Google Faces a Serious Antitrust Lawsuit. Is the Era of Unrestricted Growth in Tech Stocks Coming to an End?

The lawsuit against Google is the most significant antitrust action by U.S. authorities since the campaign against Microsoft in the late 1990s. Will it bring an end to the era of unlimited growth for a handful of the largest technology companies that have, for several years now, been lifting almost the entire U.S. stock market on their own?

We ended our August article Can tech stocks rise indefinitely? with a warning that the biggest and, in the short term, most likely obstacle to further growth would be a potential antitrust case. It seems that this obstacle has just arrived.

On October 20, the U.S. Department of Justice filed an antitrust lawsuit against Google for violating competition law. In other words, it accuses the company of monopolistic practices and suppressing competition. This is the most significant antitrust proceeding in the United States in more than 20 years, with potentially far-reaching consequences for the entire U.S. stock market.

What is the lawsuit about?

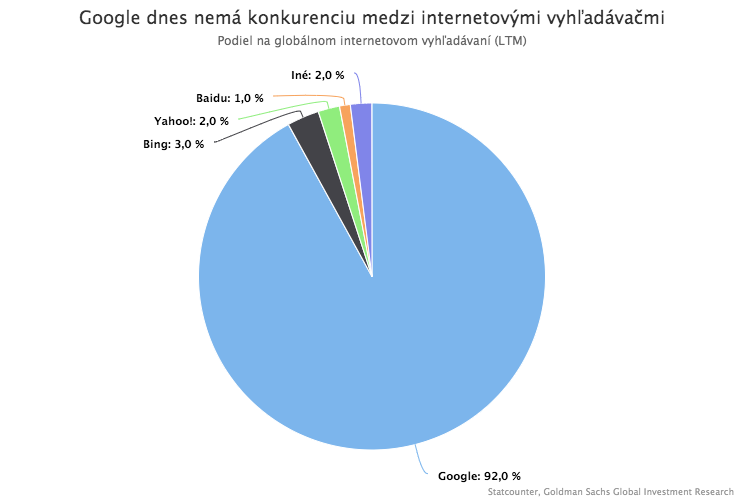

The lawsuit focuses on Google’s practices in securing the monopoly position of its search engine, namely the contracts Google entered into with manufacturers of phones, other electronic devices, and web browsers. These contracts ensure that Google is set as the default search engine on those devices and browsers. That gives Google a significant advantage, since only a small minority of consumers ever change their default search engine. In exchange, the contracting parties receive a share of Google’s advertising revenues and other financial benefits.

Google has such an agreement, for example, with another tech giant, Apple. In order to be the default search engine on Apple devices, Google is estimated to pay the company with the apple logo roughly USD 8 to 12 billion per year. This relationship is crucial for both firms. Google estimates that as much as 50% of searches originate from Apple devices. At the same time, payments from Google account for an estimated 15% to 20% of Apple’s profits.

According to the lawsuit, Google also gained, thanks to these contracts (signed back when Bing and Yahoo! could still represent real competition), today’s absolutely dominant position among web search engines.

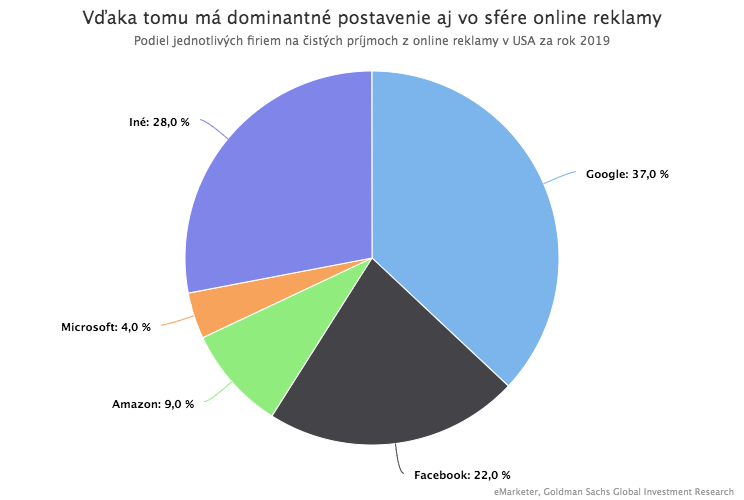

Thanks to this position, it became the “gatekeeper” of the internet, gained a dominant position in online advertising, and, of course, secured a constant inflow of enormous amounts of user data.

