Turkey Faces a Potential Currency Crisis

Since the outbreak of the coronavirus crisis, the Turkish lira has depreciated sharply. The Central Bank of the Republic of Turkey (CBRT) and President Erdoğan’s administration have tried to halt the slide, but their room for manoeuvre is limited largely as a result of their own past policy choices. If they fail to stop the weakening, Turkey risks slipping into a full-blown currency crisis.

If you are the president of a country with a high need for external financing and a fragile domestic currency, one that was introduced by redenominating the previous currency and cutting zeros, your priority should be balanced growth, currency stability, and the attraction of foreign investment. If you push growth too hard and an economy fuelled by state-directed credit begins to overheat and generate high inflation that threatens currency stability, you should aim to bring inflation down. In an economy that is partially dollarised and where the private sector carries substantial foreign-currency debt, currency stability is crucial.

In practice, raising interest rates has proven an effective tool to curb inflation. If the governor of your central bank is doing exactly that, you should not interfere or pressure them to cut rates based on idiosyncratic theories that have never been validated in real-world policy. Nor should you undermine central bank independence, which is itself a key pillar of currency stability.

And if a central bank governor ignores your unconventional views, you certainly should not dismiss them and replace them with a loyal family member who will obediently implement economically unsound preferences. Nor should you attempt to “fight” inflation by changing the methodology used to calculate it.

At the same time, you should avoid doing everything possible to deter foreign investors whose capital you need. It would also help not to alienate your most important trading partners and virtually everyone who might be able to extend assistance during a crisis.

Otherwise, you risk leaving both your currency and your economy fragile and exceptionally sensitive to external shocks. And when the largest external shock in modern history hits, you may find yourself in trouble.

President Erdoğan did the exact opposite. Today, Turkey faces the risk of a currency crisis.

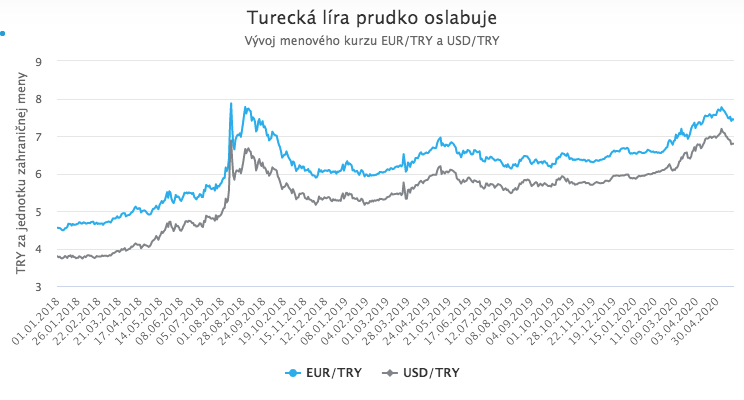

The lira is sliding rapidly and FX reserves are shrinking

Since the onset of the coronavirus pandemic, the Turkish lira has weakened sharply. Against the euro, it fell to its weakest levels since the summer 2018 currency crisis; against the US dollar, it reached an all-time low. In May, the currency stabilised somewhat, largely due to optimistic expectations regarding the reopening of European economies, Turkey’s most important trading partners. Nonetheless, the risk of renewed depreciation remains elevated.

The main driver of the lira’s weakness is, of course, the flight from riskier assets typical in times of crisis, which has also affected other emerging-market currencies and smaller advanced economies. However, when combined with the high level of foreign-currency (especially USD) debt in Turkey’s domestic private sector and the specific features of “Erdonomics,” the lira stands out as one of today’s most vulnerable currencies, facing a heightened risk of a sharp decline.

The lira would likely have depreciated even more in recent weeks had it not been for massive FX interventions by the CBRT. Since the start of the pandemic, the CBRT has spent nearly USD 30 billion to support the lira, rapidly depleting its reserves. Net FX reserves now stand at roughly USD 26 billion. If one adjusts this figure for liabilities stemming from FX swaps, net reserves fall to slightly below zero.

