A Promising COVID-19 Vaccine Lifted Market Sentiment

News of exceptionally strong late-stage clinical trial results for a potential COVID-19 vaccine developed by Pfizer and BioNTech sparked euphoria among investors as well. The resulting wave of optimism triggered a powerful pro-cyclical rotation across markets. Here is which assets have benefited, and which have suffered.

The vaccine developed by Pfizer in cooperation with German biotech firm BioNTech achieved 90% efficacy in a Phase 3 trial involving 43,500 participants. This is highly encouraging, as the relationship between vaccine efficacy and the share of the population that must be immunized to achieve herd immunity is nonlinear and inverse. In short, the more effective the vaccine, the fewer doses need to be produced, distributed, and administered to vaccinate the population.

This raises hopes that the pandemic could be brought under control over the course of next year. Emergency use authorization by the FDA could arrive as early as December. If everything proceeds according to plan, the first 50 million doses will be produced by year-end, followed by up to 1.3 billion over the course of next year. Each person will require two doses.

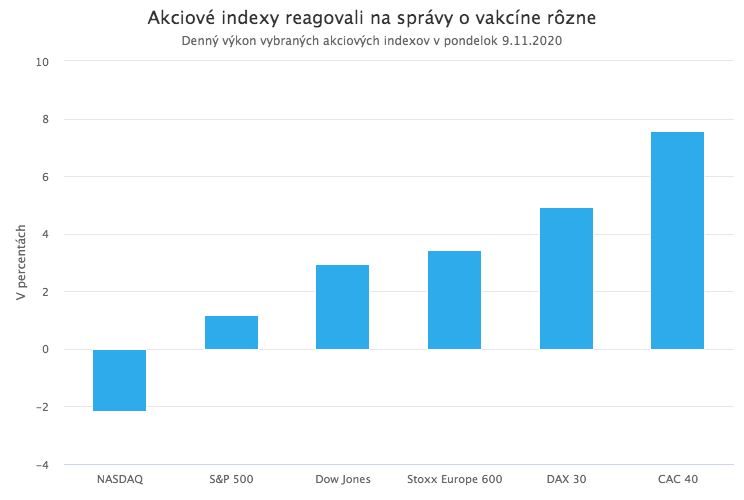

Pfizer and BioNTech announced the strong trial results and outlined next steps on Monday, 9 November, in an official press release. The surge in optimism immediately spilled over into financial markets. Several equity indices recorded one of their strongest single-day performances in history.

A quick look at Monday’s markedly divergent performance across major indices, however, reveals that the vaccine news did more than simply lift equities broadly. It also set in motion a significant and potentially long-lasting market dynamic spreading across asset classes: a powerful pro-cyclical rotation.

A promising vaccine ignites a massive pro-cyclical rotation

In brief, a pro-cyclical rotation describes an environment in which market conditions begin to favor assets that benefit from a re-acceleration in economic growth. This typically includes small-cap equities in cyclical sectors, value stocks, and higher-risk credit. These assets then outperform defensive, “bad-weather” exposures such as large-cap non-cyclical equities, growth stocks, high-quality duration assets, and precious metals.

Cyclical rotations often begin after a major catalyst that materially improves expectations for the macroeconomic outlook. This year, markets have seen several attempts at a pro-cyclical rotation, yet each one ultimately faded early. The latest attempt emerged ahead of the US election on expectations of a “blue wave,” but quickly dissipated after the vote as it became clear Democrats were unlikely to secure a Senate majority.

The rotation that began on Monday is different, not only because it was triggered by a genuinely consequential event that could bring the pandemic and its associated economic disruption to an end in the near future, but also because of its sheer intensity, strong enough to challenge historical records.

