Investors Expect Interest Rate Hikes and an Economic Slowdown

Yield curves in several developed economies have flattened significantly in recent days due to a rapid rise in shorter-term yields with minimal changes in longer-term yields. In market jargon, this phenomenon is called “bear flattening”. It is a negative signal reflecting investors’ expectations that central banks will soon raise interest rates, thereby choking off future economic growth.

The yield curve, which shows current bond yields depending on their maturity, is one of the most important economic and market indicators. Changes in its shape, level, and slope provide important information about shifts in market expectations regarding future interest rates, inflation, and economic growth.

These are factors that have a fundamental impact on the expected returns of different asset classes. Professional investors pay close attention to any more significant changes in the yield curve and adjust their investment decisions accordingly.

Bear flattening of the yield curve

Significant yield-curve moves warranting investors’ attention are happening right now, and in several economies at once. Yield curves for British, New Zealand, U.S., and to a lesser extent euro-denominated bonds are changing shape. They are flattening and becoming less steep. That means the spread between yields on longer- and shorter-maturity bonds is narrowing due to rising short-term yields while long-term yields change only minimally.

This type of curve move is called “bear flattening” and is considered a distinctly negative signal from the perspective of both the economy and markets. It reflects investors’ expectations that central banks will raise interest rates and that the economy will slow.

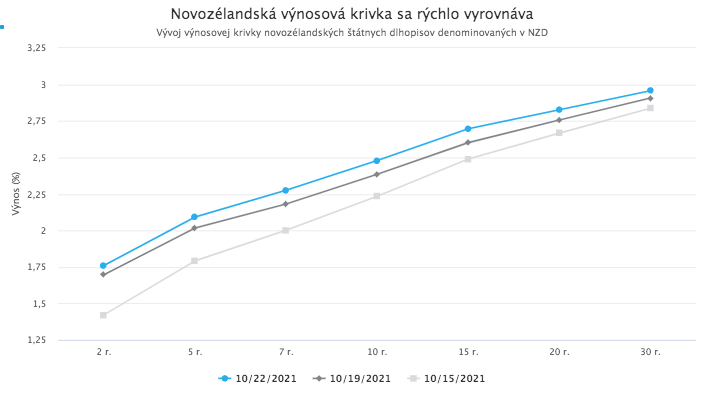

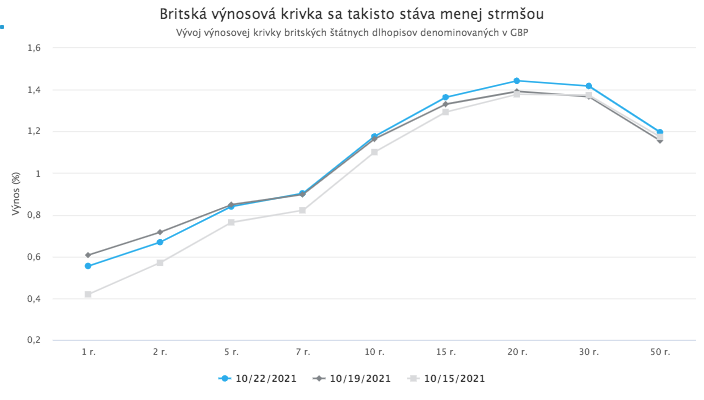

The most pronounced bear flattening occurred at the beginning of this week in the U.K. and New Zealand bond markets.

Yields on 2-year U.K. gilts rose by as much as 17 basis points over two days, while yields on 30-year and longer maturities, by contrast, declined slightly.

Similar moves occurred in the New Zealand bond market. Yields on 2-year New Zealand government bonds rose by as much as 25 basis points over two days, while yields on 30-year bonds saw only minimal movement.

A somewhat less dramatic, but for investors extremely important, flattening is also taking place in the U.S. dollar bond market. The spread between yields on 30-year and 5-year U.S. Treasuries has fallen in recent days below 1%.

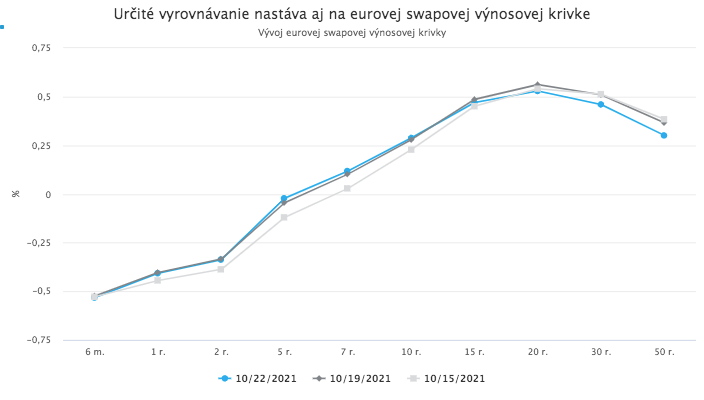

Finally, modest flattening is also occurring in the euro bond market, despite frequent statements by the ECB that it is not planning any rate increases in the foreseeable future.

