Turkey’s president Erdogan has once again replaced the central bank governor. Turkish markets weakened sharply.

Turkey’s President Erdogan has once again replaced the governor of the central bank, for the fourth time in five years. However, the latest change, which took place at the end of last week, is considered particularly controversial, and markets reacted very negatively. Turkish stocks and bonds plunged sharply. The Turkish lira also weakened significantly.

The outgoing governor, Naci Ağbal, was removed from his post only two days after the latest central bank meeting, at which he unexpectedly announced an increase in the key interest rate by as much as 2%, and at the same time promised that the bank would maintain a strict monetary policy until there is a lasting decline in inflation and the restoration of price stability.

Investors and economists clearly welcomed these steps. In recent months, the Turkish economy has again been struggling with rapidly rising inflation, and the domestic central bank suffers from a lack of credibility, which deepens foreign investors’ distrust and prevents larger capital inflows into the country. A decisive rate hike and a clear commitment by the central bank to ensure price stability were therefore exactly what markets needed to hear. The lira strengthened immediately after the bank’s meeting.

However, President Erdogan was angered by the central bank’s latest decision under Governor Ağbal, and it was undoubtedly the reason for his swift dismissal. The Turkish president is known as a fervent opponent of raising interest rates. He calls interest rates “the mother and father of all evil” and promotes idiosyncratic economic theories, euphemistically described as “unorthodox,” according to which one should not fight rising inflation by raising rates, as most economists argue, but rather by lowering them.

The problem, however, is that Erdogan’s theories of inflation and interest rates are not applicable to an economy like Turkey’s today, and in practice they cause it serious problems.

The hard lot of TCMB governors

The president’s belief that high interest rates are the cause of high inflation (and not a tool to reduce it) was likely shaped by his experience in the food industry, where he worked in managerial positions before beginning his political career. Turkish firms at the time were mostly highly indebted, and interest costs made up a significant percentage of their total costs. An increase in interest rates therefore meant a significant rise in total costs for them, which they could, to some extent, pass on to consumers by raising food prices.

This theory therefore assumes high indebtedness among most firms, a weak competitive environment that allows firms to shift higher costs onto consumers, and it completely ignores the effect of interest rates on inflation through the exchange rate. Turkey’s economy today, however, depends on inflows of foreign capital, so lowering rates reduces the attractiveness of Turkish assets, leads to capital outflows, a weakening of the lira, and consequently to more expensive imports and rising prices (inflation).

The governors of the Turkish central bank (TCMB) thus find themselves caught between two millstones. If they raise rates, or do not cut them enough, they anger Erdogan. But if they cut rates, they must face rising inflation and a weakening currency, which will not earn them praise either. It should be added that Erdogan is willing to quietly tolerate some rate increases, but only in a critical situation, when it is absolutely necessary to stop the lira from weakening.