This implies that if pressure on the lira persists, the central bank may soon run out of “ammunition” to defend the currency, at which point the lira could weaken abruptly. Unsurprisingly, the CBRT has been attempting to secure additional reserves, while the Erdoğan administration has introduced other measures to ease pressure on the currency. Yet given the policy choices of recent years, options are limited.

The specific features of “Erdonomics”

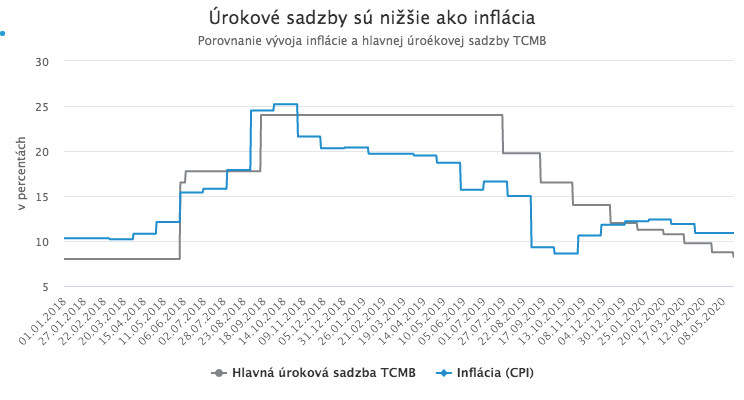

In theory, the most straightforward way to support a currency is to raise interest rates. Higher rates curb inflation and attract foreign investors seeking yield. Turkey, however, has been cutting rates aggressively over the past ten months, since Erdoğan dismissed the previous governor, who had been reluctant to cut rates given the economic backdrop, and replaced him with his loyal son-in-law, Murat Uysal.

Uysal has complied with the president’s wishes and, in ten months, has cut the policy rate nine times, most recently yesterday by 50 basis points. In total, since last summer he has reduced rates by a record 15.75 percentage points, from 24% to 8.25%. At first, these rapid cuts were not problematic because inflation was falling even faster. But in the last quarter of the previous year, inflation began to rise again while rates continued to decline. Early this year, inflation surpassed nominal interest rates. As a result, the real interest rate (adjusted for inflation) turned negative.

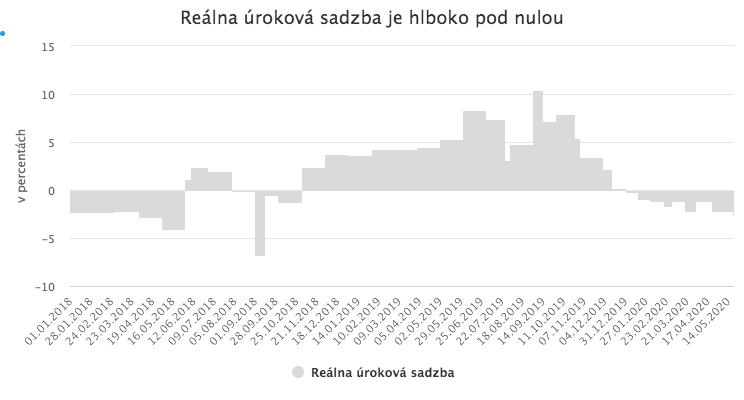

After the latest rate cut, the real policy rate stands at around -2.65%, among the lowest real rates in the world. This is hardly an invitation for the foreign capital Turkey needs to refinance existing foreign-currency debt and fund imports.

How to scare off foreign investors

In the current environment, raising rates is politically and economically unpalatable, as a crisis-hit economy typically requires low rates to stimulate demand. Yet the need for FX reserves has increased further due to the collapse in exports, and a currency crisis would exacerbate an already difficult economic situation. Turkey has therefore been forced to search for other, more complex ways to stabilise the lira and secure foreign currency.

One such approach has been partial capital controls. Turkey’s banking regulator has attempted to prevent foreign investors from “betting” against the lira. Shorting the currency has become extremely costly and technically difficult. On 7 May, Turkey even banned three foreign banks, BNP Paribas, Citibank, and UBS, from conducting lira transactions in the FX market. Although the ban was lifted four days later after producing the opposite effect, it triggered fears of broader capital controls, accelerating outflows and the sale of TRY-denominated assets.

