Domestic currencies of the V4 countries are under pressure

From an exchange-rate perspective, it is positive that the central banks of these countries have started fighting inflation in recent months and have significantly raised their key interest rates. This led to a strengthening of domestic currencies in recent weeks. Therefore, the current weakening of these currency pairs has not reached critical levels; on the contrary, they have returned to the values seen before central banks intervened in monetary policy. On the other hand, raising interest rates was meant to curb inflation. However, a decline in the exchange rate has a pro-inflationary effect, and the price level will continue to rise. Inflation in these countries will probably exceed 10%, as imports will become significantly more expensive. This factor will be further reinforced by commodity prices, which are rising sharply again due to the war and are reaching multi-year highs.

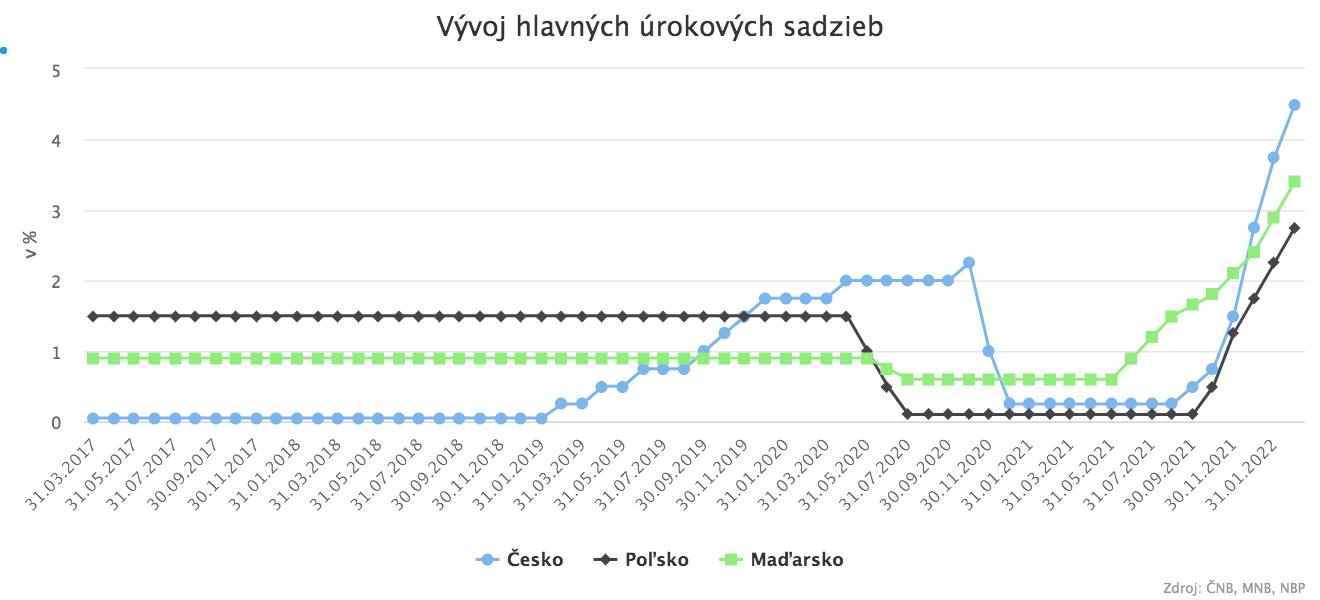

How much room is there for further rate hikes?

Almost none, because further increases in interest rates would cause a recession in these countries. The reason is simple: more expensive borrowing reduces demand for loans, thereby restraining economic growth. Of course, these countries will have little choice, and if necessary they will proceed with further rate hikes, because otherwise they could risk an inflationary spiral. It should be noted that even this tool is not all-powerful, and if escalation intensifies, it will not be sufficient. In the Czech Republic, the key interest rate is currently at 4.5%, the highest level since January 2002. Hungary raised its interest rate in February to 3.4%, reaching the highest level since October 2013. Poland has also declared war on inflation, and its key interest rate stands at 2.75%. Poland had a similar level in 2013.

The Czech Republic has extremely large foreign-exchange reserves for its size

As mentioned above, the Czech Republic has the highest key interest rate among these countries, so the room to raise it further is quite limited. The positive news is that the Czech National Bank does not rely only on the key interest rate, but also holds enormous foreign-exchange reserves. Specifically, it holds approximately USD 175 billion, EUR 157 billion, and more than CZK 3.8 trillion. To put this into perspective, the size of these reserves exceeds the Czech Republic’s GDP, which was USD 245 billion. These massive reserves can be used by the central bank in case of need to intervene in the foreign-exchange market. We can see this in real time. The CNB announced today that it has started intervening in the FX market to stabilize the weakening of the Czech koruna. This step could stabilize further declines in the koruna, but even this tool is not sufficient if real panic were to occur. Poland’s central bank has also announced interventions in the market, and in Hungary we can expect a similar approach. If the conflict escalates and Czech citizens and foreign investors lose faith in the currency, an uncontrolled collapse like the ruble’s could occur. Even in that case, it is possible to ask the IMF for help so that the central bank can stabilize the exchange rate. The exchange rate of the Czech koruna is determined exclusively by supply and demand. So logically, people trying to protect their savings would move into safe havens, worsening the situation because they would contribute even more to the strengthening of the euro or the U.S. dollar. The only advantage of a weakening currency is increased demand for products from the country, since a weaker currency makes exports cheaper. However, no one is saying that such a worst-case scenario will actually happen and the currency will collapse. Some analysts assume that in an unfavorable scenario, the EUR/CZK exchange rate could reach as much as 28 koruna per euro. For now, there is no reason for extreme panic, because the currency is still under control and unnecessarily increasing fear makes no sense. In addition, investments held by Czech citizens in U.S. dollars or euros benefit from this situation as long as they are not currency-hedged.