Biden Plans to Raise Taxes on Investment Gains. Could a Sell-Off Hit U.S. Stocks?

During yesterday’s ceremonial address in Congress, President Biden officially introduced an ambitious USD 1.8 trillion plan to support American families and education called the “American Families Plan.” This is already the third major support and reform program the President has presented during his first 100 days in office. It follows the economic rescue package worth USD 1.9 trillion and a USD 2.3 trillion plan to rebuild U.S. infrastructure, which is still awaiting approval. The new plan includes measures to improve access to education and make childcare easier. For example, it proposes paid parental leave, child tax credits, tax relief for low-income groups, a teacher training program, and free preschool facilities. These measures are to be financed in part by higher taxes for the highest-income groups. Naturally, this part of the plan is now in the spotlight for investors, and analysts are trying to estimate its impact on stock markets.

Higher income tax and higher capital gains tax

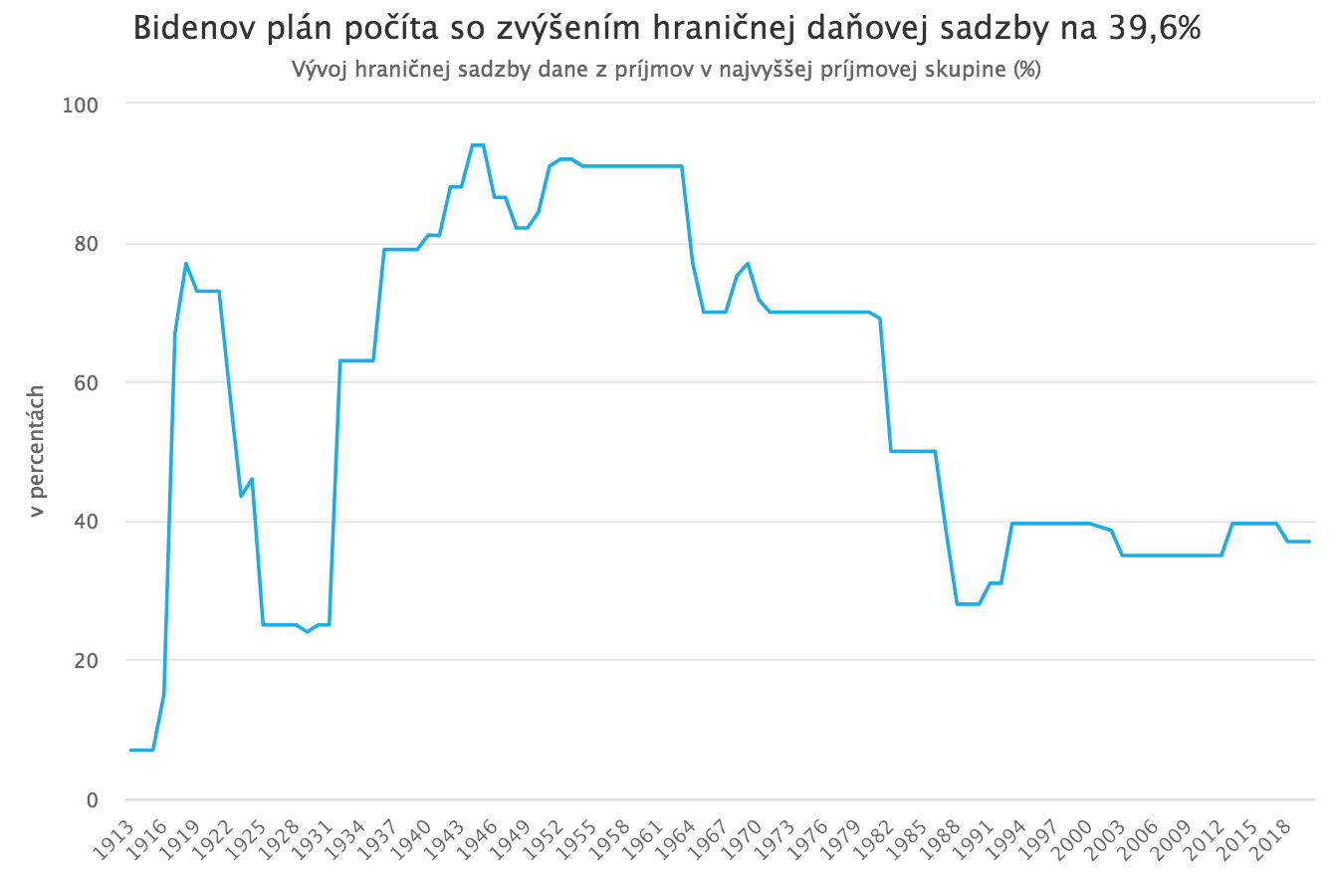

The planned tax increases include raising the top marginal income tax rate for the highest-income bracket and increasing the capital gains tax, also only for the highest-income bracket. The plan also includes improving tax enforcement and measures to prevent certain forms of tax optimization. The marginal income tax rate for households in the highest-income bracket, meaning those with income exceeding USD 400,000 per year, would rise from today’s 37% to 39.6%. This is essentially a return to the pre-2017 level, before Trump’s tax reform lowered the rate from 39.6% to the current 37%. So this is not a dramatic increase, and historically it remains a relatively low level. Looking at the history of this rate shows that a higher top marginal tax rate is not an obstacle to economic growth. When the U.S. economy experienced its “golden years” of strong growth after World War II, this rate was as high as 91%. Raising the top marginal income tax rate is therefore not a true concern for markets, even though nobody in that bracket is, of course, pleased by it. Potentially larger and more immediate market effects could come from the proposed increase in the capital gains tax. In the United States, the capital gains tax is currently 20%, or 23.8% if we include the special Obamacare surtax. Capital gains are therefore taxed at a lower rate than other income. President Biden considers this unfair. In the words of A. Dunn from the President’s team: “The President is aware that something is wrong with our tax system when the income of a hedge fund manager earning hundreds of millions of dollars is taxed at a lower rate than the salary of the maintenance worker in his office or the cleaner in his villa. (The President) will therefore take steps, steps supported by the American public, to restore fairness to our tax system.” Biden proposes doubling the capital gains tax for people earning more than USD 1 million per year, bringing it up to the same level as the planned top marginal income tax rate for that income group, namely 39.6%. Capital gains of the wealthiest Americans would then be taxed at the same rate as their other income.