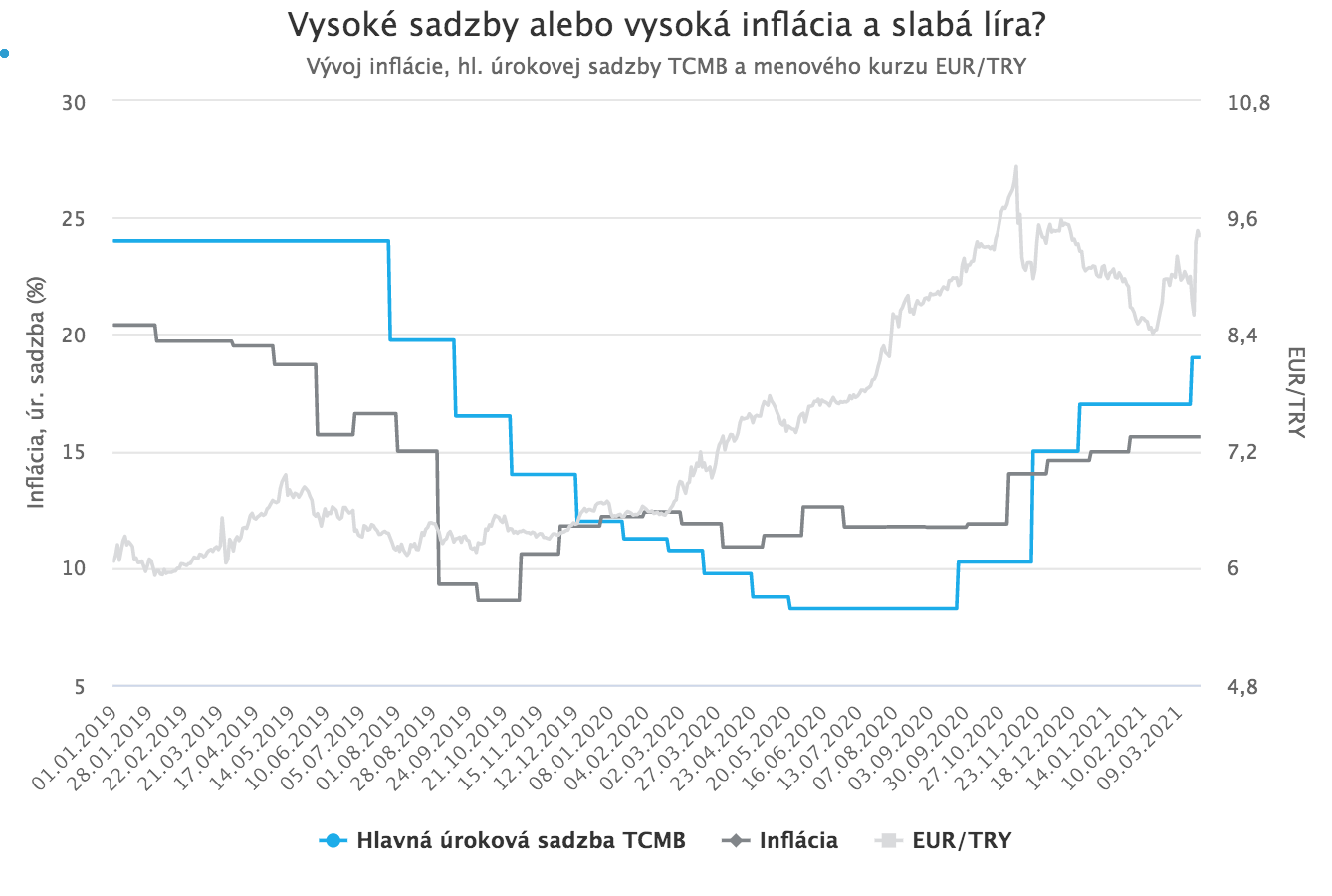

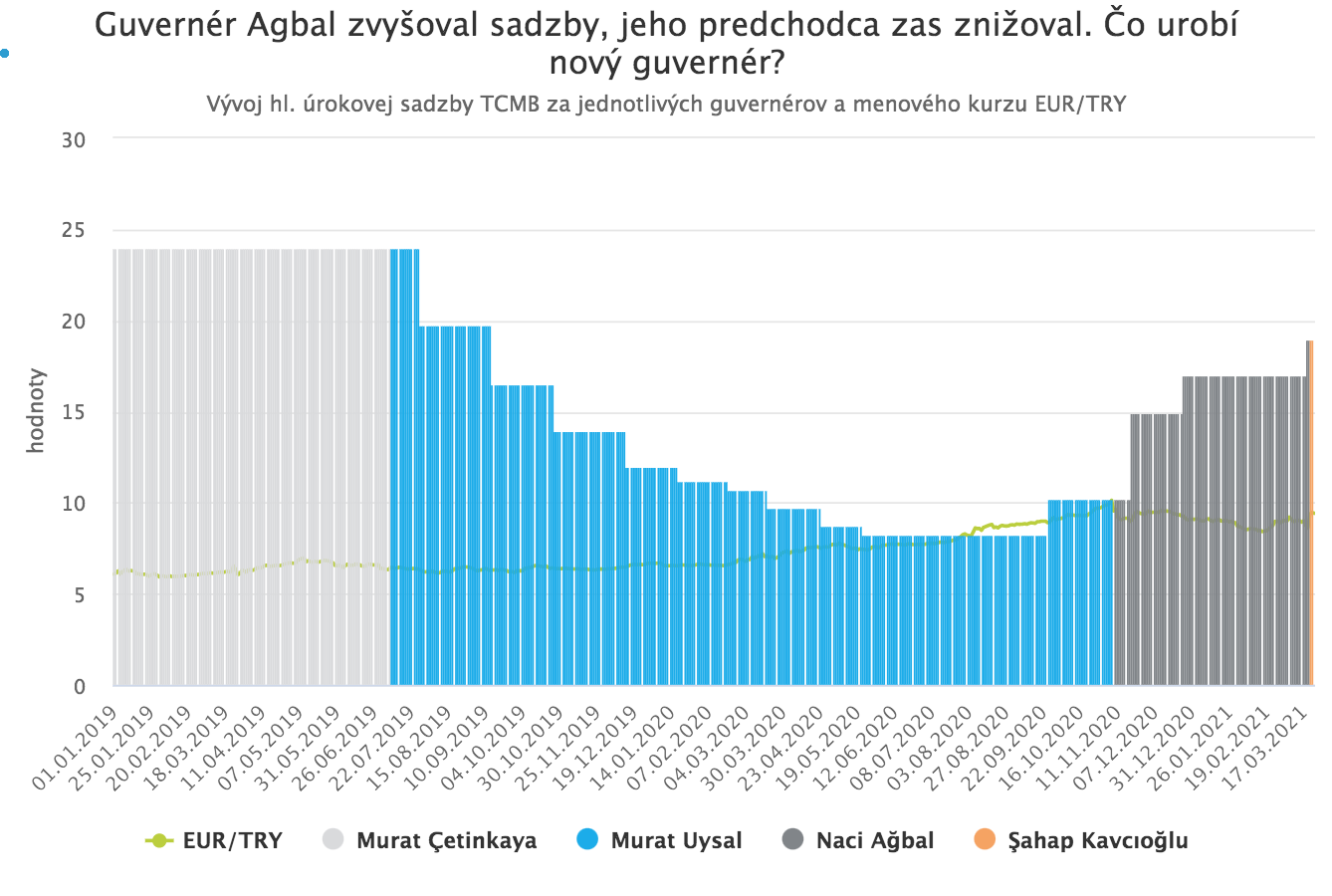

Governor Murat Çetinkaya helped avert a currency crisis by decisively raising rates to 24%. In the end, however, it cost him his job because he did not begin cutting rates quickly enough at the first signs of stabilization. His successor, Murat Uysal, took that lesson to heart and, over 14 months in office, cut rates by a record 15.75%. This, however, led to a marked weakening of the lira and a renewed rise in inflation, which ultimately cost him his job anyway.

