Can Tech Stocks Rise Forever?

The benchmark S&P 500 index reached a new high this week. The rally, however, has been far from broad-based. The index has been pulled up from the depths of the pandemic largely by the outsized gains of a handful of the largest technology companies. Firms such as Amazon, Apple and Facebook did fall during the peak of market panic in March, but they quickly erased those losses, and their advance in the weeks and months that followed only accelerated.

In fact, many of the major social, economic and investment trends that have been propelling these companies for years have been reinforced and sped up by the pandemic. As a result, today’s tech giants enjoy near-ideal conditions to continue growing, in effect, indefinitely in a post-pandemic world.

A key engine behind their rise is a self-reinforcing mechanism created by the rapid growth of passive, index-based investing. The most important equity indices, including the S&P 500, are market-cap weighted. In practice, this means that the largest weight is assigned to the companies with the highest market capitalization, and market capitalization is driven by share price. The higher the price, the higher the market cap, and therefore the larger the index weight.

At the same time, the larger a company’s weight in major indices, the stronger the mechanical demand for its shares. Hundreds of ETFs and index funds designed to track the most popular indices must buy constituent stocks in proportion to their index weights. In other words, the larger a company’s weight in an index tracked by ETFs, the more money flows into its shares. And the stronger the demand, the higher the share price, which in turn pushes market capitalization higher and further increases the stock’s weight in the index. The loop then reinforces itself

The popularity of passive investing has been rising sharply in recent years. In August of last year, assets in passively managed U.S. index funds and ETFs surpassed those in actively managed funds, and the trend has continued. As ever larger sums flow into index funds and ETFs, they disproportionately flow into stocks with the largest index weights. That steady demand keeps pushing the prices of those stocks higher, further increasing their weights. The primary beneficiaries of this “index perpetual motion machine” are precisely the handful of mega-cap technology firms that dominate major indices.

Kings of the indices

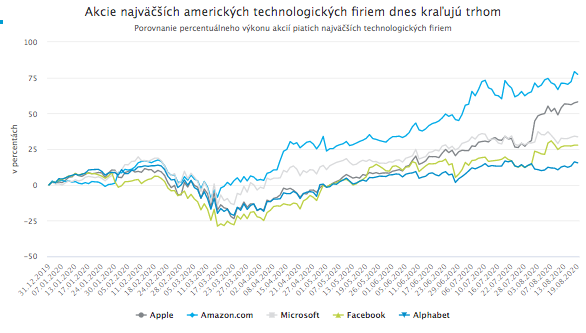

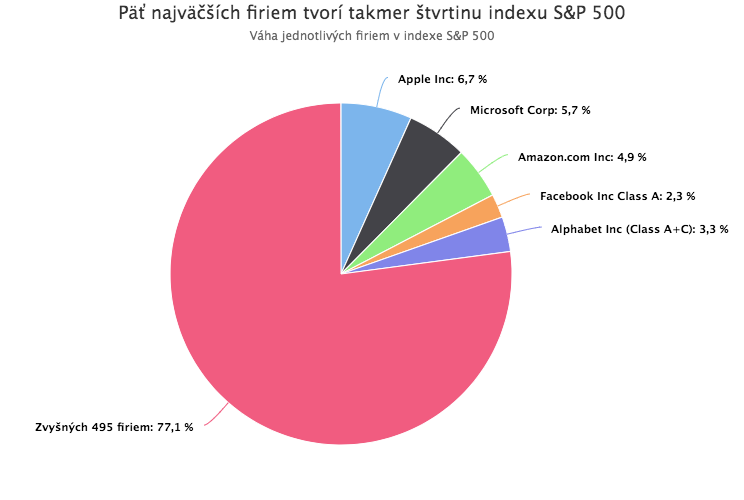

The most widely followed benchmark today is the S&P 500. By a wide margin, the five largest constituents are technology giants, Facebook, Amazon, Apple, Microsoft and Google (Alphabet), collectively known as FAAMG. Their prices and market capitalizations rise within the same mutually reinforcing mechanism.

Five years ago, the top five constituents accounted for roughly 12% of the S&P 500. Today, thanks to their surging market capitalizations, their combined weight exceeds 23%, higher than at the peak of the dot-com bubble. In other words, nearly a quarter of the index widely viewed as the benchmark for the entire U.S. equity market is now made up of just five technology companies.

Because of their outsized gains and heavy index weights, these stocks lift the entire index and create the impression of a strong U.S. equity market. In reality, the headline performance is often driven largely by a small number of mega-cap tech names.

