2021 Has Ended, What Can We Expect from 2022?

Equities performed well in Western markets

When we talk about strong gains, the S&P 500 exceeded 26%, the Nasdaq gained more than 21%, and the Euro Stoxx 50 rose by more than 20%. By contrast, Asian equities performed less well, showing limited growth overall, and Chinese equities quite literally bled. Japan’s Nikkei 225 added a little over 4% last year, while China’s CSI 300, on the other hand, lost a little over 5%. This decline in Chinese equities has very clear reasons, mainly the government’s aggressive policy aimed at weakening powerful players in the economy and thereby limiting their growing influence in the country. In addition, there is also the poor situation in China’s construction sector, where several construction companies have accumulated unsustainable debt and will likely be forced to cease operations.

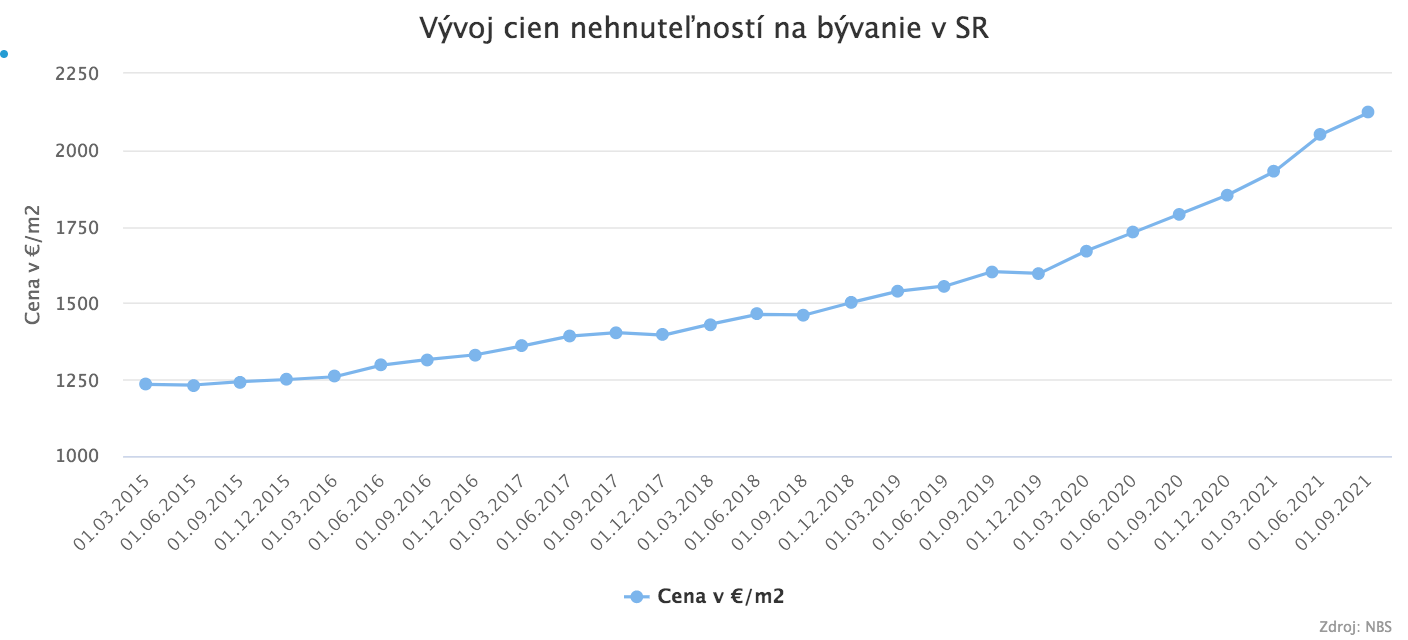

Real estate did not lag behind equity markets

Many analysts were concerned about how property prices would react after the onset of the pandemic. However, contrary to all skeptics, they managed not only to hold their value but even rose significantly. The latest published Slovak data indicate an 18.4% year-on-year increase in residential property prices. Such robust growth easily covers inflation and provides an attractive return for the investor or owner. Some analysts, however, raise a warning flag and believe real estate is heading into a bubble, but the real estate market was heavily impacted after the financial crisis, and therefore the current growth following a period of post-crisis stagnation, when property prices stagnated for a longer time, is not unhealthy or shocking. The pronounced growth has been driven mainly by high demand for property and low supply in our real estate market. In addition, the current rise in the prices of input materials for construction has also contributed to higher property prices. Similar developments in real estate price growth can be observed in our near surroundings as well as elsewhere in the world. Therefore, it still holds that real estate can currently offer investors a safer investment than equities, while still providing attractive appreciation.

