China’s Economy Grew Despite the Pandemic

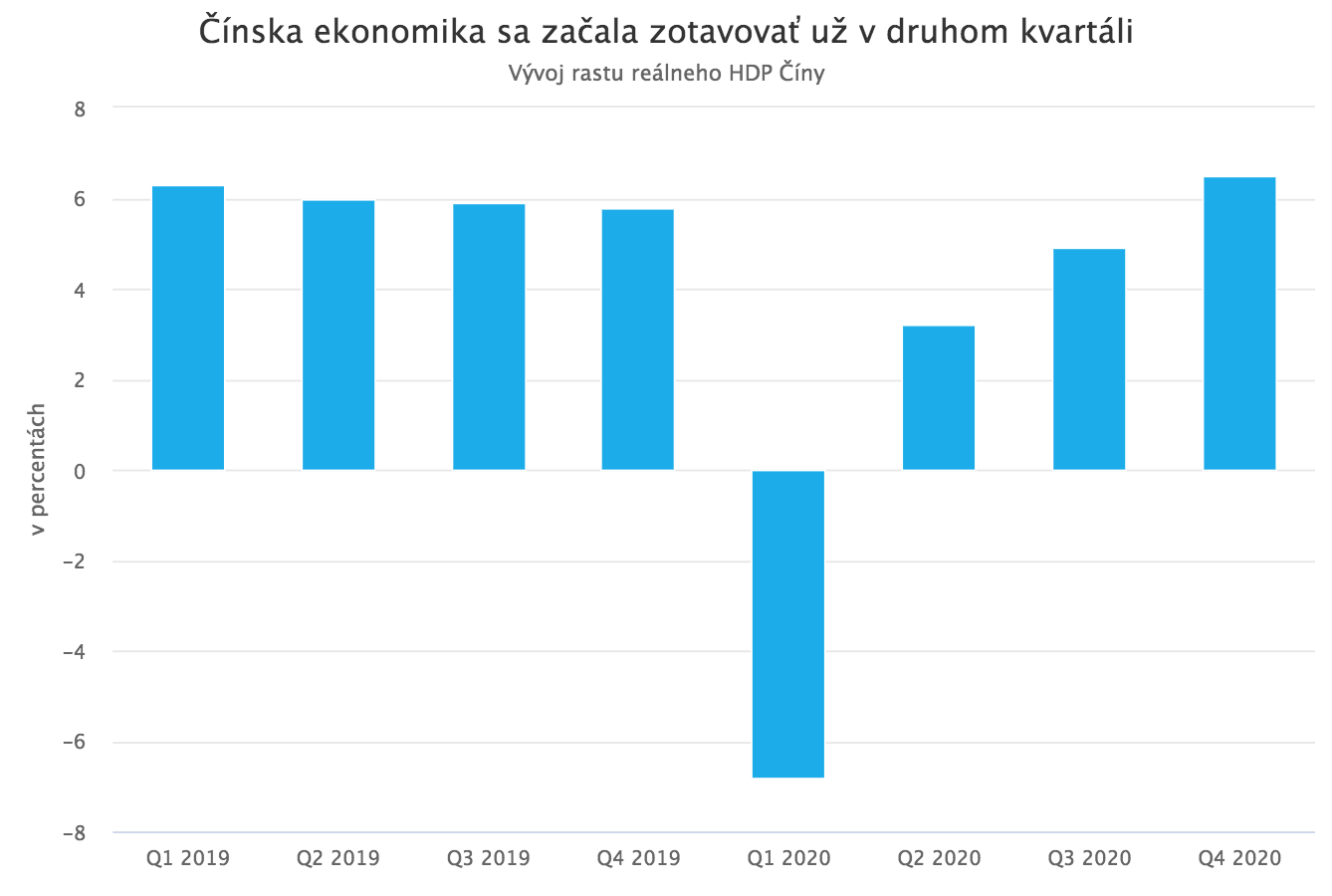

China’s economy began recovering from the pandemic earlier than most of the world, largely thanks to the rapid containment of the virus. After an unprecedented 6.8% contraction in the first quarter, growth returned as early as the second quarter. Data released this week show that fourth-quarter GDP expanded by 6.5%, broadly in line with China’s pre-pandemic pace.