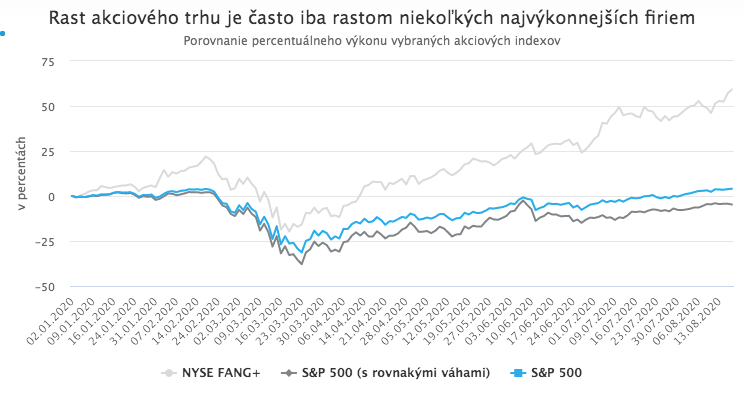

This is illustrated by a simple comparison. The S&P 500 has gained 4.05% year-to-date. But if each of the 500 constituents were assigned an equal weight, thereby removing the outsized impact of the five largest companies, the equal-weight version of the index would be down nearly 5% year-to-date. That is roughly 9 percentage points below the conventional market-cap-weighted benchmark.

If we isolate only the ten largest technology stocks, the contrast becomes even clearer. The ten companies that make up the NYSE FANG+ index are up an average of 59.25% year-to-date. Mega-cap tech stocks do not dominate only the S&P 500. Their appeal and specific characteristics mean they appear across hundreds of indices, thematic and factor funds, as well as popular “smart beta” products. That makes them the largest beneficiaries of the index “perpetual motion” effect, a mechanism that helps explain their extraordinary performance.

Importantly, there is little evidence that this mechanism will stop anytime soon. The sharp sell-off in March and the subsequent rapid rebound, which many actively managed funds missed as they failed to re-enter markets in time to benefit from the central-bank liquidity wave, has only strengthened the appeal of passive investing.

The pandemic strengthened their hand

The pandemic and the resulting changes in social and economic behavior have also handed technology giants additional advantages. Fear of physical contact and restrictions on mobility have naturally accelerated the adoption of contactless, technology-based solutions by both consumers and companies. This trend, which benefits the same firms that dominate major indices, has become visible across virtually every area of daily life.

It is also reasonable to assume that even if the pandemic ultimately fades, new consumer habits and investments into contactless technologies will not simply disappear. The crisis has also produced changes in the macro environment that, coincidentally, support the same group of companies. Aggressive rate cuts and the compression of bond yields by central banks have pushed investors to look for alternatives to safe, but unattractive bonds offering negative real returns. They often find that alternative in the equities of large technology firms.

After all, where can one invest more “safely” while still seeking returns than in a small group of the world’s largest companies, many of which enjoy quasi-monopolistic positions, are well aligned with current technological and social shifts, operate business models that generate recurring cash flows, and maintain strong balance sheets with billions in excess cash?

Record-low interest rates, likely to remain near current levels for years, also allow these companies to keep employing a strategy that has proven effective in recent years: despite holding vast cash reserves, they can issue debt at very low (and in some cases even negative) yields, then use the proceeds to repurchase their own shares. By reducing the number of shares outstanding, earnings per share rises even if total profit does not. Equity prices respond accordingly.

Unstoppable?

Tech giants therefore face highly favorable conditions to continue rising. But it is unlikely to last forever.

The most significant and, in the short term, most probable obstacle is antitrust action. Calls to break up these data monopolies are becoming increasingly common, including among policymakers. Reports of soaring share prices (and founder wealth) amid a deep economic contraction are likely to amplify those voices.

Even if regulators do not end the rally, the trends that currently fuel it, including the powerful index-driven feedback loop, will eventually lose momentum. The more money that flows into passively managed index products, and therefore into the stocks with the largest weights, the harder it becomes to lift those stocks by another few percentage points, both mechanically and in valuation terms.

At the same time, it may become easier for active managers to outperform by investing in high-quality smaller companies that do not enjoy large index weights and therefore trade at much more attractive valuations. If, at a broader scale, active strategies begin to outperform passive index products, fund flows would likely reverse, and the “perpetual motion machine” would ultimately slow and stop.