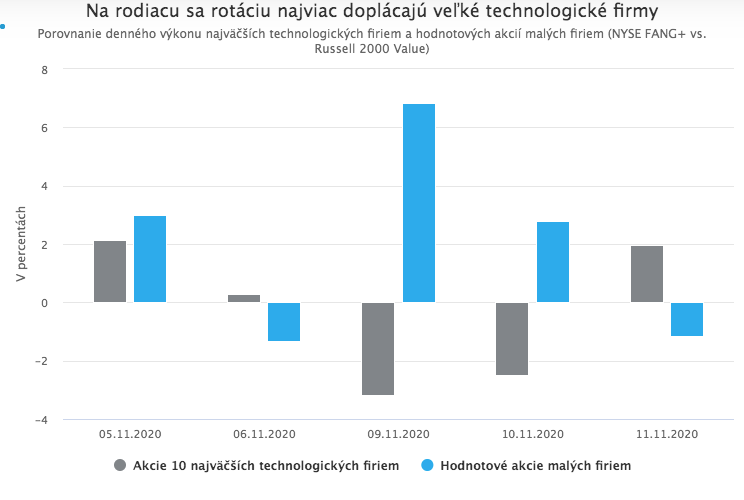

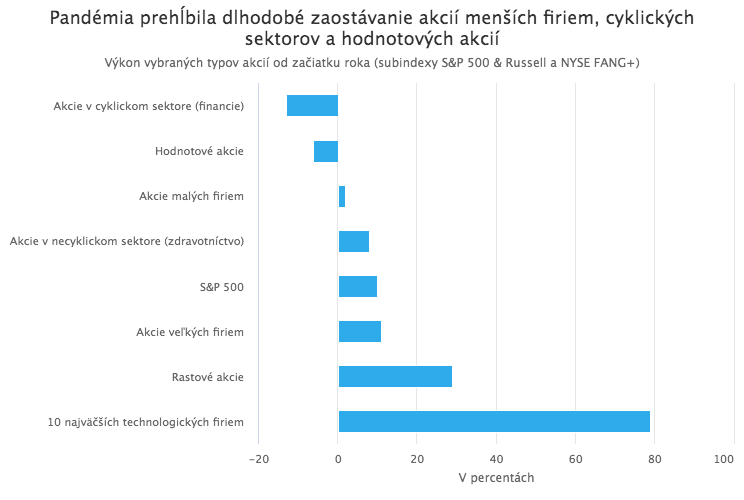

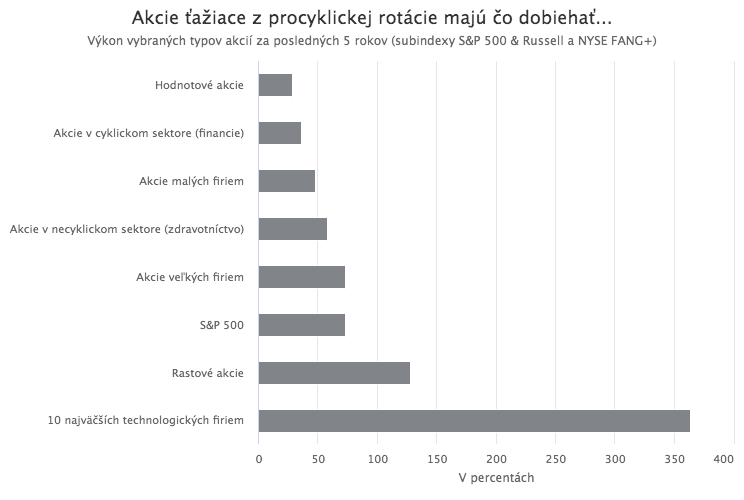

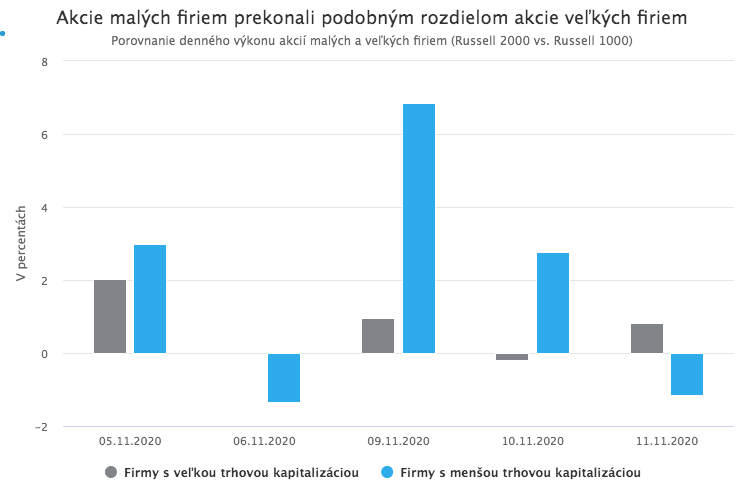

In equities, the early phase of this pro-cyclical rotation manifested in sharp gains for small caps, cyclical sectors, and value stocks. In other words, it favored precisely the parts of the market that have lagged for years, and whose underperformance deepened after the onset of the pandemic.

In that sense, the rotation is largely a catch-up move. And after years of dispersion, there is a great deal of catching up to do.