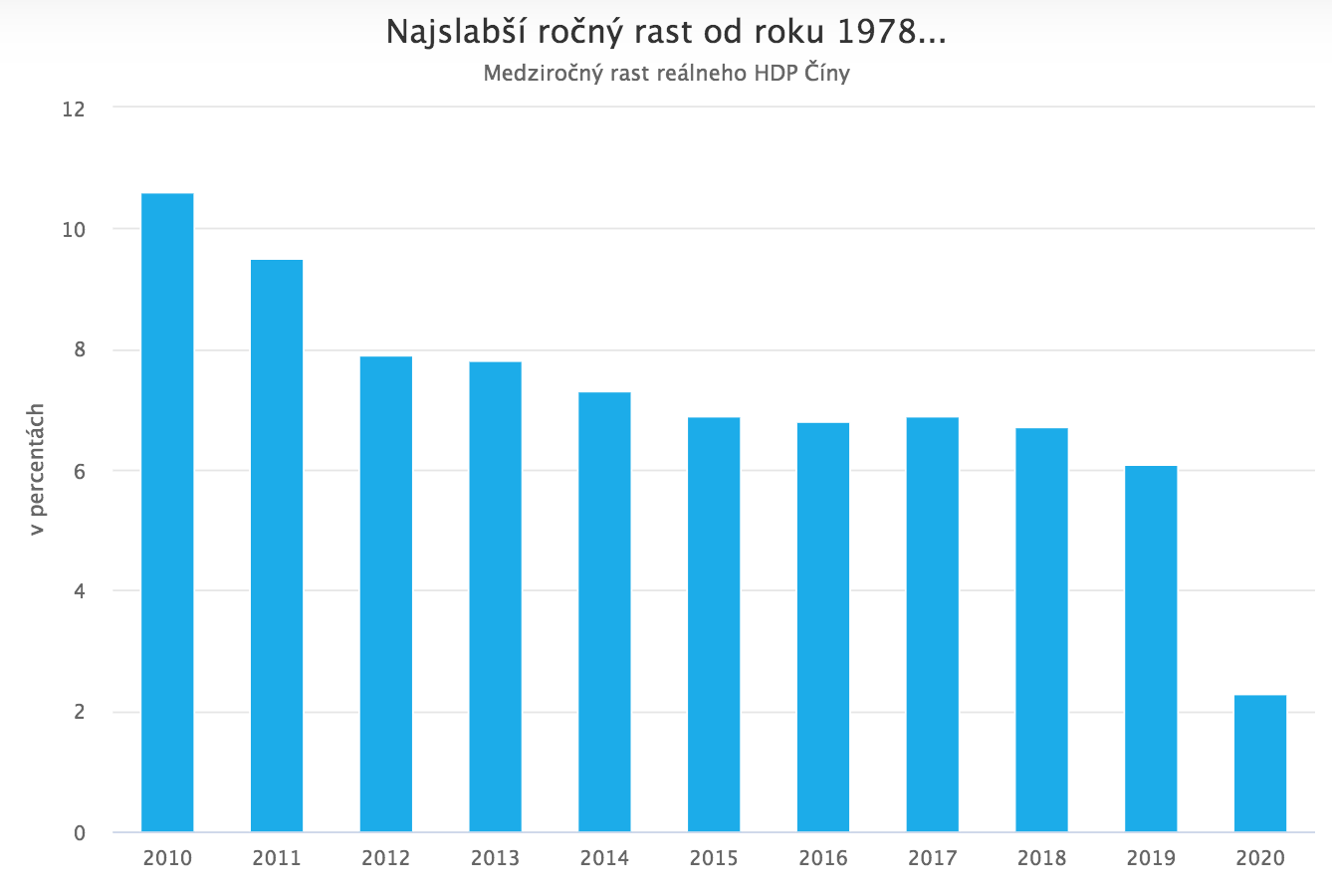

For the full year, growth came in above expectations at 2.3%, helped by the late-year acceleration. The International Monetary Fund had forecast 1.9%. While 2.3% represents a sharp slowdown compared with previous years, and indeed the weakest annual expansion since 1978, it is an outstanding result in global context.