How will it end?

Google is, naturally, defending itself against the lawsuit. It argues that users use Google not because they have no other choice, but because they want to, since Google is simply the best search engine. The company claims its contracts with phone and device manufacturers do not violate competition law, comparing them to agreements cereal manufacturers make with supermarkets to place their product in a prominent spot on a shelf.

Experts, however, estimate that the lawsuit has a fairly high chance of success. Its strong point is that it focuses on one easily demonstrable monopolistic practice in the form of the aforementioned contracts with other companies. Both in its importance and in its content, it therefore resembles the lawsuit that forced Microsoft to change some of its monopolistic practices at the end of the 1990s, making room for companies like Google.

G. Reback of Carr & Ferrell LLP, an attorney specializing in competition-law violations, commented as follows: “It’s not that Google just has a better shelf position than its competitors. It’s in all the shelves, and the competition is in another store 400 miles away in a questionable neighborhood.”

Proving that Google engaged in practices harmful to competition should therefore be relatively straightforward. The problem may be demonstrating their negative impact on consumers, since the product itself is free and outdated antitrust laws focus on negative price effects of monopolies on consumers.

What is certain is that the lawsuit will be followed by long court battles lasting several years. Google currently has more than USD 120 billion in cash and liquid assets. It will not skimp on lawyers. For now, it is also unclear what would happen if Google were to lose the case. The Department of Justice has not yet specified the remedies it is seeking. However, officials have not ruled out any options in public statements. In the extreme case, the company could theoretically even face a breakup.

The first shot in the coming antitrust barrage

Regardless of how this lawsuit ends, its significance lies mainly in the fact that it appears to be only the first shot in a coming antitrust barrage.

In the United States alone, as many as 48 state attorneys general are conducting separate investigations into Google’s practices. Eleven of them joined the current lawsuit. A large group of states is also preparing another joint lawsuit focused on the company’s monopoly position in online advertising. Other “Big Tech” firms such as Facebook, Apple, and Amazon are likewise already targets of intense scrutiny by authorities due to their monopolistic practices.

Constraints on the monopoly power of these firms may also come from Congress in the form of legislative interventions. This is one of the few priorities on which Republicans and Democrats agree.

Democrats on the House antitrust subcommittee published this month the results of a 16-month investigation into the practices of Google, Facebook, Apple, and Amazon. They concluded that the firms engage in harmful monopolistic practices and recommended legislative action. Republicans are not far behind. William Barr, the federal attorney general, regarded as a close ally of Trump, personally oversaw the current lawsuit against Google and pushed for it to be filed before the election. Trump himself has also repeatedly spoken out sharply against the monopoly positions of companies such as Google and Amazon.

It therefore seems certain that, regardless of how the November election turns out, the campaign against a handful of the largest technology companies will continue. This, in turn, could have a fundamental impact not only on the companies directly affected, but also on the entire U.S. stock market.

Will antitrust enforcement end the dominance of the U.S. stock market?