BNP Paribas has not resumed lira trading even after the ban was lifted. Foreign banks remain under investigation for allegedly “coordinating a manipulative attack on the lira.” Domestic banks face restrictions on FX dealings with foreign counterparties. Erdoğan continues to frame developments as a fight against “treacherous Western attacks” aimed at ruining the Turkish economy, while additional measures limiting foreign investors’ access to lira trading remain in place.

These partial controls have been effective in one sense. The share of foreign investors in total lira trading volume has fallen over the past month to less than one-third, the lowest level in ten years. In summer 2018, by contrast, it stood at 65%. However, restricting foreigners’ ability to trade the lira not only reduces speculative pressure; it also discourages foreign investors from purchasing Turkish assets and investing in the country. While it may ease immediate pressure on the lira, it does nothing to bring in the foreign currency Turkey urgently needs, in fact it may do the opposite.

Burned bridges

In its attempt to secure FX liquidity, Turkey has turned to foreign central banks to request swap lines. Yet because Erdoğan has spent recent years alienating the EU and the United States, whose currencies Turkey needs most, progress has been limited. The Federal Reserve reportedly rejected a USD swap line with the CBRT, noting that such arrangements are reserved for countries with a “relationship based on mutual trust.” Trust has hardly been strengthened by Turkey’s purchase of the Russian S-400 air defence system as a NATO member despite US threats of sanctions, its assistance to Iran in circumventing sanctions, the detention of an American pastor, and similar actions.

The ECB has also reportedly declined Turkey’s request for a euro swap line. This is not surprising. The EU has long criticised Turkey’s human rights record as well as its military operations, which have at times been alleged to amount to war crimes. Erdoğan’s repeated threats to “open the gates” and allow migrants to enter the EU have further strained relations.

Erdoğan has also pre-emptively slammed the door on potential IMF assistance. He frequently declares that he will “never bow to the IMF,” describing it as a “tool of Western imperialism.” Turkey has therefore had to seek swap lines with other countries, even though it primarily needs dollars and euros. It has pinned hopes on negotiations with the Bank of Japan and the Bank of England. Earlier this week, reports suggested a deal with both central banks was imminent and would involve USD 10 billion swap lines with each. Both banks denied the reports, and talks continue.

This week, however, Turkey did secure a tripling of its existing swap line with Qatar, from USD 5 billion to USD 15 billion. While the Qatari riyal is neither the dollar nor the euro, it is a “harder” currency than the lira, and the swap could provide some relief.

Political manoeuvring can avert even a currency crisis

It is therefore possible that Erdoğan may manage to navigate out of this difficult situation and avert a currency crisis. The economy is separate from politics only in textbook models; in reality, it is inseparable from a country’s political positioning. Strong political leverage can compensate for economic mismanagement. And Erdoğan has repeatedly demonstrated a capacity to exploit Turkey’s strategically advantageous geography and geopolitical position. For that reason, even more severe episodes than economic amateurism and provocations toward the very countries whose currencies Turkey needs have, at times, been tolerated.

Recall that Turkey has NATO’s second-largest army and occupies a strategic position between Europe and the Middle East. In pursuing its own interests, it deftly oscillates between the US, the EU, Russia, and increasingly China. Erdoğan is also a major power broker in the Middle East, benefiting from Turkey’s active involvement in proxy conflicts in Syria and Libya.

The question of whether Turkey will fall into a currency crisis cannot be separated from whether the EU would risk destabilising a country hosting millions of refugees on its borders, whether the US might ultimately seek a compromise to keep Turkey anchored in NATO, whether Russia or China might attempt to pull Turkey decisively out of NATO in exchange for economic support, and whether any of the actors in the proxy wars in Syria and Libya may require Turkish military-strategic concessions.

Finally, Qatar did not increase the size of its swap line with Turkey because it was economically attractive. The reasons are political. Turkey has supported Qatar, its ally since the Syrian conflict, politically and logistically, helping it withstand the regional isolation imposed by other Gulf states after Qatar sought to balance Saudi influence by moving closer to Iran.