Is a New Commodity Supercycle Beginning?

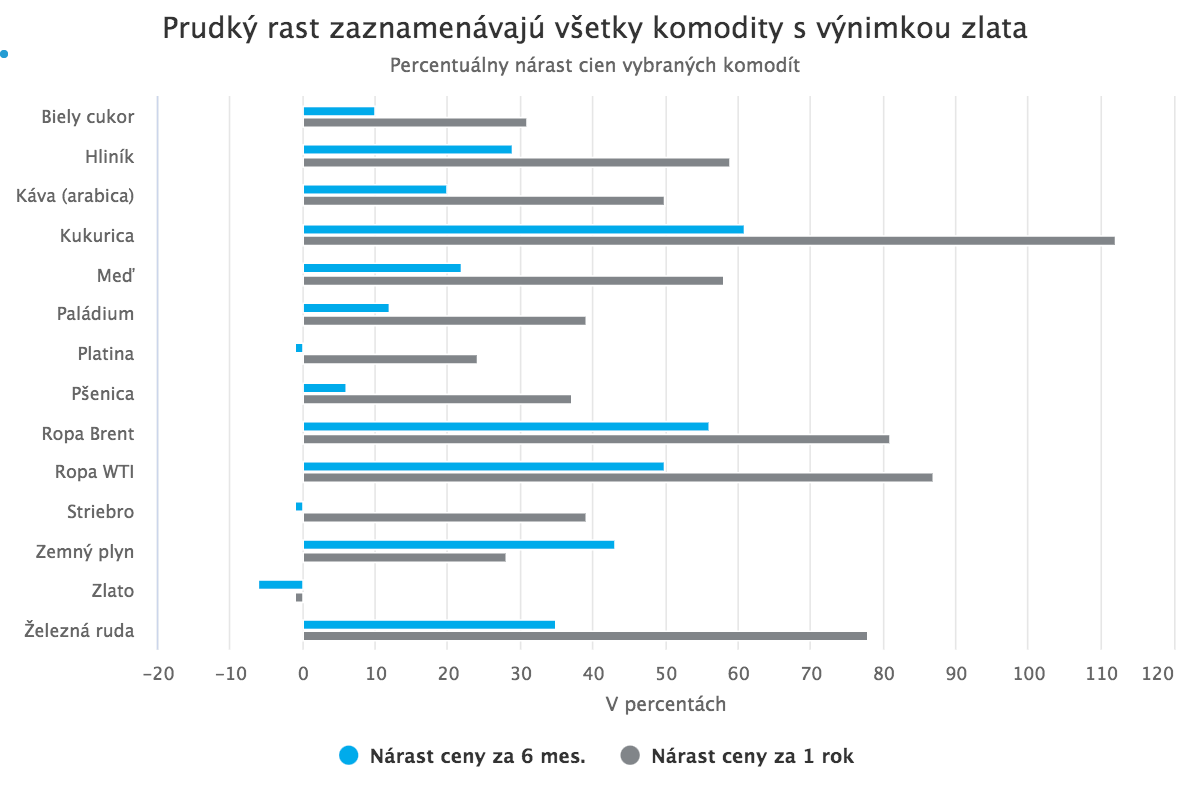

Prices of most commodities have been rising sharply since April last year. The S&P GSCI Index, which tracks the price performance of a basket of 23 of the world’s most heavily traded commodities, has increased by more than 60% over the past 12 months. Strong, double-digit and even triple-digit price growth has been recorded across nearly all commodity types, from oil through lumber and industrial metals to agricultural crops. The only interesting exception is gold. The price of this precious metal has not increased at all in recent months; on the contrary, it has declined slightly.

This sharp and broad-based rise in the prices of all types of commodities is attracting increasing attention from investors, analysts, and economists. Some are even talking about the start of a commodity supercycle. Are we truly on the threshold of a new supercycle, or is this only a short-term fluctuation?

