The US Senate Delays the Threat of a Sovereign Default

US lawmakers reached a last-minute agreement to raise the federal debt ceiling, averting the risk of a technical default by the United States. Markets breathed a sigh of relief, but likely only briefly. The agreed increase of USD 480 billion is expected to last only until early December. In a matter of weeks, this absurd political drama, with potentially catastrophic implications for financial markets and the economy, will return. What is the dispute really about, and what is at stake if politicians fail to reach a deal in December?

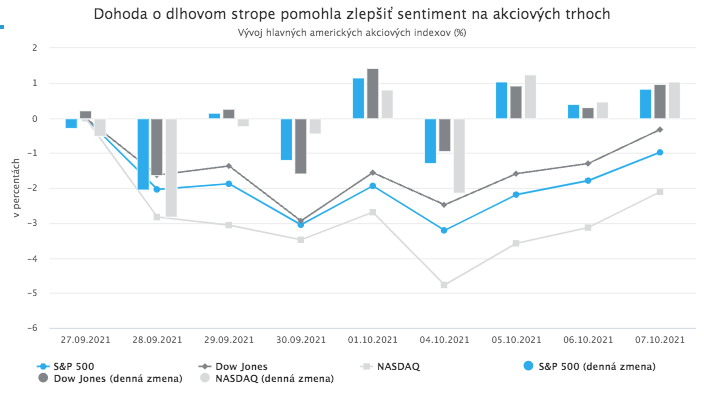

When US politicians struck a deal over Wednesday and Thursday to raise the debt ceiling, investors welcomed the news. Equity markets halted their recent declines and moved higher.

Against the backdrop of a looming energy crisis, elevated inflation, rapidly rising yields, and persistent problems in the Chinese economy, the prospect of another political standoff with potentially severe consequences was the last thing markets needed.

Still, the Senate-approved deal is only a stopgap. Raising the debt ceiling by USD 480 billion allows the US government to continue meeting its obligations only until 3 December 2021. Unless lawmakers agree on a more durable solution by then, the threat of US payment incapacity will once again be on the table.

The debt ceiling: a tool of fiscal discipline or a pointless constraint?

The debt ceiling debate is now deeply politicized and often deliberately distorted. It is therefore useful to restate what is actually at issue.

The debt ceiling sets a maximum level for total federal government debt. Intuitively, it may sound like a fiscally responsible measure designed to prevent excessive spending and borrowing.

In reality, it is not. The debt ceiling has no direct link to future government spending or to future budget deficits. Raising it does not automatically mean that the government will spend more or borrow more going forward. All planned federal expenditures are authorized by Congress through the budget process.

Instead, the debt ceiling merely caps the amount of debt the Treasury can issue to finance spending that Congress has already approved. More than 90 percent of routine outlays go to programs enacted by previous administrations.

In this sense, the rule is largely an unnecessary complication. It places a technical constraint on financing already-approved expenditures. Congress can raise the ceiling at any time, and has done so more than 80 times since it was introduced in 1917.

For most of its history, increasing the debt ceiling was treated as a routine technical step that both Republicans and Democrats could support. Political conflict naturally focused on the budget itself and the approval of spending, not on the mechanics of financing it.

Debt can rise by an additional USD 480 billion

Total US federal debt hit the statutory limit of USD 28.4 trillion on 1 August this year, when the debt ceiling was reinstated after a two-year suspension approved in 2019. For more than two months, the Treasury has relied on so-called extraordinary measures, using existing cash balances and accounting maneuvers to keep funding government operations.

On 28 September, Treasury Secretary Janet Yellen warned lawmakers that these measures could finance federal spending only until 18 October.

If Congress failed to raise or suspend the debt ceiling by then, the United States would not have sufficient funds to meet all its obligations. Yellen stressed that such an outcome would have catastrophic consequences.

Lawmakers, preoccupied with negotiations over the size of a new fiscal stimulus package, did not rush to resolve the issue. On the contrary, both parties sought political advantage. Democrats, holding a narrow Senate majority, technically had enough votes to raise the ceiling without Republican support, but insisted that Republicans share responsibility by voting for the increase.

The goal was to prevent Republicans from later weaponizing the issue in campaign messaging, framed misleadingly as a question of fiscal responsibility. Republicans, for their part, saw little reason to help Democrats. Both sides theatrically accused the other of causing the looming crisis.

While almost everyone assumed that politicians would ultimately come to their senses and would not risk a US default for the sake of partisan conflict, the probability of an extreme outcome was no longer zero. President Biden himself declined to rule it out.

Financial markets, already unsettled by a range of risk factors in recent days, had yet another source of uncertainty. As noted above, Democrats and Republicans ultimately agreed on a temporary fix, raising the ceiling by just USD 480 billion. The problem has not been solved, only postponed until early December. According to current Treasury estimates, the US will again hit the higher statutory limit on 3 December 2021.

Is a market and economic catastrophe on the horizon?

In less than two months, the political drama of recent days will likely repeat. It may be even more intense, and reaching an agreement may be even more difficult. At the same time, Democrats will be pushing to pass a new spending package, and as is often the case in December, a government shutdown could also come into play.

From a market perspective, the December environment could be further complicated by the expected start of Federal Reserve tapering. If the winter is cold, an energy crunch could add pressure as well. This year, markets may not enjoy the usual year-end calm or a “Santa Claus rally”.

Our base case is that Congress will ultimately reach some temporary agreement in December, perhaps extending the ceiling for a few months. But what if lawmakers fail to agree and the US government genuinely lacks sufficient funds to meet its obligations? Would financial markets face an apocalypse?

Everything would depend on how long such a situation lasted. If it persisted for only a few hours or days, no disaster would occur, neither in the economy nor in financial markets. Some government payments would be delayed, but even a brief delay in servicing Treasury securities would not, by itself, trigger a meltdown.

The Federal Reserve has ample tools to limit the negative impact of such delays on the financial system. Paradoxically, demand for US Treasuries and for the dollar could even rise under such a scenario, much as it did during the 2011 debt-ceiling standoff, which ultimately led S&P to downgrade the US credit rating.

If, however, US payment incapacity were to last for months, or if the country were to declare an outright default, the consequences would be catastrophic. The global financial system and the world economy still rest heavily on the dollar and on US government bonds.

That said, the risk of such an outcome remains very low, and it would be absurd for it to occur. The United States is monetarily sovereign. Its obligations are denominated in dollars, a currency it issues itself.

The US government’s ability to meet its obligations is constrained only by rules such as the debt ceiling, which politicians created and can amend, modify, or abolish at any time. Faced with a genuine threat of economic and financial collapse, one would hope that lawmakers would find the political will to do so.