The “losers,” by contrast, have been large, growth-oriented companies in defensive sectors that have enjoyed a remarkably strong run in recent months and years, above all the mega-cap technology names such as Apple, Amazon, Microsoft, Facebook, and Alphabet (Google).

These companies benefited for years from an environment of slowing growth, low inflation, and declining interest rates. Their business models and near-monopolistic positions allowed them to grow even under challenging macro conditions. The pandemic only reinforced this trend: “big tech” was among the few areas of the market that not only avoided damage, but in many cases benefited from the crisis. From this perspective, the prospect of an economic recovery and a partial return to physical interaction and offline activity (at the expense of virtual activity) is, at least in relative terms, negative news for them.

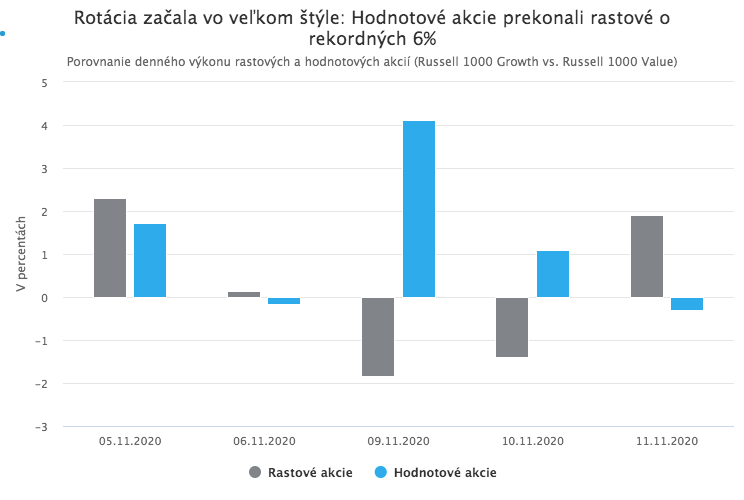

Once expectations shifted on Monday following the vaccine news and the rotation began, the initial moves were truly dramatic. Performance dispersion across equity factors reached extreme levels.

Value stocks outperformed growth stocks by a record 6%. A similarly large gap opened between small caps and large caps.

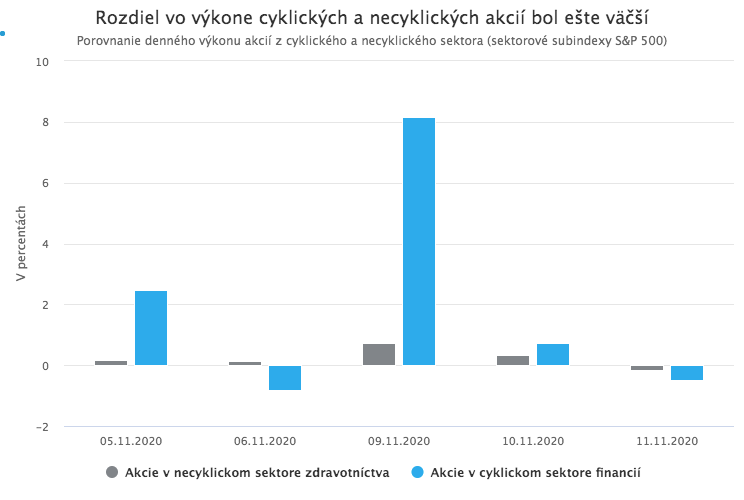

The spread between cyclical and non-cyclical sectors was even more striking. Cyclical financials outperformed defensive healthcare by 9% in a single session.

As noted above, the biggest “victims” of the emerging rotation were the mega-cap technology firms. On Monday, they fell by an average of 3.2%. If we compare their performance with that of small-cap value stocks, which benefited disproportionately, the result is a staggering 10 percentage point performance gap in one day.

In short, the rotation began in emphatic fashion.

Incidentally, the heavy weight of the largest technology companies in US equity indices, particularly the NASDAQ, was a key reason why those indices reacted more weakly, or even negatively, to the otherwise excellent vaccine news mentioned at the outset.