The threat of higher taxes has not frightened markets so far

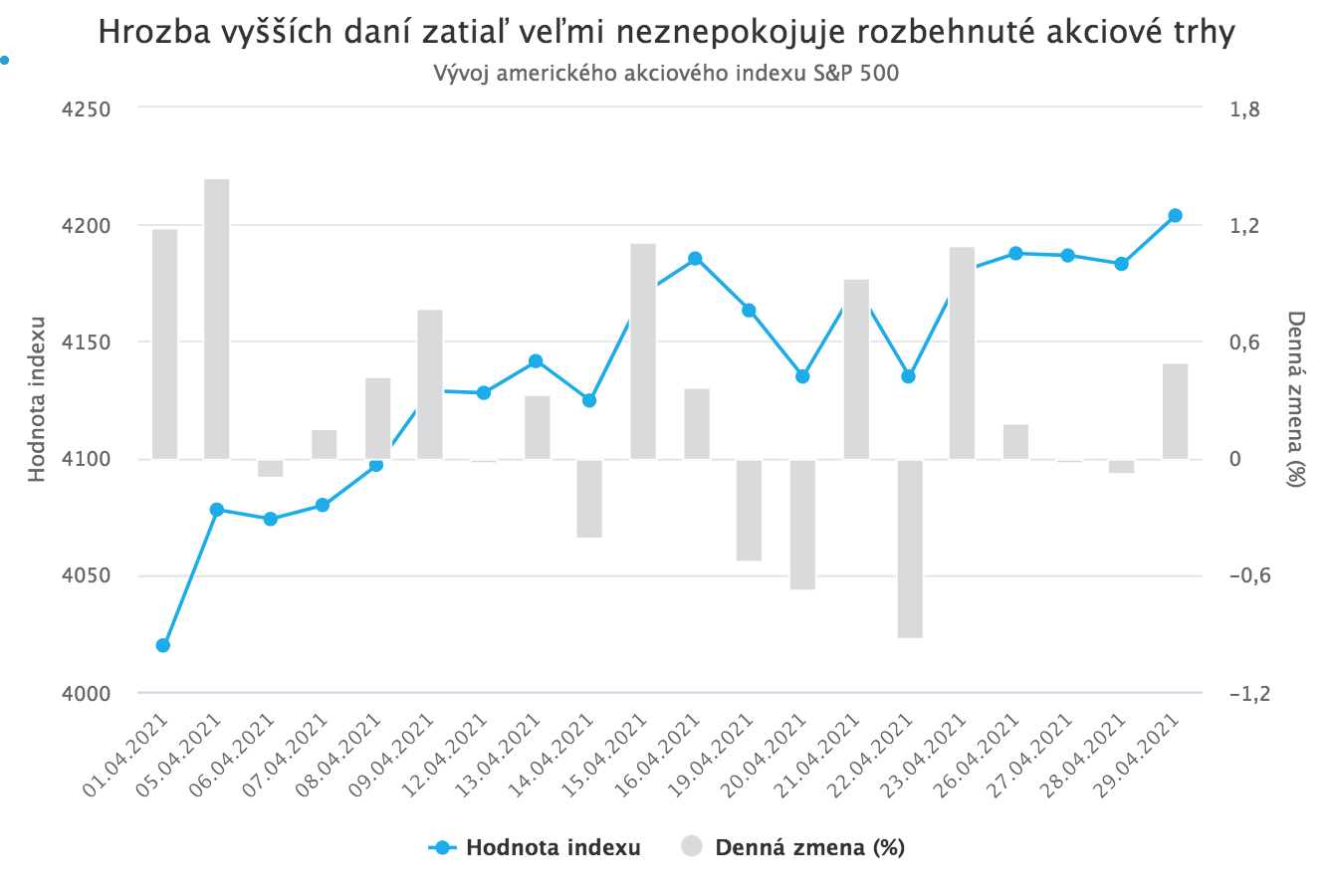

The proposed increase in the capital gains tax could, in theory, have a material impact not only on the investors directly affected due to the size of their incomes, but also on stock markets as a whole. Investors who would be subject to the higher tax could decide to close some profitable positions before it takes effect, so their gains would still be taxed at the current lower rate. If such selling ahead of the tax hike reached sufficient volume, it could pull the whole market down and cause losses for other investors as well. But should we be worried about such a scenario? So far, investors clearly do not seem very worried. Information about the planned capital gains tax increase first became public last Thursday (22 April). U.S. stock indices reacted with an almost 1% decline. Given the low volatility in recent weeks, it was the largest drop of the entire month. Interestingly, the decline did not happen immediately when the information appeared in a New York Times article, but only a few hours later when it flashed on Bloomberg terminals. It therefore seems it “scared” automated trading strategies more than individual investors. The very next day, however, markets calmed down, continued to rise to new highs, and even the official presentation of Biden’s plan did not change that. Strong first-quarter results from the largest U.S. companies, solid macroeconomic data, and a “cooperative” Fed gave investors plenty of reasons for optimism. In addition, it is not yet clear whether Biden will succeed in pushing these tax increases through. Democrats currently hold only the narrowest majority in Congress, and some of them reportedly are not willing to support the proposal. But what if Biden ultimately does succeed in raising the capital gains tax to the level currently proposed? Would stock markets fall? Analysts have been considering this question for months, and the first forecasts were published even before Biden was elected. After all, tax increases under a Biden presidency were widely expected, and the capital gains tax has been seen from the start as the most likely candidate for an increase.

Will a sell-off occur if Biden pushes his plan through?