Commodity supercycles

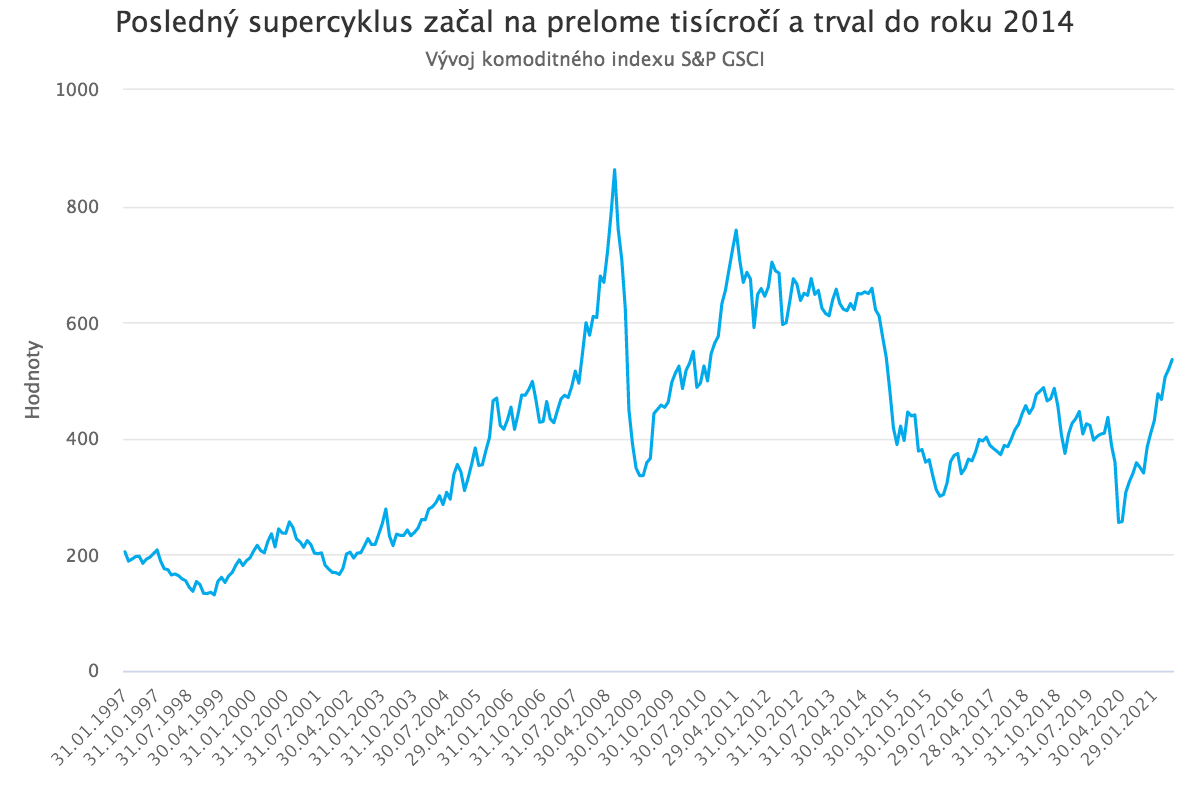

Commodity supercycles can be defined as multi-year, or even multi-decade, periods of simultaneous price increases across many types of commodities, driven by structural changes in the economy and society that create a long-term dominance of demand over supply. In modern history, four major commodity supercycles have occurred to date. The first began at the end of the 19th century and, with minor interruptions, lasted until the early 1930s. Its primary trigger was massive industrialization and urbanization in the United States; later, the outbreak of World War I significantly extended and strengthened it. Two further supercycles occurred in the 20th century due to mobilization ahead of World War II and the subsequent post-war reconstruction of Europe and Japan. The last, fourth supercycle was driven by the economic boom in China and some other emerging markets. It began around 2000 and, with one short but sharp interruption in the form of the global financial crisis, lasted until 2014.