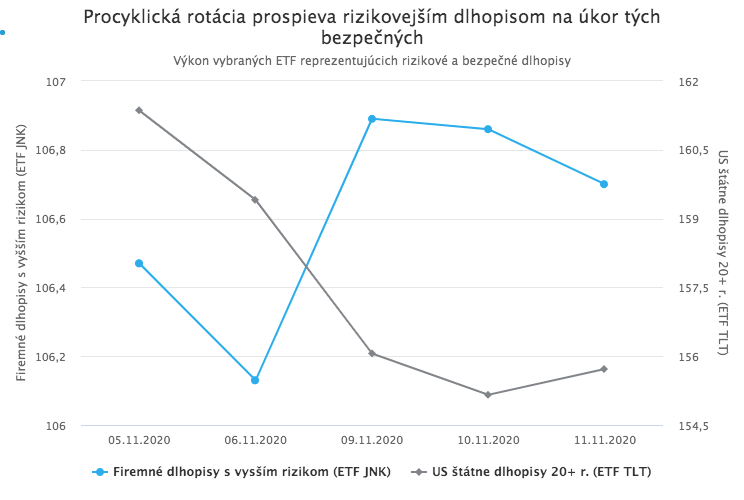

The pro-cyclical rotation is not confined to equities, even if it is most visible there. It is propagating broadly across markets and asset classes. It has also produced particularly interesting moves in fixed income. The rotation favors riskier credit instruments, while its “casualties” are long-duration safe assets that tend to be in demand during periods of elevated risk, weak growth, recession, and falling interest rates, most notably long-maturity sovereign bonds in the most advanced economies. In other words, it marks a sharp reversal of the prevailing trend.

US Treasuries, generally viewed as the safest of safe-haven assets, experienced an unusually steep price decline (and yield increase) early in the week. Speculative-grade corporate bonds, by contrast, rallied, with yields falling to record lows.

The divergence between safe and risky fixed income that accompanied the start of the rotation is well illustrated by comparing the performance of the high-yield ETF JNK and the long-duration Treasury ETF TLT.

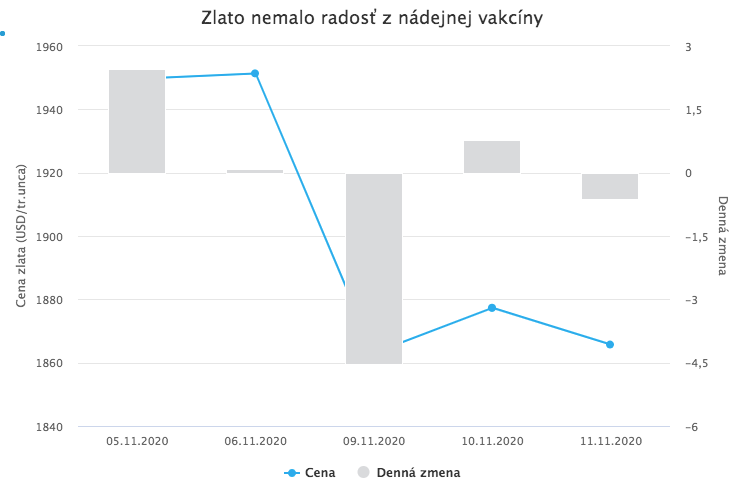

In addition to government bonds, other traditional safe havens also fell. Gold dropped by more than 4% on Monday.

What comes next?

A key question is whether this rotation will, like earlier attempts, stall after a few days, failing to gain traction beyond the initial phase. Yet both the catalyst and the magnitude of the move suggest a higher probability that this time is different.

The vaccine news, which could end the pandemic within a matter of months, was a genuinely powerful impulse. To stop the rotation and reverse the trend, markets would likely require a negative shock of comparable magnitude, one that materially darkens the economic outlook.

Of course, the pandemic is still raging. Vaccine production and distribution could face setbacks, and even under the best-case scenario, the positive effects on the real economy will likely be felt only after several months. Negative news cannot be ruled out. Markets, however, are forward-looking, and modest delays or operational complications would likely be absorbed. Political and geopolitical risks remain abundant as well, yet the probability of the darkest scenarios still appears relatively low.

On the other hand, several developments could further reinforce the rotation now underway. For example, additional vaccine developers are expected to report clinical trial results in the coming weeks. Moderna, according to expectations, could release data later this month. If Moderna’s results, or those of other candidates, prove similarly encouraging to Pfizer’s, the pro-cyclical rotation would receive another strong tailwind. Simply put, multiple effective vaccines increase the odds of a faster end to the pandemic.

This emerging pro-cyclical rotation therefore has a materially higher chance of persisting and playing out more fully. If it does, it is likely to become the dominant market force shaping price action across a broad range of assets over the coming weeks and months. For investors who identify it early, it may offer attractive opportunities for tactical positioning.