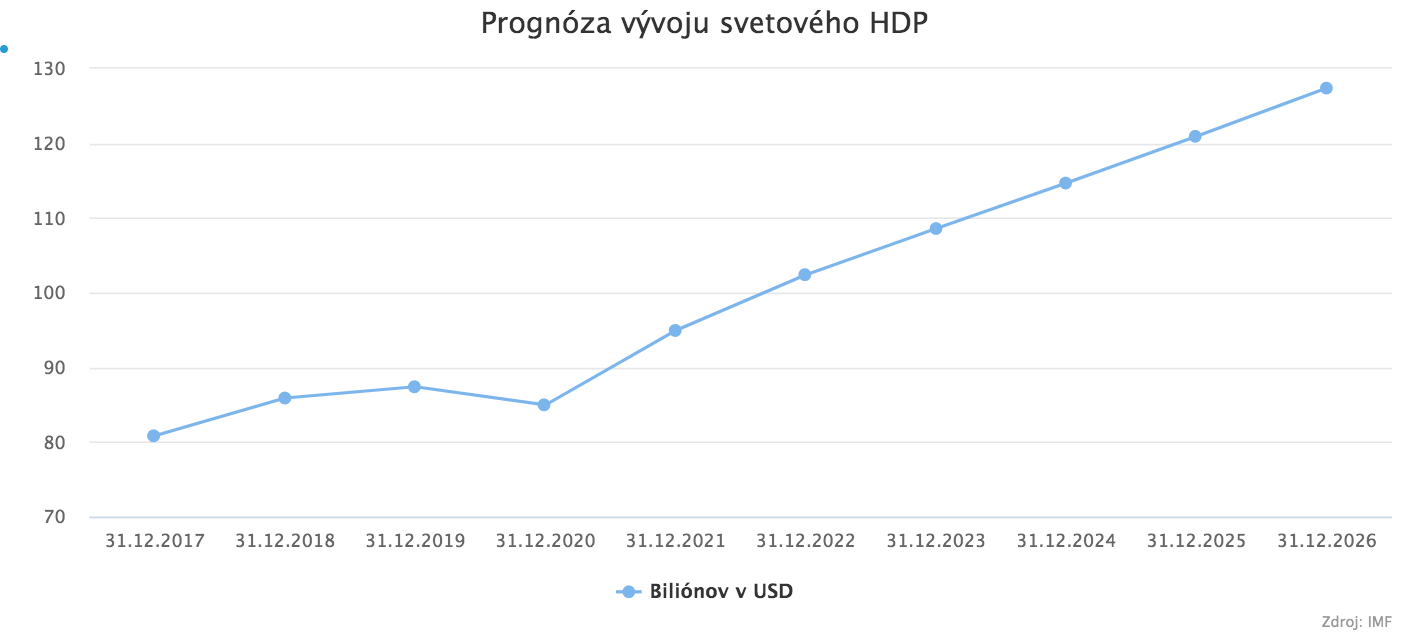

The global economy is recovering quickly; Slovakia more slowly

Of course, many advanced countries also performed well, and as measures were gradually relaxed there was a significant recovery in economies. As a result, global GDP could probably return to, and surpass, its pre-pandemic level already this year, supported by expected strong growth in 2021 of 5.6% according to the World Bank, or as much as 6% according to the IMF. This would represent the strongest global economic growth after a recession in the last 80 years. However, we still have to wait for the final data for Q4 2021. The World Bank also provides an outlook for the current year and expects global economic growth of 4.3%, and growth of 3.1% in 2023. It is natural that after economic expansion come years of consolidation. In addition, the world has still not dealt with several factors that continue to threaten economic stability and growth. The Slovak economy grew in the third quarter at a rate of only 1.3%; the slower growth was driven mainly by weak foreign demand for our products. By contrast, domestic consumption performed well and supported economic growth, although industry remains the most dominant contributor.

