European Commission Unveils a Landmark Recovery Plan; Markets Welcome the Proposal

European Commission President Ursula von der Leyen on Wednesday presented to the European Parliament an ambitious plan to revive the European economy in the wake of the Covid-19 crisis. In both scale and the instruments deployed, the proposal is historic and without precedent. It has been described as a “fiscal bazooka” and as “the largest political shift on the European continent in 30 years.”

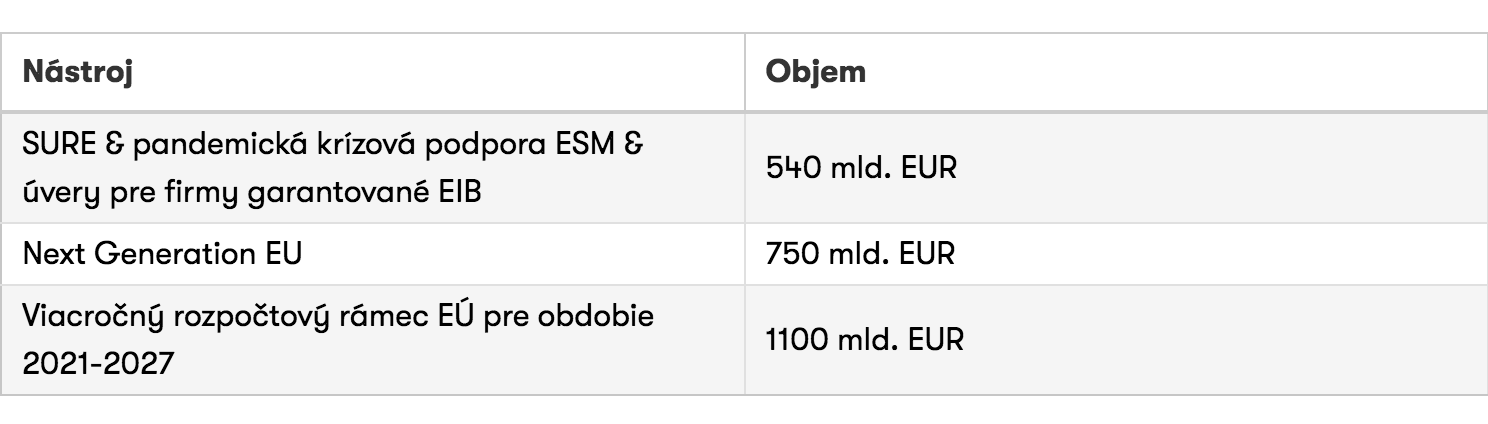

At the core of the package is a proposal to establish the Next Generation EU recovery fund with a headline size of up to EUR 750 billion. The fund would complement and expand the EU’s planned 2021 to 2027 budget framework, which on its own amounts to EUR 1.1 trillion. This would lift the EU’s overall budgetary capacity to EUR 1.85 trillion.

Next Generation EU would be the EU’s second extraordinary instrument in response to the pandemic. The first, a EUR 540 billion safety net agreed on 23 April, was intended as immediate “first aid” for the hardest-hit countries and businesses. The new fund is designed to support member states’ post-crisis recovery via a combination of grants and loans.

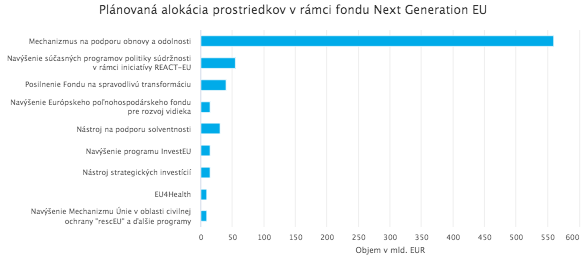

Of the total envelope, EUR 500 billion would be distributed as grants and EUR 250 billion as concessional loans. The fund’s tools and programmes are formally organized into three pillars:

Supporting member states’ investment and reform efforts

Kick-starting the EU economy via incentives for private investment

Drawing lessons from the crisis

The largest component by far is the Recovery and Resilience Facility (RRF), with capacity of up to EUR 560 billion. As part of the first pillar, the RRF would provide funding for member states’ investment and reform agendas, with priority given to digitalization and the green transition. Up to EUR 310 billion could be disbursed as grants, with the remaining EUR 250 billion offered as loans.

