The Fed Got Spooked by Inflation, Markets Got Spooked by the Fed, and the Fed Got Spooked by Markets

Despite their previous statements, Fed officials have apparently become alarmed by the rise in inflation and, at last week’s meeting, signaled a tighter monetary policy sooner than expected. In doing so, they frightened investors who had grown accustomed to an extremely loose monetary policy. However, the subsequent sharp market moves in turn alarmed the Fed, prompting its officials to walk back their earlier messaging and reassure markets that no monetary tightening would take place in the foreseeable future.

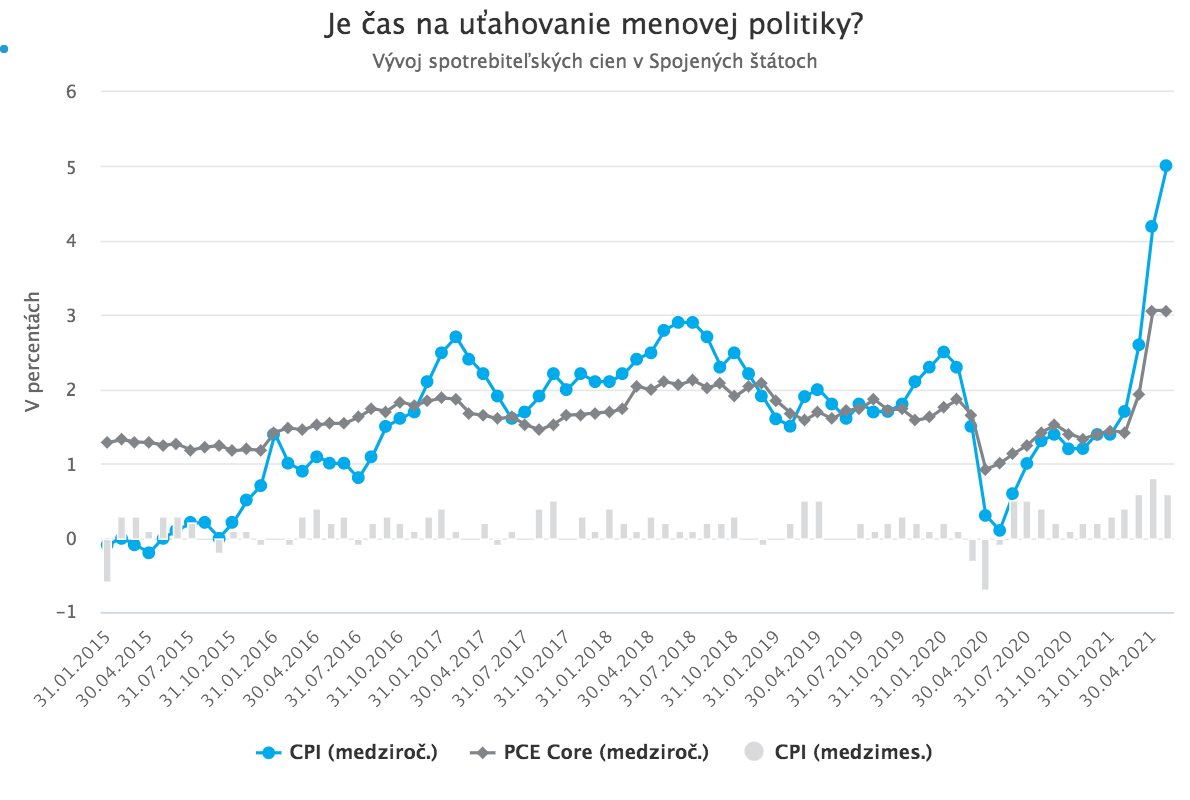

It was expected that last week’s Fed meeting would bring no major steps or surprises. The current rise in inflation in the United States has certainly worried some economists and investors, but in recent weeks Fed officials had repeatedly emphasized that they see it as only temporary. In any case, in favor of a full recovery of the economy and the labor market, they were willing to temporarily tolerate even higher inflation.

It seems, however, that in the meantime they changed their minds. As a result, the June Fed meeting became a major event with dramatic impacts on financial markets.

Important dots

As absurd as it may sound to someone not following financial markets, the “shocking” element of the June Fed meeting that triggered a storm in markets was the repositioning of a few dots on a chart. A chart that Fed officials themselves say has practically no significance and is not a basis for their decisions.

This is the famous “dot plot chart”, a scatter plot that shows the current expectations of Fed officials regarding the future path of interest rates. Since these are the expectations of the people who set the current level of interest rates, it obviously cannot be considered entirely meaningless. At the same time, its importance should not be overstated. It reflects only the personal expectations of Fed officials several years ahead, and each of them stresses that the optimal level of interest rates cannot be forecast reliably that far into the future.