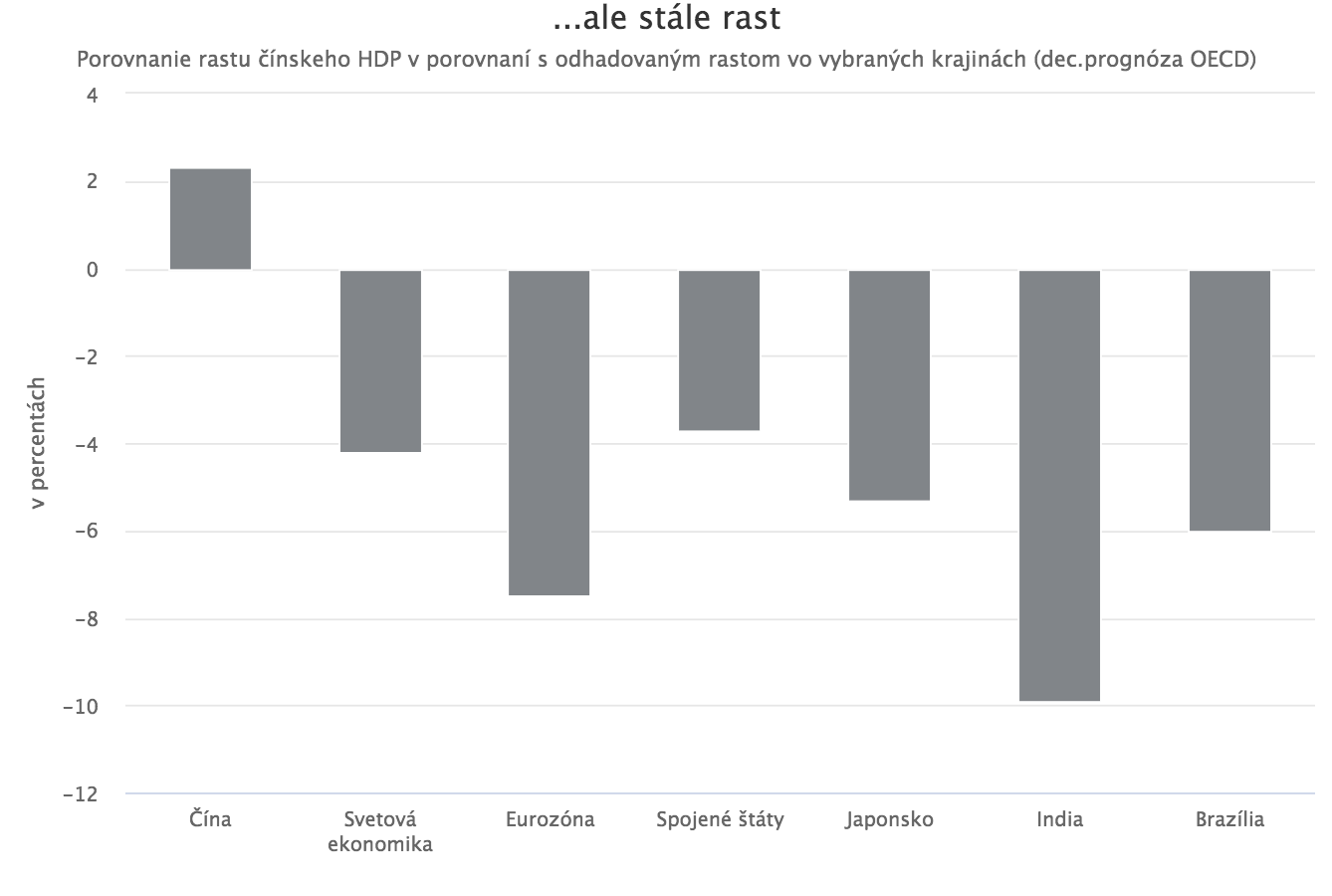

The world economy is estimated to have contracted by roughly 4.2% over the same period, and every major economy recorded a decline. Despite its slowdown, China increased its share of global GDP, and did so at the fastest rate on record.