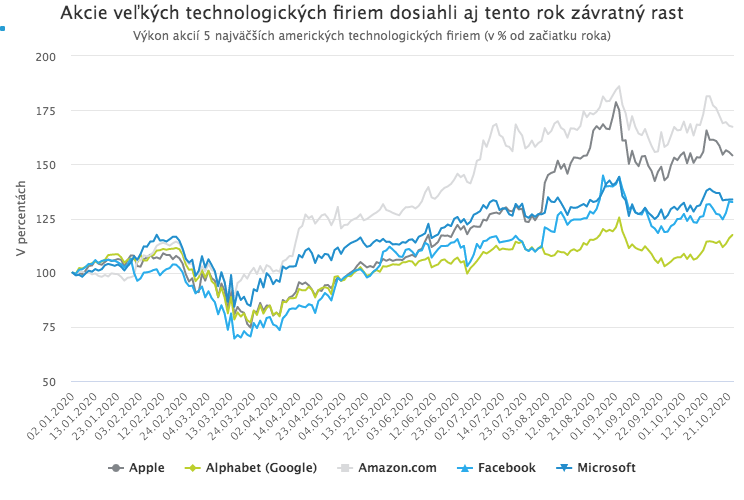

Shares of a handful of the largest U.S. technology companies, threatened by antitrust action, have for several years been a pillar of the entire U.S. stock market. Their dizzying rise was not stopped even by the pandemic. Quite the contrary; changes in consumer behavior caused by the pandemic have only benefited these companies. As a result, their stocks have been among the best-performing assets in the world this year.

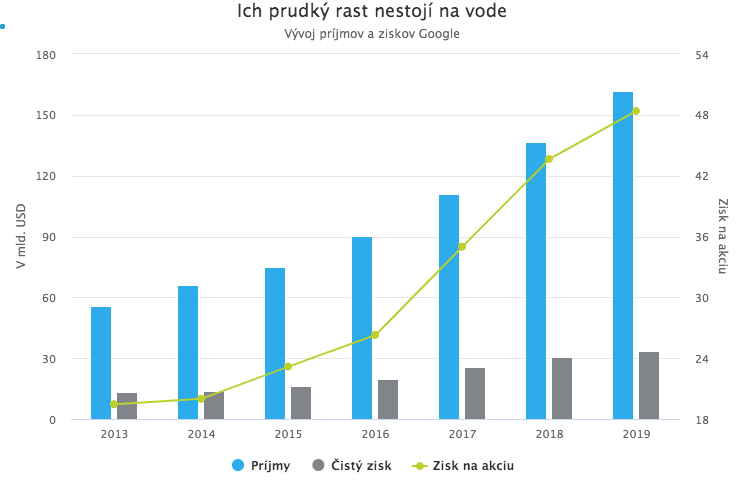

Their continued rapid growth is not driven solely by mania like during the tech-stock bubble at the turn of the millennium. It is supported by real and growing profits, although, of course, various technical and speculative factors also play a role.

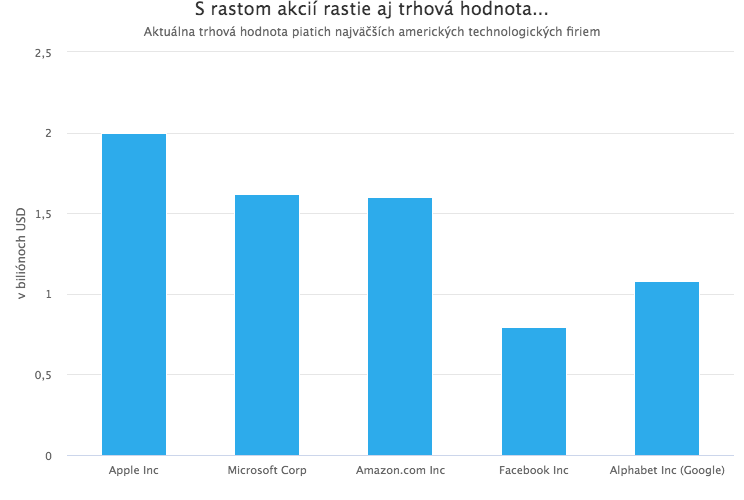

In any case, this ongoing surge has pushed the market value of the largest technology firms into the stratosphere. The market capitalization of four of them exceeds one trillion dollars.