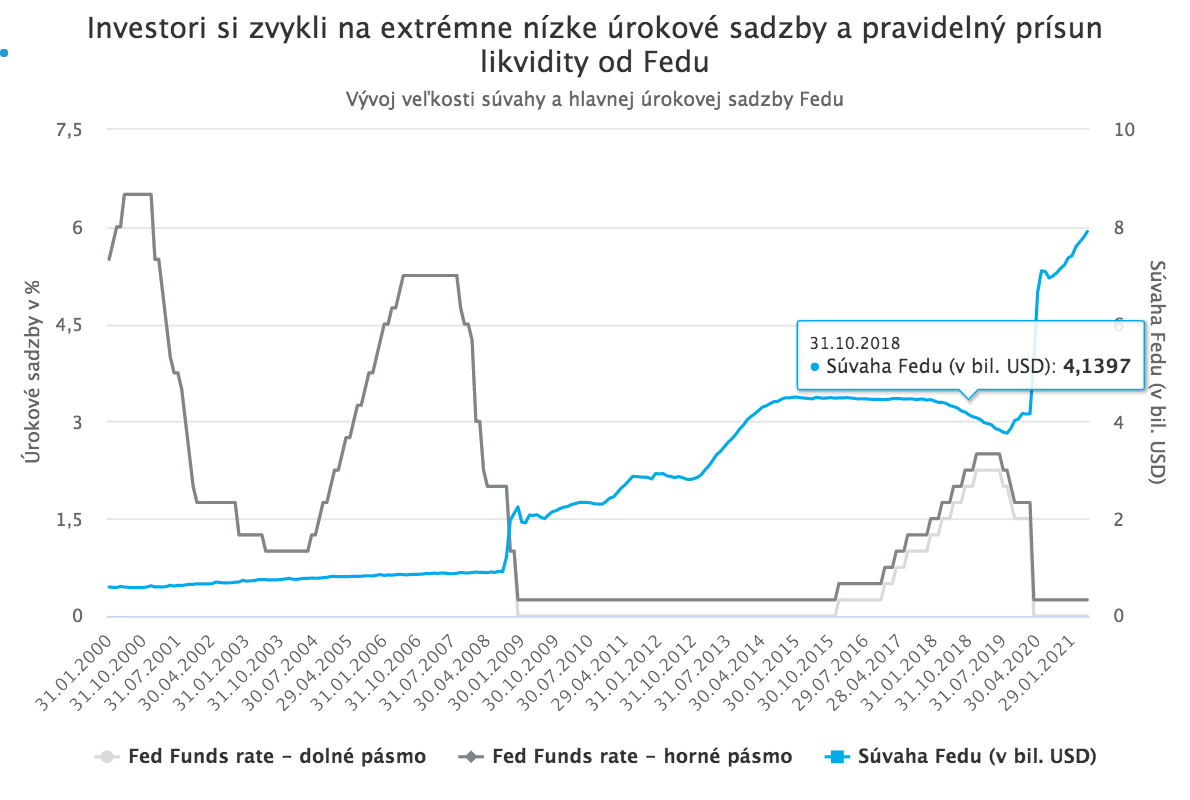

In any case, the updated dot plot showed that Fed officials expect rate hikes to begin earlier from the current record-low level than had originally been anticipated. The median projection points to a rise in rates “as early as” 2023, by 0.5%. Seven of the 18 members expect the first hike as early as next year. It also holds that before raising rates, the Fed would have to reduce its regular monthly asset purchases under quantitative easing, which currently amount to USD 120 billion per month.

Investors and analysts therefore interpreted the updated dot plot (combined with a slight increase in this year’s inflation projection and comments from some FOMC members) as a signal that the current rise in inflation surprised and even frightened the Fed, pushing it to consider tightening monetary policy sooner than it had originally planned and signaled to markets.

The Fed Got Spooked by Inflation

Such a dramatic shift in stance can be viewed as a serious communication mistake by the Fed. Up until the June meeting, its officials had emphasized that they considered the current rise in inflation merely a temporary phenomenon caused by base effects, the reopening of the economy, and temporary disruptions in supply chains, which would fade over time even without raising rates.

At the same time, they also reminded markets that tolerating a temporary rise in inflation in favor of recovery in the economy and labor market is consistent with the new policy known as FAIT (Flexible Average Inflation Targeting), which the Fed adopted last year.