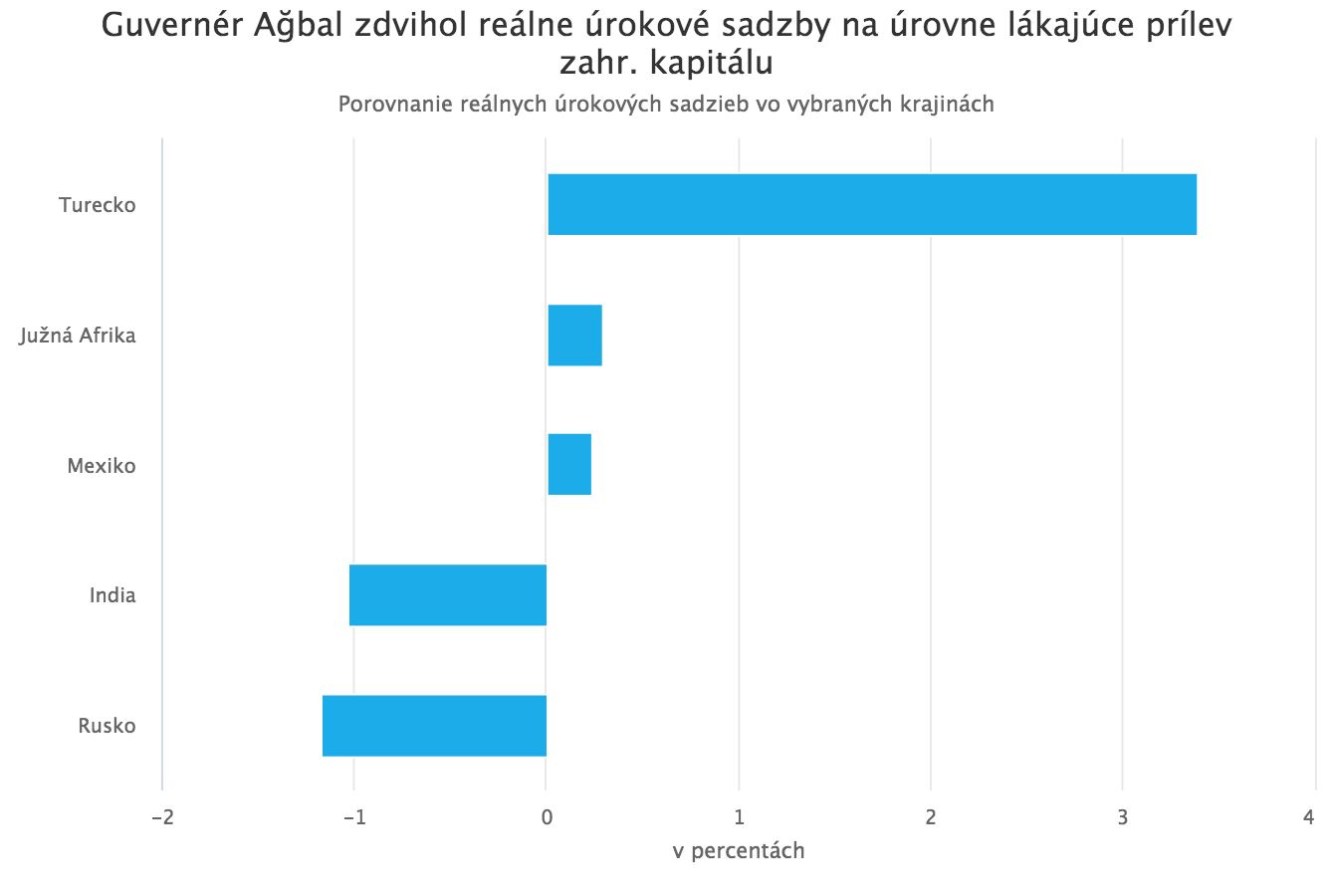

The main task of his successor, Ağbal, was therefore to avert an emerging crisis and stabilize the rapidly weakening lira. He succeeded, mainly thanks to decisive rate hikes. Under his leadership, the TCMB raised the key policy rate by as much as 8.75 percentage points in four months, to 19%. The real interest rate in the country thus moved from negative territory to the highest level among emerging markets.

However, the last unexpectedly large rate hike (markets expected only a 1% increase) and the central bank’s commitment to keep rates high until inflation falls evidently crossed the limits of Erdogan’s tolerance. Governor Ağbal therefore also had to go.

What to expect from the new governor?

Ağbal’s swift dismissal was an unpleasant surprise for markets. An even greater shock, however, was the name of his successor. He is Şahap Kavcıoğlu, a banker and politician. Kavcıoğlu is politically close to the president and served in parliament as an MP for Erdogan’s AKP party. It is likely, however, that the decisive characteristic that brought him to the position of central bank governor is that he shares Erdogan’s views on interest rates.

In fact, the very day after the rate hike under Ağbal’s leadership (and thus the day before his own appointment), Kavcıoğlu wrote a column in the pro-government newspaper Yeni Safak, in which he attacked Governor Ağbal and accused him of acting against the Turkish economy by raising rates. According to Kavcıoğlu, the central bank “should not insist on a policy of high interest rates. While interest rates around the world are close to zero, raising rates will not solve the economic problems in our country. On the contrary, raising rates will only deepen problems in the future, because it will indirectly lead to an increase in inflation.”

It therefore seems that the new governor’s views perfectly mirror Erdogan’s, both in content and in the way they are presented. Kavcıoğlu apparently believes, contrary to economic theory and practice, that rising inflation should be fought by cutting rates. He considers previous rate hikes to be domestic conspiracies, and the conditions that forced them (a weakening lira, capital outflows, the deficit) to be a foreign conspiracy against the Turkish economy.