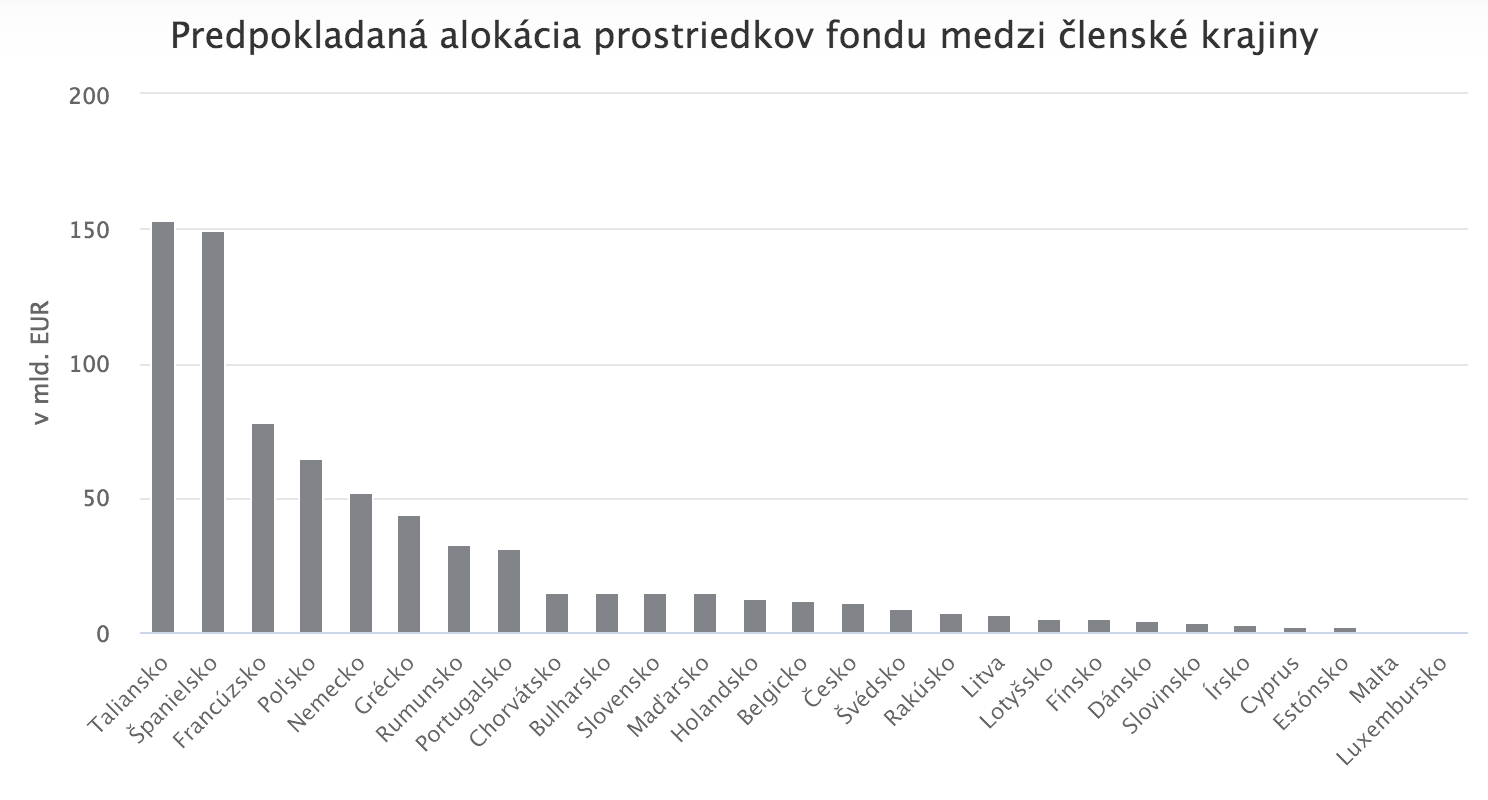

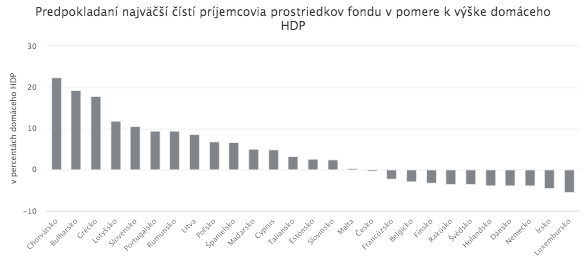

The largest nominal allocations would go to countries most severely hit by the pandemic, notably Italy (EUR 153 billion) and Spain (EUR 149.3 billion). In GDP terms, however, smaller countries, including Slovakia, are expected to rank among the biggest net recipients.

While the size of the programme is striking and historically unprecedented (though it remains unclear whether it will be sufficient), the truly transformative element lies in the proposed financing mechanism.

A revolutionary financing model

The Commission intends to raise funding by issuing bonds in the capital markets, borrowing up to EUR 750 billion in total. Critically, these securities would be issued by the European Commission itself, rather than by individual member states. In effect, this amounts to the EU issuing joint debt backed by all member states, irrespective of which countries ultimately receive the support.

This represents a decisive step toward a form of fiscal union. For years, several northern countries led by Germany opposed such a move, wary of implicitly guaranteeing the liabilities of highly indebted southern member states. Bonds issued in this way are, in substance, close to the so-called “corona bonds” that many member states had firmly rejected only weeks earlier. A key turning point was Chancellor Angela Merkel’s shift in position.

That shift reportedly coincided with a ruling by Germany’s Constitutional Court questioning the compatibility of the ECB’s bond purchases with Germany’s constitution (even though the ECB has not regarded itself as bound by the judgment). The ECB has carried much of the crisis-response burden through asset purchases; a meaningful constraint on this channel would have left the euro area with a dangerous policy gap.