As a result, in recent months investors favored assets and strategies that perform best in an environment of higher inflation and a rapidly growing economy (cyclical stocks, commodities, “bets” on a steeper yield curve, emerging-market currencies, etc.).

But as it turned out, in the end only two higher monthly inflation readings in a row were enough for the Fed to “flinch”. This was despite the fact that the April and May inflation data are indeed distorted by base effects and were significantly driven by temporary factors (especially the rise in used-car prices due to a temporary chip shortage), while the U.S. economy, and especially the labor market, are still far from a full recovery.

Markets Got Spooked by the Fed

Market reactions to this surprising pivot by the Fed were rather wild and volatile. The possibility of slowing asset purchases sometime over the course of next year and raising interest rates by 0.5% to levels that would still be historically extremely low in more than two years does not sound all that dramatic. However, investors accustomed to record-low rates and a constant stream of liquidity from the central bank amounting to USD 4 billion per day, and who in recent weeks had heavily “bet” on an environment of Fed-tolerated higher inflation amid rapid economic growth, found this prospect very unsettling.

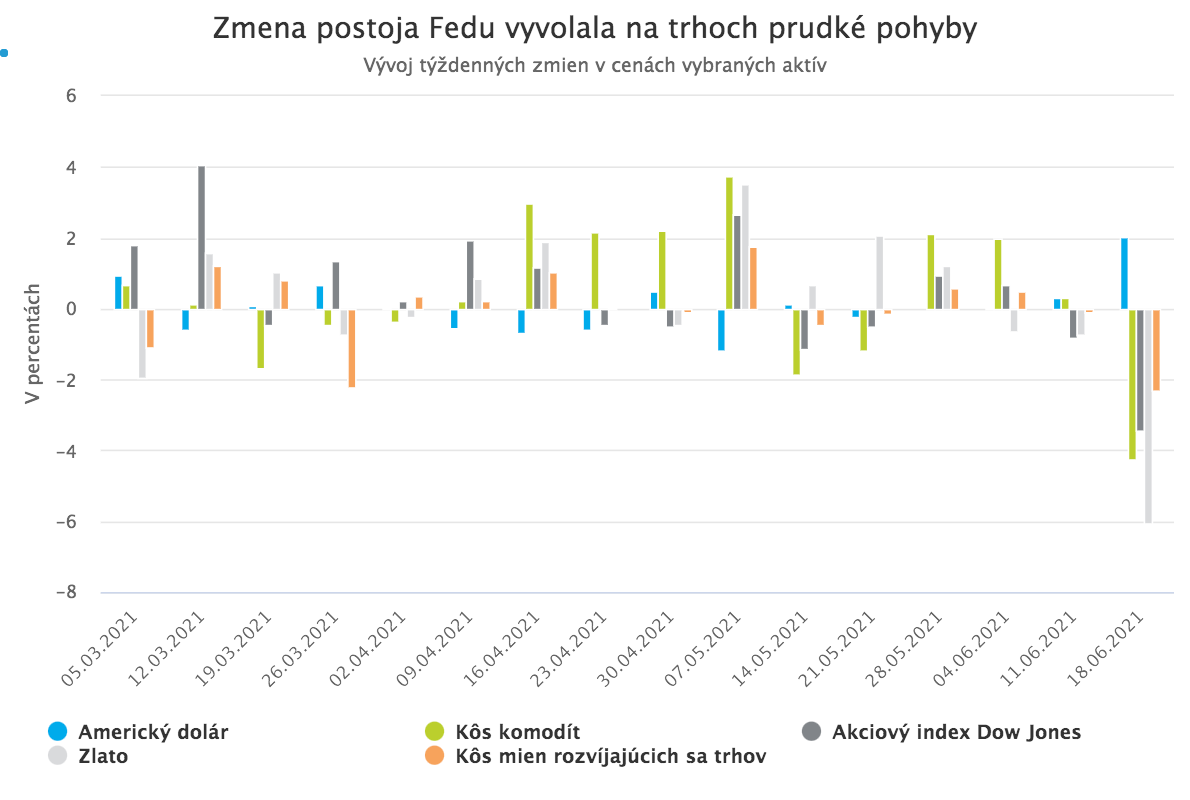

The market moves that followed were essentially the accelerated opposite of the moves that had been taking place over the past weeks and months. Investors simply began unwinding popular trades built for an environment of higher inflation.

That meant the sharpest strengthening of the dollar (and weakening of emerging-market currencies) since the start of the year, a decline in equities (especially cyclical stocks) and commodities, and a rise in real yields that pulled gold sharply lower.