According to the IMF, this dynamic could bring forward the point at which China overtakes the United States by two years, making it the world’s largest economy as early as 2028.

Growth, but not necessarily healthy growth

The headline figures are undeniably impressive. A closer look at the composition and drivers of last year’s growth, however, suggests that it came at the cost of deepening long-standing and potentially destabilizing domestic imbalances. In that sense, China is still far from a genuinely healthy recovery.

Michael Pettis, a professor of economics at Peking University, likened China’s current performance to a runner who wins a race after taking methamphetamine: first across the finish line, perhaps, but hardly the healthiest athlete. The core issue is that Beijing has once again relied on an old playbook, boosting the very growth engines it had only recently sought to rein in because of their longer-term risks. Chief among them are unproductive investments in infrastructure and real estate, well known through “ghost cities” and “bridges to nowhere.”

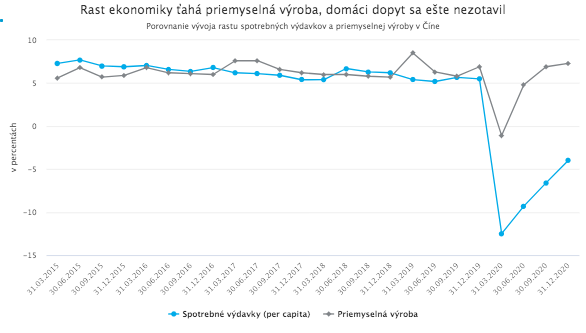

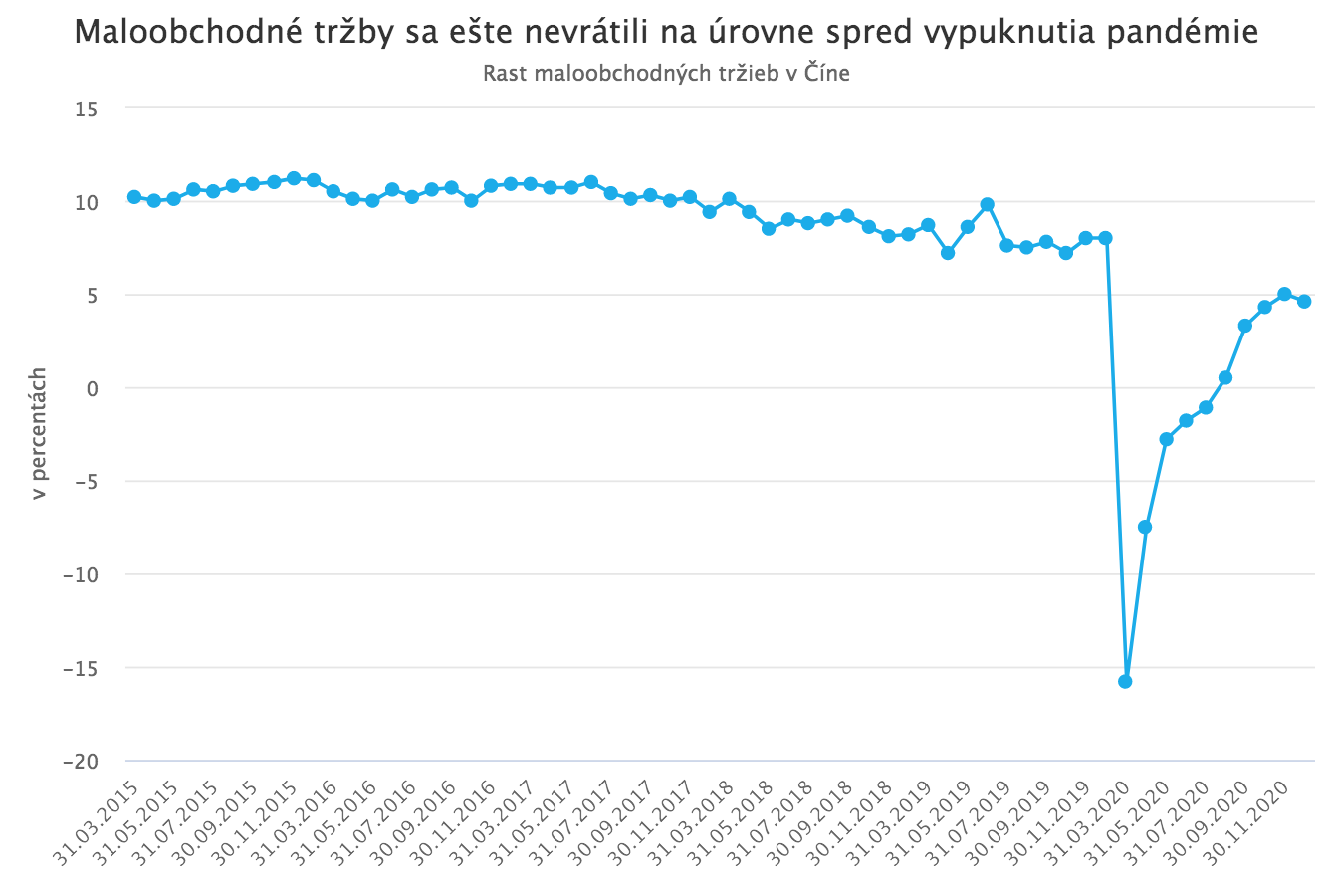

Unlike most countries, China largely avoided direct transfers to households. Instead of stimulating demand, it focused almost exclusively on supply-side support. Consumer spending and retail sales remain well below pre-pandemic levels, while industrial output has reached new highs and is doing most of the heavy lifting for growth.

That combination, record industrial production alongside weak domestic consumption, stands in stark contrast to the government’s long-term objective of reducing reliance on exports and raising the contribution of household consumption to GDP.

New records and widening imbalances

Beyond the lack of direct support, subdued domestic demand reflects a sharp increase in savings and a still-weak labor market, with wage growth stagnating. Another structural challenge is persistent income inequality, which China’s own president has previously cited as a threat to future growth. Fresh data show that the top 20% of earners still make, on average, 10.2 times more than the bottom 20%, one of the highest income gaps globally, and a disparity China has struggled to narrow. The comparable ratio is 8.4 in the United States and around 5 in Western Europe.