Forecasts of the impact of such a tax increase on stock markets are based mainly on how investors reacted to the last significant capital gains tax increase in 2013 and on the current volume of unrealized gains held by investors who would theoretically be subject to the tax. Under the currently proposed conditions, the capital gains tax increase would affect about 0.32% of U.S. taxpayers. Only that share of taxpayers had income exceeding USD 1 million in the previous year and also reported capital gains or losses. Percentage-wise, this is not a large number, but it is important to remember that stock ownership is highly concentrated among the highest-income groups. According to Federal Reserve data, the top 1% of the wealthiest Americans currently own 53% of all stocks. The top 10% own almost 90% of stocks. Lower-income groups hold almost no stocks.

Given this high concentration of stock ownership among the highest-income groups, even the reaction of 0.32% of the wealthiest Americans could, in theory, have a significant impact on the overall market. However, if their reaction is not very different from past capital gains tax increases, markets are not facing any massive sell-off. Analysts at the investment bank Goldman Sachs estimate that unrealized stock market capital gains of the wealthiest Americans currently amount to USD 1 to 1.5 trillion. That is roughly 3% of the total market capitalization of U.S. equity markets and 30% of the average monthly trading volume of the S&P 500. It is not likely, however, that investors would decide to realize this entire amount before the tax increase. In 2013, ahead of the capital gains tax increase from 15% to 25%, the wealthiest investors sold only 1% of their equity portfolios, and in the very next quarter they bought 4% more. If the affected income groups sold 1% of their portfolios today, the selling volume would, according to the bank’s estimates, reach USD 120 billion. JPMorgan estimates slightly higher selling of around USD 200 billion. If sales of USD 120 to 200 billion were concentrated in one quarter right before the tax increase takes effect, they would by themselves have a noticeable impact on the main stock indices and pull them down by several percent. However, these volumes are not large enough to push equity markets lower regardless of other factors. If market conditions are otherwise positive, normal buying flows can offset them. So if Biden’s proposed capital gains tax increase were approved in its current form, increased selling flows would likely appear in the quarter before it takes effect. If market sentiment is positive at that time, stock markets may rise less than they otherwise would have without the higher tax, but no dramatic declines would occur. If, however, sentiment is negative at that time, then the selling triggered by the tax increase would amplify the market’s declines.