The U.S. Treasury yield curve flattened due to what at first glance looked like a surprising drop in nominal yields at longer maturities. This move, however, was the result of unwinding “bets” on a steeper yield curve. The drop in longer-term nominal yields then negatively affected bank stocks. Volatility increased.

…and the Fed Got Spooked by the Market Reaction

The relationship between the Fed’s steps and market reactions is a complicated feedback loop, followed by subsequent corrections. One could say that market expectations largely determine the Fed’s room to maneuver. If Fed officials fail to steer investors’ expectations in the desired direction through long-term and gradual signaling ahead of a move (or the hint of a move), they risk a sharp market reaction. That reaction can then, for political as well as objective economic reasons, force them to correct their previous step or statement.

That is what happened this time as well. The sharp market reaction to the June meeting compelled the Fed to correct its earlier message, partly to fix a communication mistake and partly for objective economic reasons. A stronger dollar, falling equities, and rising real yields in anticipation of monetary tightening have an impact on the economy similar to actual tightening. In this case, however, the tightening is effectively brought forward by markets, when conditions are not yet appropriate, and it could endanger the economic recovery.

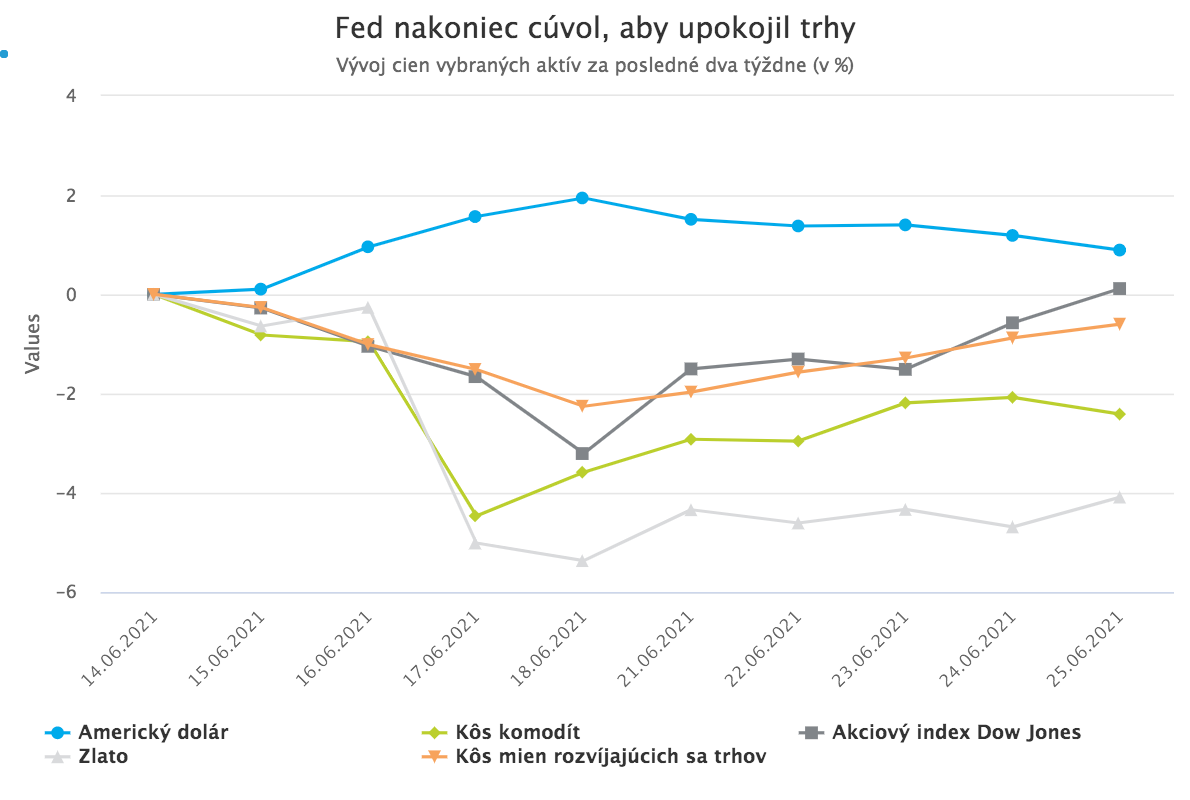

Fed Chair J. Powell and other FOMC members therefore used public appearances over the course of this week to adjust their earlier messaging and reassure markets that, despite the dots on the chart, rate hikes are not even being considered in the foreseeable future.

Markets calmed down, the dollar weakened, equities, commodities, and nominal bond yields rose. Real dollar yields fell, gold stabilized, and emerging-market currencies strengthened.