At first glance, today’s strong increase in commodity prices has certain features in common with previous commodity supercycles. It began after a major historical event that caused profound structural changes in society and the economy, namely the outbreak of the pandemic, and it is characterized by a simultaneous rise in virtually all types of commodities. A closer look at its causes will further highlight some historical similarities, but it will also point to certain important differences.

What is driving commodity prices higher today?

The current rise in commodity prices is driven by an interesting combination of factors. Several of them can be considered short-term and transitory, while some have a longer-term, structural character. The “shutdown” of economies and many restrictions associated with the outbreak of the Covid-19 pandemic triggered a sharp decline in the prices of many commodities in March last year. When the economy stalled and people did not go out or travel, demand for industrial, energy, and various consumer commodities naturally dropped sharply. Oil was among the most affected commodities. As a result of the suspension of flights and production due to the pandemic, and a coincidentally ill-timed price war between Russia and Saudi Arabia, its price briefly fell into negative territory. When the global economy subsequently began to recover from the initial shock and measures were eased, commodity prices naturally moved upward. However, most did not stop at pre-crisis levels but continued rising to multi-year and even historic highs. This is therefore not only a recovery from previous declines.

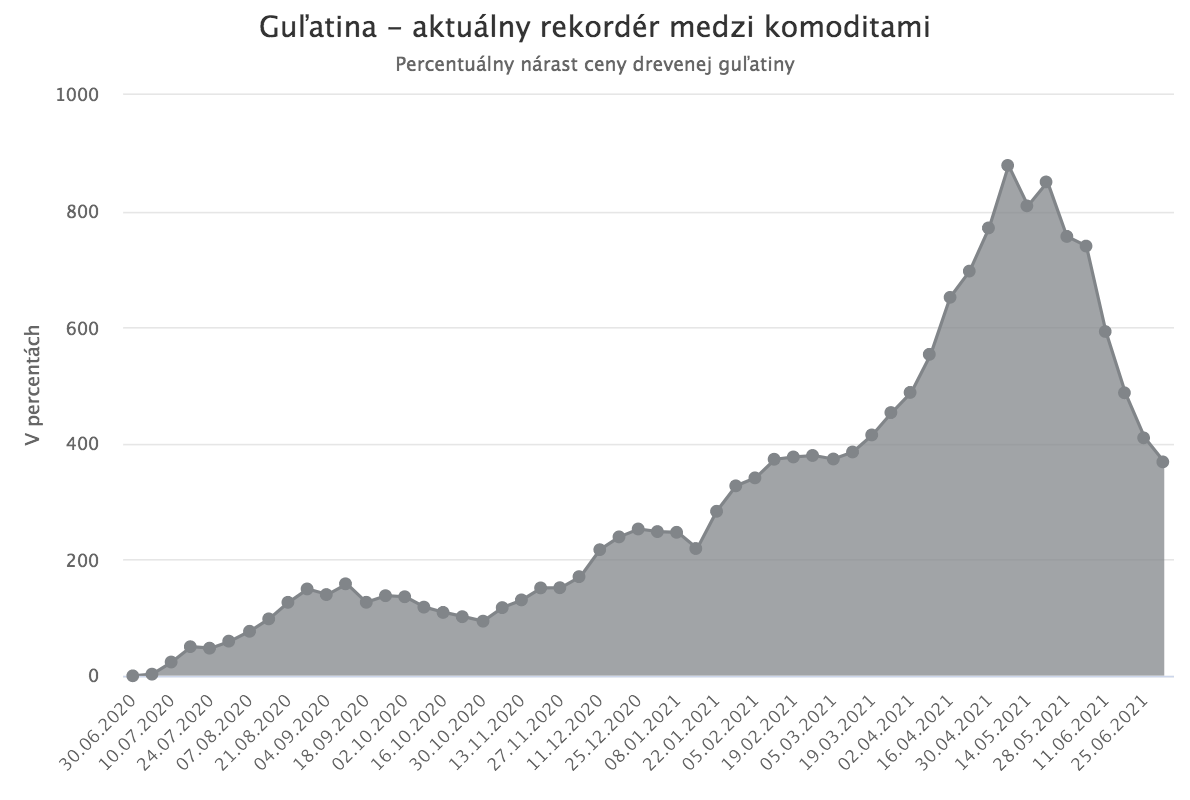

For some commodities, a temporary lag of supply behind demand plays a role, due to slowed production or extraction related to the pandemic and a rapid rise in demand after the reopening of the largest economies. Changes in consumer behavior triggered by the pandemic also generated unexpectedly strong demand for certain types of commodities, to which supply cannot adjust quickly. One example is lumber, which in recent months has been the fastest-rising commodity. The massive shift to working from home triggered a sharp increase in demand for houses, while demand for construction lumber also came from restaurants building terraces and from people who decided to use lockdowns to carry out various DIY projects in their gardens. Lumber production naturally could not adjust quickly to such a rapid increase in demand, so the price of logs surged sharply upward in the short term.

Price growth in some commodities is also supported by declines in supply due to factors unrelated to the pandemic, such as weather swings (for example, drought and subsequent frost in Brazil, which negatively affects coffee production and pushes its price higher) or artificial constraints (intentional production cuts adopted by the OPEC+ oil cartel to support higher oil prices).

Long-term factors

