Rising bond yields are now also worrying central banks.

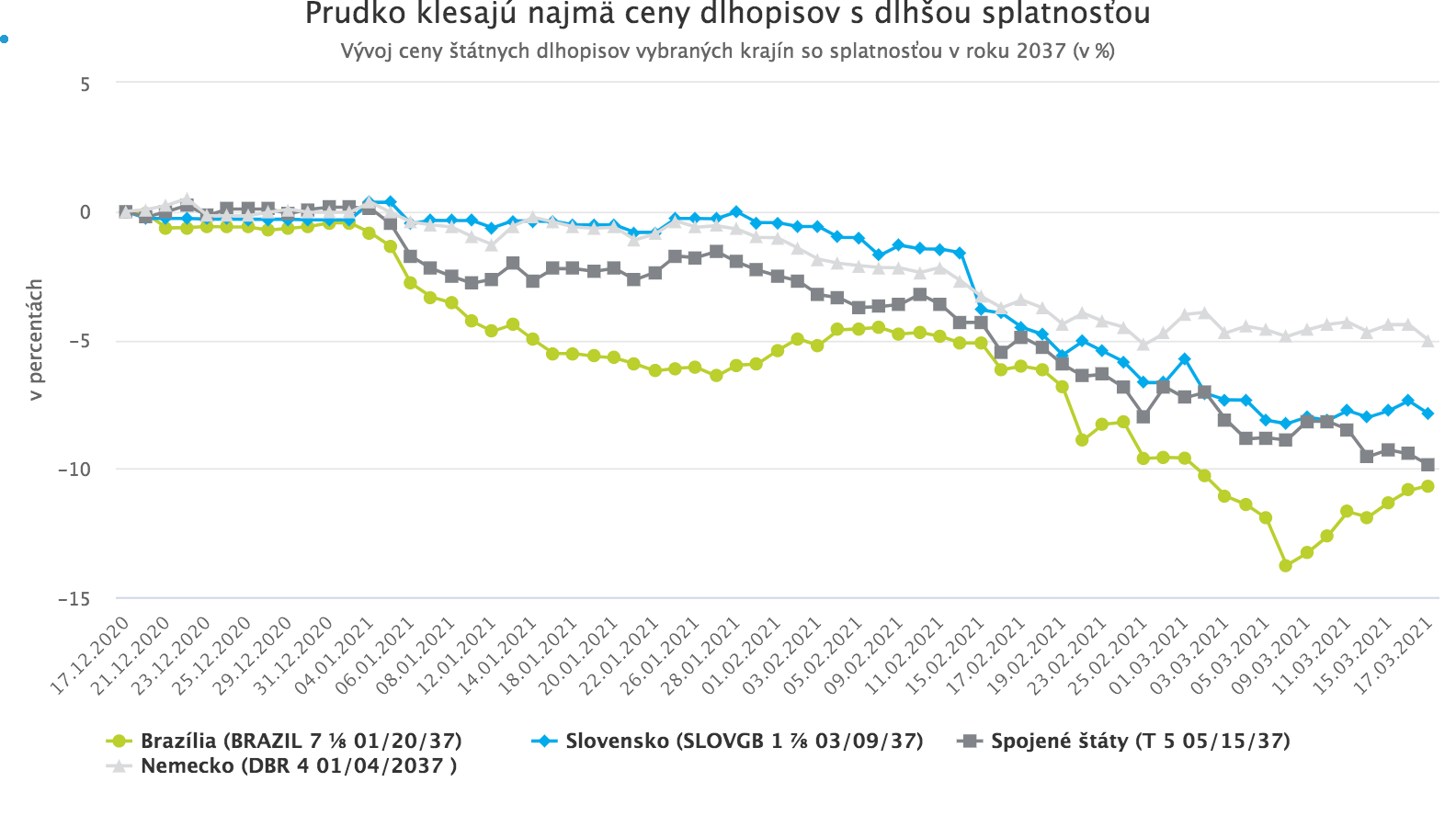

The emerging strong recovery of the global economy, combined with extremely loose monetary policy and a sharp increase in debt, is fueling market concerns about a (at least temporary) rise in inflation. These concerns are leading investors around the world to sell longer-maturity bonds, which are most exposed to the risks of rising inflation and potential interest rate hikes. The result is a rapid decline in their prices and a sharp rise in yields. This development is worrying not only investors but also an increasing number of central banks.

Rapidly rising bond yields can lead to an undesirable increase in interest costs for companies and entire countries at precisely the time when highly indebted economies are finally beginning to recover from the crisis. The ECB, as well as the Japanese and Australian central banks, therefore took steps during this month to slow the rise in yields in their domestic economies. The U.S. Fed, however, has so far, rather surprisingly, not taken such a step, even though the rise in bond yields is currently most dramatic in the United States.