A clear advantage of joint EU issuance is that the EU, represented by the Commission, can borrow on better terms than weaker, more indebted member states could achieve on their own. The Commission has a top-tier AAA rating, allowing it to mobilize funding at significantly more favorable conditions than, for example, Italy, Spain, or Greece.

Technically, the Commission would back the issuance using its budgetary headroom, specifically the gap between (i) the maximum level of resources it can call from member states and (ii) the expenditure ceiling in the EU budget. The ceiling on own resources has been increased to 2% of member states’ gross national income.

Bond issuance would take place over 2020 to 2024, with maturities ranging from 3 to 30 years. Repayment would be scheduled for 2027 to 2058, financed from future EU budgets. The loan portion would be repaid by the member states receiving the loans.

The Commission also proposes to explore new EU “own resources” to ease the burden on national contributions. Potential sources include expanding emissions trading to aviation and shipping and/or introducing new EU-wide levies (for example, a digital tax, carbon-related taxes, or a tax on large companies “benefiting significantly from the single market”). This, too, would be a significant institutional shift. EU federalists have argued for stronger own resources for years, while other political factions have fiercely resisted them.

The recovery fund, and in particular its financing, therefore marks a major milestone in EU history. The Commission frames the tool as “exceptional” and “temporary”; in economic policy, however, temporary exceptions often have a tendency to become permanent.

Support arrives just in time

The Commission’s proposal comes at a critical moment, especially given the long path to approval. EU leaders will begin negotiations at the June European Council summit, but the package is expected to be agreed only toward the end of the year, with a potential start date of 1 January 2021.

Unanimous approval will be required, meaning protracted and difficult negotiations are likely, similar to those surrounding the EU’s multiannual budget. Germany’s shift is central, but the so-called “frugal four” (Austria, the Netherlands, Denmark, and Sweden, sometimes labelled by southern member states as the “stingy four”) remain opposed. They appear to have accepted joint issuance in principle, but argue that support should be provided only as loans, not grants.

The package will likely pass given support from the largest member states, including Germany, though changes are possible, including adjustments to the grants-to-loans mix or additional conditionality governing access. The key, however, is speed and preserving sufficient scale.

ECB President Christine Lagarde noted this week that euro area economic performance currently sits between the “baseline” and “severe” scenarios outlined after the pandemic began. To date, the ECB has carried much of the stabilization burden, and Lagarde has repeatedly urged EU leaders to agree a meaningful fiscal package, warning that the ECB’s toolkit is limited. The central bank’s most powerful instrument remains asset purchases, and even that programme will likely need to be expanded, as the originally approved EUR 750 billion envelope may prove insufficient.

Without agreement on the Commission’s plan, the euro area would face a significant risk of another sovereign debt crisis that could threaten the integrity of the currency union. The countries hit hardest by the pandemic are largely in southern Europe, where debt levels were already elevated before the crisis. They are also disproportionately exposed to a collapse in summer tourism, implying an additional sharp hit to revenues. Without massive fiscal support, a debt crisis would be likely, potentially devastating domestic economies and strengthening euro-sceptic and EU-exit movements that are already influential in countries such as Italy, partly due to perceptions of insufficient EU support in the early stages of the pandemic.

Market reaction

Markets welcomed the Commission’s proposal. Together with the reopening of European economies, the plan helped underpin a more optimistic tone in European markets this week, tempered only by escalating U.S. China tensions and President Trump’s attacks on technology companies.

The euro strengthened to its highest level in the past two months. The plan could also have meaningful implications for the euro’s longer-term status as a reserve currency. If an “exceptional” tool were to become permanent and joint EU issuance continued at scale beyond the programme, the euro’s reserve-currency standing could be materially strengthened.

One of the key factors limiting the euro’s role as a global reserve currency is the scarcity of safe euro-denominated assets. Countries with the safest government bonds, such as Germany and the Netherlands, issue relatively limited volumes compared with the U.S. or Japan, while bonds issued by other euro area countries are not viewed as risk-free. This reduces investors’ willingness to hold large euro reserves due to the lack of sufficiently deep, low-risk instruments in which to park them.

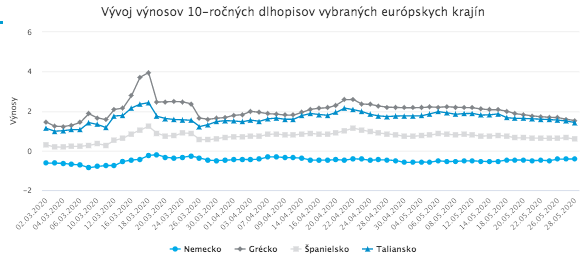

A pronounced response was also visible in bond markets. Yields on bonds of higher-risk countries such as Italy, Spain, and Greece, which would benefit most from the recovery fund, fell sharply. By contrast, yields on the safest German bonds rose modestly, as investors often hold them as protection against adverse tail-risk scenarios.

European equities, buoyed by the improved sentiment, recorded five consecutive days of gains and reached their highest levels since the March sell-off.