The supply-demand mismatch caused by pandemic-related production slowdowns and the simultaneous or subsequent rapid rise in demand can be considered only a temporary factor that will fade within a few months. However, commodity prices are also being pushed higher today by some longer-term drivers. These are mainly fiscal and monetary policy, and the long-term trend toward the green economy. Central banks and governments around the world responded to the outbreak of the pandemic with an unprecedented scale of monetary and fiscal stimulus. Central banks “poured” hundreds of billions into the economy through quantitative easing programs, while many governments introduced programs of massive public spending to support economic recovery. Both factors support higher commodity prices

In many countries, public spending aimed at supporting economic recovery has focused in particular on multi-year plans to build or renovate infrastructure, thereby increasing demand for construction and industrial commodities for years to come. At the same time, the flood of liquidity from central banks sharply boosts demand for all assets that are currently “in fashion.” Commodities are among them today, since the combination of massive stimulus from both governments and central banks is fueling inflation concerns, increasing demand for assets that traditionally serve as a good hedge against rising inflation, including commodities. The long-term trend toward sustainability and the so-called green economy simultaneously supports commodity prices in two ways: on the one hand, it increases demand for metals such as copper, lithium, and cobalt, which are used in electric vehicles and other green technologies; on the other hand, it leads to a significant decline in investment in the extraction and production of traditional energy sources and environmentally harmful metals that are still needed, reducing supply.

A fifth supercycle?

Today’s marked rise in commodity prices is thus the result of a combination of multiple factors. Many of them are transitory in nature and will fade within a few months; others are random and unpredictable; however, some, especially fiscal and monetary policy and the transition to the green economy, have a long-term, structural character and will likely continue to put upward pressure on prices of selected commodities for many years. Whether this is, or is not, the beginning of a new supercycle cannot yet be said with certainty. Supercycles can be identified accurately only in hindsight, after they have taken place. At that point, however, such a classification naturally has limited practical value and to some extent is also a matter of definition. What can be said today is that several commodities currently have excellent conditions for continued price growth and therefore represent an interesting investment opportunity. A good example is copper, which is used both in traditional industrial sectors and in so-called green technologies. As a result, it benefits simultaneously from the natural economic recovery after the pandemic, public spending on infrastructure renewal, and the transition to the green economy.

Investing in commodities has its specifics and pitfalls. Commodities are not suitable for direct purchase, and less experienced investors often do not fully understand the nature and characteristics of the various financial instruments through which they invest in commodities. The real performance of their investments can therefore often differ significantly from the expected performance, as well as from the actual performance of the underlying asset itself. At Sympatia, we will be happy to help you invest in commodities or other investment instruments that match your needs and objectives.