Markets did not welcome the change

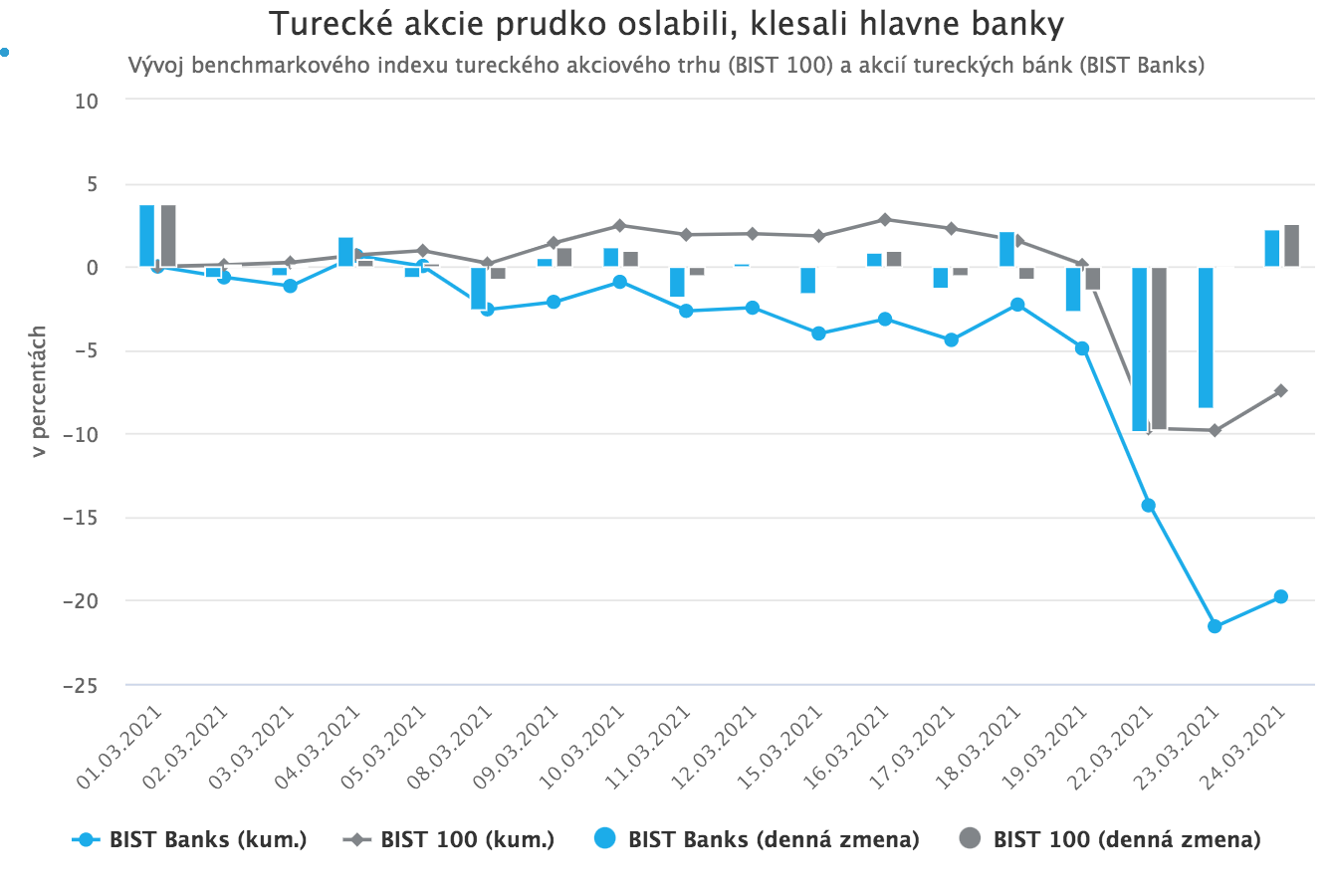

Such rhetoric, although undoubtedly pleasing to Erdogan, represents exactly the opposite of what investors and economists would want to hear from the head of an institution that has a long-standing credibility problem, should be politically independent, and must now face an acute threat of rising inflation. It is therefore not surprising that as soon as markets opened on Monday after the weekend replacement, Turkish stocks and bonds headed steeply lower.

Turkey’s main stock index lost almost 10% during Monday. The biggest declines were suffered by Turkish banks. Their shares did not stop falling sharply the next day either. Over two days, they lost more than 17%.

