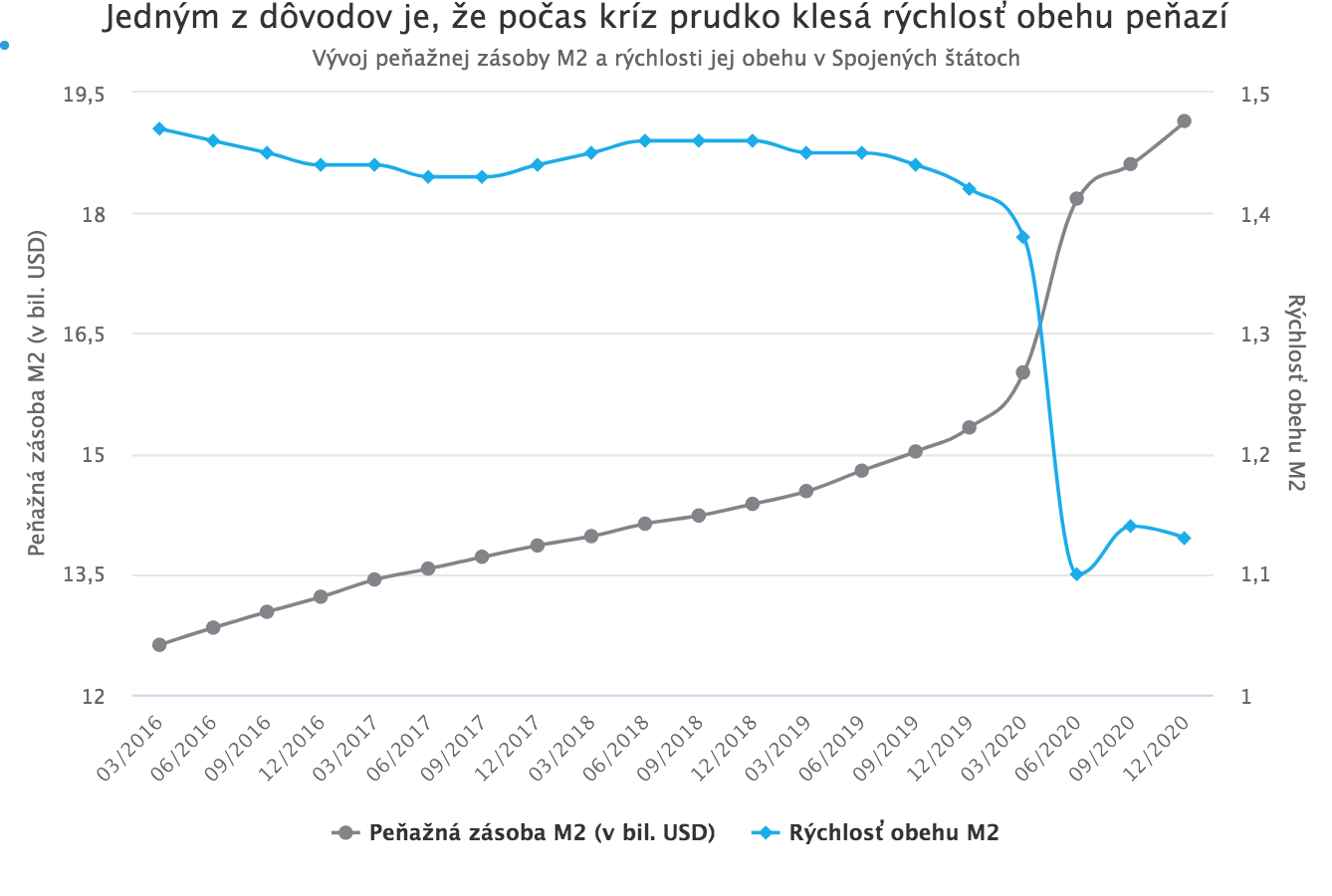

Money supply measures in the U.S. have indeed risen sharply over the past year due to abundant Fed liquidity, but an increase in the money supply does not automatically translate into inflation. Inflation is a complex phenomenon shaped by the interaction of many factors. The size of the money supply is only one input, and by itself proves little.

High inflation typically emerges in economies that are structurally damaged and where the central bank lacks credibility. The United States is clearly not such a case. The Fed’s preferred inflation gauge remains well below the 2% target despite the jump in monetary aggregates.

In short, catastrophic dollar scenarios currently look unjustified and extremely unlikely. The most probable baseline remains further dollar strength, driven by stronger U.S. growth relative to other developed economies and rising U.S. real yields. A trend reversal could occur if the recovery in other advanced economies, especially the euro area, accelerates meaningfully, or if the Fed fails to respond in time to a more pronounced inflation upswing in an overheating economy.