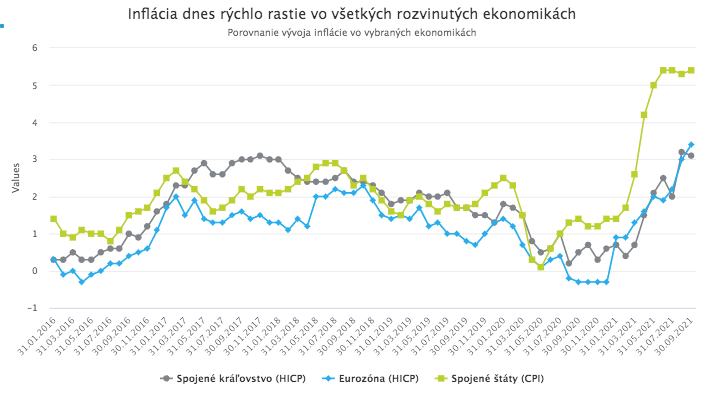

Rising inflation is forcing central banks to raise rates

The rise in short-term yields with minimal changes in long-term yields reflects investors’ expectations that the central banks of the countries whose currencies these bonds are denominated in will raise interest rates in the near future. Investors assume persistently rising inflation will force central banks to do so.

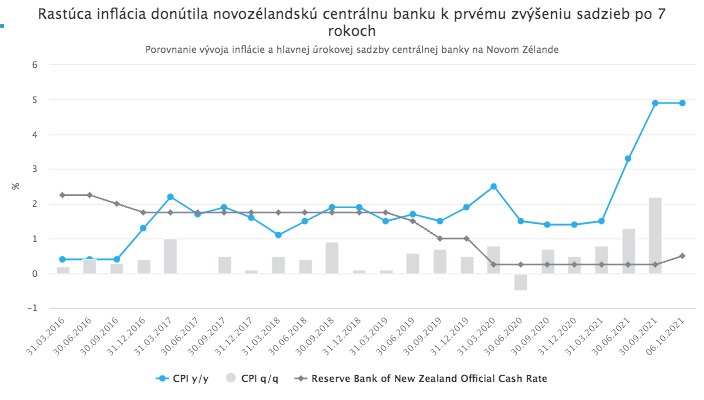

The Reserve Bank of New Zealand already delivered its first rate hike since 2014 in early October in response to rising inflation. A few days later, fresh inflation data showed continued rapid price growth. Consumer prices rose by as much as 2.2% quarter-on-quarter. On a year-on-year basis, inflation rose by 4.9%, far exceeding economists’ expectations. It therefore seems highly likely that the bank will soon have to resort to another rate hike.

Worrying inflation developments are also pushing the Bank of England toward action. While U.K. consumer price growth is still “only” a little over 3% year-on-year, Governor A. Bailey clearly considers it necessary to act.

In a weekend panel discussion, he emphasized that rising energy prices are fueling undesirable inflation expectations: “That is why we, in the Bank of England, have signaled, and we are signaling again, that we will have to act.”

Investors expect the Bank of England to raise its main policy rate by 0.15% as early as the November meeting, which would be the first hike since 2018.

Although rate hikes in the United States and the eurozone are not a matter of the next few months, the sharp and persistent rise in consumer prices is bringing forward the expected timing of the first post-pandemic rate hike in both economic blocs.

Just a few weeks ago, investors and analysts expected the Fed’s first rate increase no earlier than 2023, after the bond purchase program had fully ended. Based on current statements by central bank officials, it appears that the first U.S. rate hike since the outbreak of the pandemic could come as early as the second half of next year.

Finally, movements in the euro money market currently reflect investors’ expectations that the ECB will also raise the deposit rate by 0.1% in the autumn of next year. The ECB is not signaling such a step, and just a few weeks ago nobody expected it could happen in the foreseeable future. However, inflation and the resulting political pressure may not leave it with a choice.

In the current situation, investors are increasingly concerned about interest rate hikes.

Higher rates in a slowing economy are unfavorable for both stocks and bonds

The important signal sent by the flattening of yield curves with respect to expected interest-rate changes and economic growth should be taken into account when making investment decisions.

If interest rates are raised, it is of course negative for publicly traded bonds denominated in the currencies affected. Higher policy rates lead to higher bond yields and thus to lower bond prices.

This expectation is also reflected in the latest Bank of America survey of large fund managers. Allocation to bonds among investors managing more than USD 1.35 trillion has fallen to a record low.

The outlook for equity markets is also not positive. Higher rates and higher yields are generally negative for growth stocks of large technology companies, which today carry enormous weight in major U.S. and global equity indices. We have already seen this dynamic several times this year during periods of sharper yield increases.

Value stocks of smaller-cap companies that performed well in recent months even during periods of rapid yield rises are also unlikely to be immune to declines triggered by rate hikes.

These stocks do perform well in an environment of higher inflation, higher rates, and higher yields, but only when the economy is growing rapidly, or when rapid growth is expected. If, however, central banks amplify the slowdown in economies by raising rates at the wrong time, these types of stocks will struggle.

Bear flattening of yield curves therefore currently reflects investors’ expectations that central banks will raise rates in an attempt to fight persistently rising inflation, thereby contributing to an economic slowdown. Such a scenario is generally negative for both bond and equity markets. Even in a complicated macroeconomic environment, however, it is possible to find securities, as well as entire asset classes, that still have a positive outlook and can deliver stable returns.

At Sympatia, we will be happy to help you select the most suitable investment instruments for any economic environment.