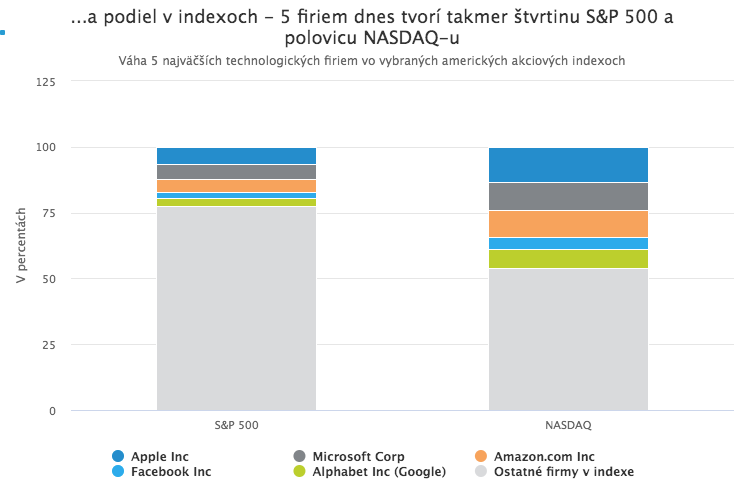

The gigantic market capitalization of these firms means that in the most popular equity indices, which are market-cap weighted, they now have a record-high share. The performance of the entire U.S. stock market (as measured by indices) therefore depends to a large extent on the continued strong growth of a handful of the largest companies.

The five largest technology companies, known in markets by the acronym FAAMG (Facebook, Apple, Amazon, Microsoft, Google/Alphabet), now make up as much as 22.6% of the S&P 500 index, which is considered the benchmark for the entire stock market. In the popular NASDAQ technology index, their concentration is even higher. These five companies account for nearly 46% of the index’s total market value.

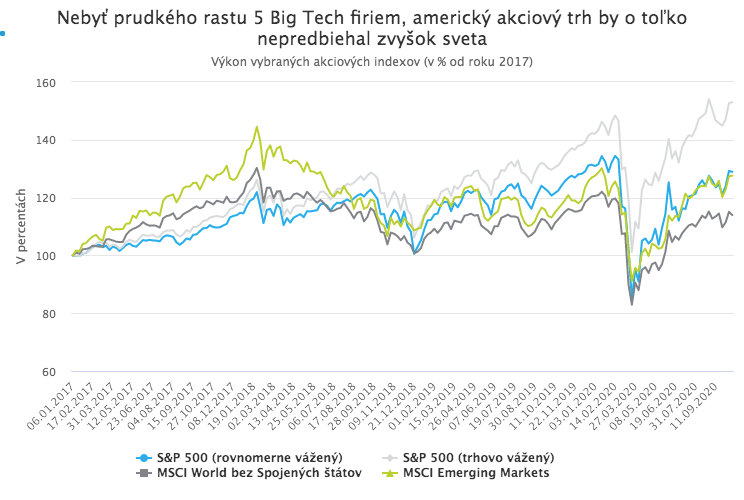

The strong growth of these firms and their enormous weight in the main stock indices is (not only) this year virtually the only reason for the exceptionally strong performance of the U.S. stock market compared with the rest of the world. The dramatic difference between the performance of these five firms and the remaining 495 companies in the S&P 500 was especially visible in the second quarter. While FAAMG achieved, on average, 2% growth in earnings per share during that period, the remaining 495 companies in the index suffered, on average, a 38% decline in earnings per share.

The long-term dependence of the U.S. stock market on the performance of a few of the largest technology firms is also well illustrated by the following chart. It compares the performance of the benchmark U.S. S&P 500 index in its current market-cap weighted form (with a high weight for the five largest “big tech” firms) with its hypothetical equal-weighted version, in which fast-growing technology firms do not have such an enormous share. We can see that such an index would not so significantly outperform equity markets in the rest of the world.

The lawsuit against Google, signaling the start of antitrust action against the largest technology companies, may therefore, among other things, bring an end to the above-average performance of the U.S. stock market compared with the rest of the world. Investors should keep this risk in mind.