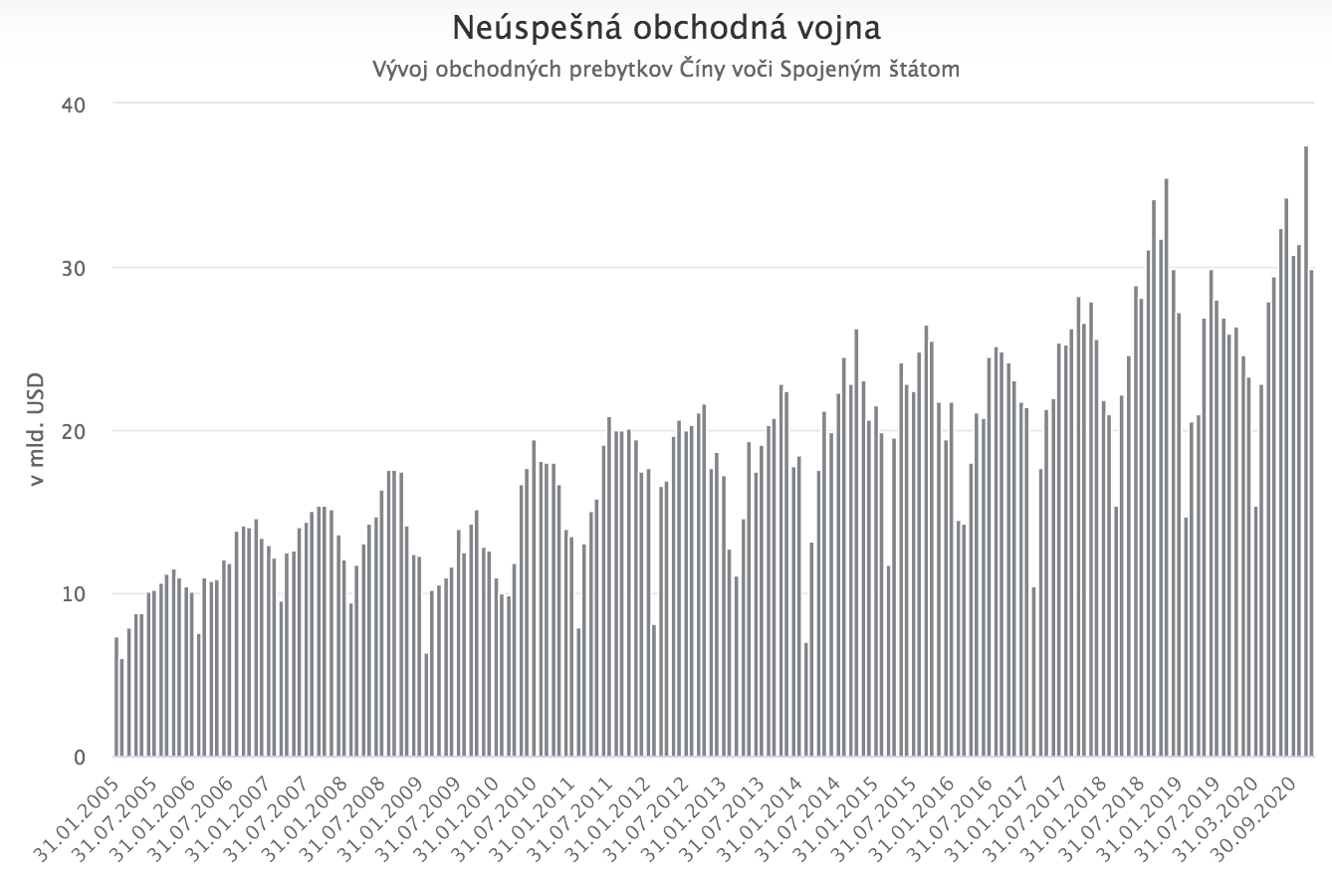

Weak domestic demand alongside rising industrial production has also pushed up China’s external surplus. Exports grew 3.6% last year, while imports fell 1.1%. As a result, China’s current account surplus rose to a record USD 310 billion. China thus overtook Germany (USD 261 billion) to become the world’s largest surplus country.

Notably, China’s trade surplus with the United States also climbed to a record, reaching its all-time high in the very month Donald Trump lost the election. The data suggest that Trump may have suffered a defeat not only at the ballot box but also in his trade war with China, whose stated goal was to reduce that imbalance.

China’s export momentum held up even as the renminbi strengthened against the dollar to its highest level since the summer of 2018. The currency’s steady appreciation in the second half of last year was supported by the recovery in China’s economy and by a monetary stance that has been less accommodative than in the United States or the euro area. China’s benchmark interest rate stands at 3.85%, in sharp contrast to the near-zero or negative rates prevailing in Europe and the U.S.

A potential rebound in consumer spending

China is expected to continue recovering this year, with most forecasts clustering around 7% to 8% growth. It is highly likely that, as the pandemic fades, Beijing will attempt to correct the imbalances described above and shift the composition of growth more toward household consumption.

Consumer spending may also rebound even without explicit demand-side stimulus. As vaccination and reopening reduce uncertainty and strengthen growth, households may lower precautionary savings and start spending accumulated cash balances.

That could create some of the more interesting opportunities in China this year in companies leveraged to domestic consumption. By contrast, the outlook for China’s largest technology firms remains less favorable. Before leaving office, the Trump administration expanded the list of restrictions preventing suppliers from providing key components to Chinese technology companies, led by Huawei. There is little evidence the Biden administration intends to materially change course.

At the same time, privately controlled Chinese technology firms face tightening domestic regulation. Jack Ma’s experience became emblematic: Chinese authorities not only halted the planned IPO of Ant Group, which was set to be the world’s largest, but also effectively sidelined the billionaire himself. After publicly criticizing regulators in November (following criticism of his remarks by the authorities), Ma disappeared from view and only resurfaced this week. Alibaba shares immediately jumped.