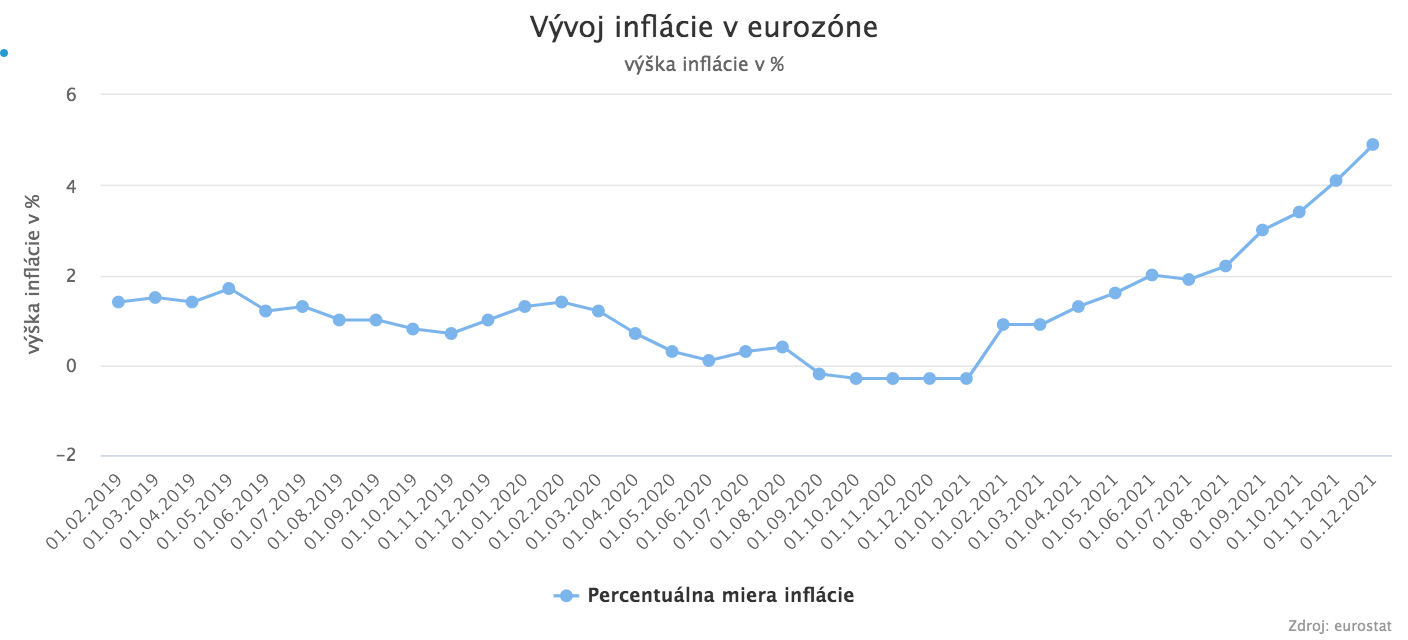

Economic problems persist

The most pronounced problem is rising inflation, which likely will not be transitory as most economists believed. It is keeping central bankers awake at night, and around the world they have begun to raise interest rates modestly in order to reduce the availability of cheap capital and slow inflation, with the exception of the Fed and the ECB. These central banks are taking their time and so far are making changes only in the area of asset purchases, which they are gradually reducing or plan to do in the near term. The Fed is acting much faster than the ECB, as it plans to begin raising interest rates this year, and to do so several times. By contrast, the ECB does not plan to adjust interest rates this year and intends to keep them at low levels. A sharp increase in interest rates would significantly threaten low-income groups, whose loans would become much more expensive. Such a step would also significantly slow business activity, since financing would also become more costly, which would result in weaker economic growth. Even a potential increase in interest rates might not curb inflation, since this inflation is not caused only by cheap cash, but mainly by the pandemic and a sharp rise in commodity prices, especially energy. In addition to inflation, the pandemic is still with us and is nowhere near over. At the end of 2021, a new virus variant emerged that proved highly infectious, although probably less dangerous. We are therefore currently witnessing new records in the number of positive cases, and many experts fear another pressure wave on hospitals that could lead to renewed shutdowns of economies, further damaging supply chains. This fact continually complicates many companies’ ability to keep production running. A significant and persistent problem is also the chip shortage, which remains unresolved and we will likely feel it throughout the year.

Challenges for 2022

Among the biggest challenges and threats for 2022 is inflation, which could not be brought under control last year and remains far from the 2% target set by both the ECB and the Fed. The US is in a different position from the euro area, since its economy recovered faster and better. The euro area economy still does not show strong growth, and potential adjustments to interest rates could reduce this growth further, which is what the ECB fears most. In addition, there is still the ongoing energy crisis, which is pushing energy prices to high levels that are feeding through into all parts of the national economy. This problem is crucial for the functioning of advanced countries, and it is necessary to find a solution that reduces pressure on energy prices as quickly as possible. It would probably be appropriate to reconsider the EU’s energy policy and make the targets for the coming years more realistic.

Moreover, the COVID-19 pandemic has not left us; it will likely gain strength in 2022 and we will see new records. The pandemic is again beginning to constrain some large companies that must quarantine a large portion of their employees and subsequently cannot keep their operations running properly. For this reason, several countries are beginning to consider reducing the number of quarantine days for vaccinated individuals. There is also still the unresolved problem of China’s construction sector, which has not yet resolved its issues of extreme indebtedness. Ongoing state interventions in the country also do not help the credibility of its capital markets. Geopolitical tensions in Ukraine are also increasing and investors should not overlook them. Let us hope that an armed conflict never occurs and that this is only a power game.

As for equity markets, they are again at their historical highs, and Apple became the first company in the world to reach a market value of USD 3 trillion. Therefore, investors should remain cautious in capital market investments and monitor how highly equity markets are valued.