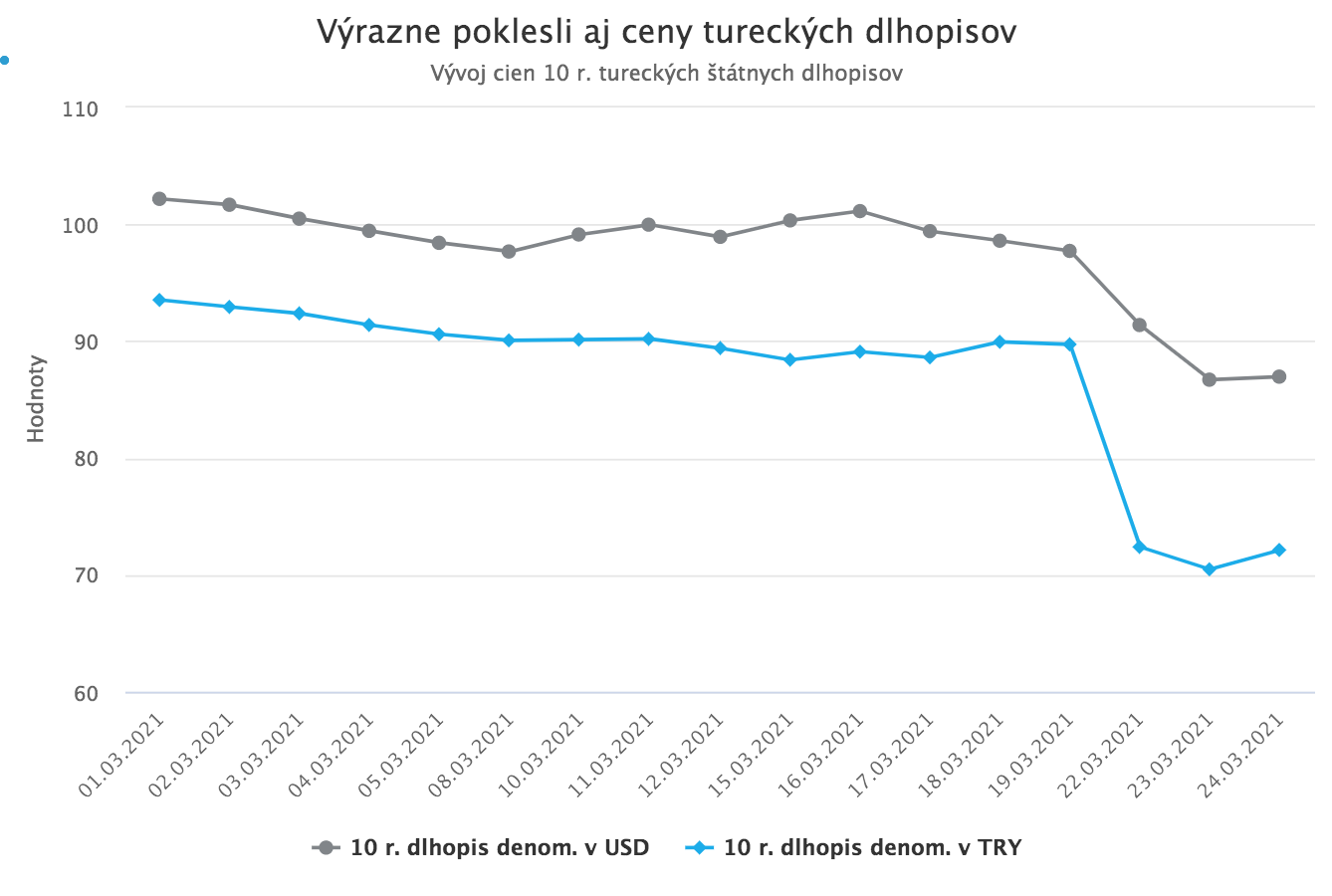

A significant drop was also recorded in Turkish bond prices, especially those denominated in the domestic currency. Their yields shot up to as high as 18%. Government bonds denominated in foreign currencies fell somewhat more moderately.

The Turkish lira, which has long been one of the most fragile currencies among emerging-market currencies, naturally also suffered a sharp weakening. In the course of a single day, it erased almost all of Governor Ağbal’s several-month effort to stabilize it.

The outlook is not optimistic

The market reaction to the governor’s replacement was very sharp; however, in the current context it does not appear exaggerated. If the new governor truly follows the views that brought him to this position when steering central bank policy, further weakening of the lira and of Turkish stocks and bonds can be expected.

Moreover, over the course of last year the Turkish central bank used up a large part of its foreign exchange reserves and therefore has limited room to stabilize the lira through market interventions. It is therefore likely that if pressure on the lira continues, it will resort to various restrictions limiting trading in the lira on foreign markets and making access to foreign currencies more difficult on the domestic market.

President Erdogan described the current developments in markets as temporary fluctuations that do not reflect the fundamentals, dynamism, and potential of the Turkish economy, and he called on foreign investors to “believe in the strength, potential, and future of Turkey.” The seriousness of the situation is underlined by the fact that he simultaneously urged citizens to “invest their foreign exchange reserves and gold in domestic financial instruments that support our economy and production.”