Yield curve control

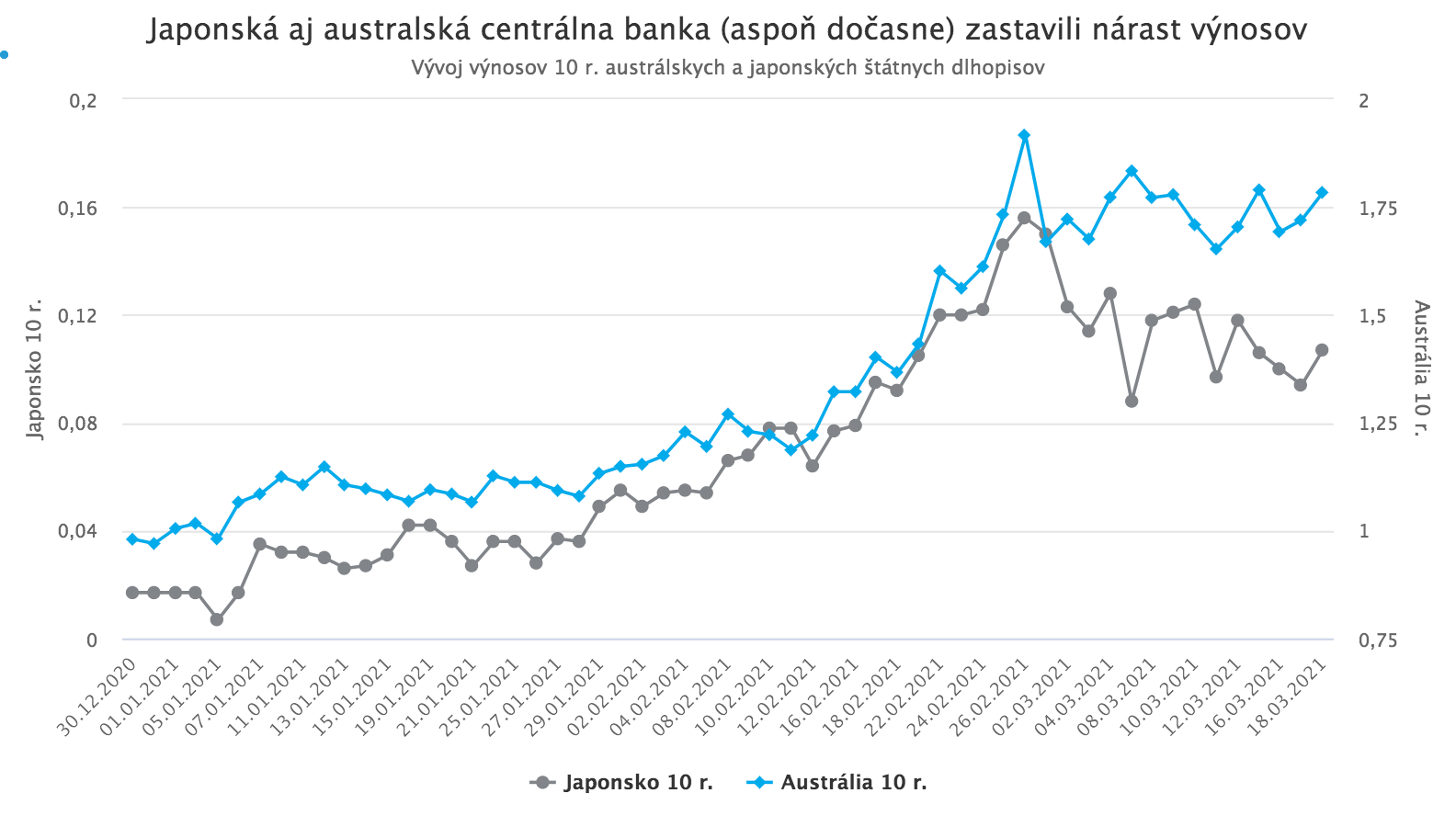

The Bank of Japan was the first of the most significant central banks to slow the rise in domestic bond yields this week. A verbal intervention was sufficient. Japanese government bond yields had been rising rapidly since the beginning of January. The reason was expectations that, for the reasons mentioned above, the central bank would widen the tolerated band for 10-year yields. Under its yield curve control policy, it currently seeks to keep 10-year yields at the target level of 0%, with an allowed fluctuation band of 0.2% up and down.

Over the past two months, in anticipation of a widening of this band from the usual 0.02%, 10-year Japanese bond yields rose to a two-year high of 0.15%. However, they did not break through the upper limit of the band. First, towards the end of the month, yields were pulled down by the usual month-end portfolio rebalancing from equities into bonds. Then, any hopes of further increases were dashed by the Governor of the Bank of Japan, H. Kuroda. At the bank’s meeting on 5 March, he simply stated that he does not currently consider widening the fluctuation band for 10-year bonds to be necessary. Yields fell immediately and did not come close to testing the upper limit of the band in the following days.

In a similar way, the Governor of the Reserve Bank of Australia, P. Lowe, intervened against the rise in domestic bond yields when, in a statement in early March, he quashed speculation that the bank might raise interest rates. Even before this statement, the Reserve Bank of Australia had unexpectedly doubled the volume of longer-maturity bonds it was purchasing. As a result, yields on 10-year Australian bonds stabilized around 1.75%.

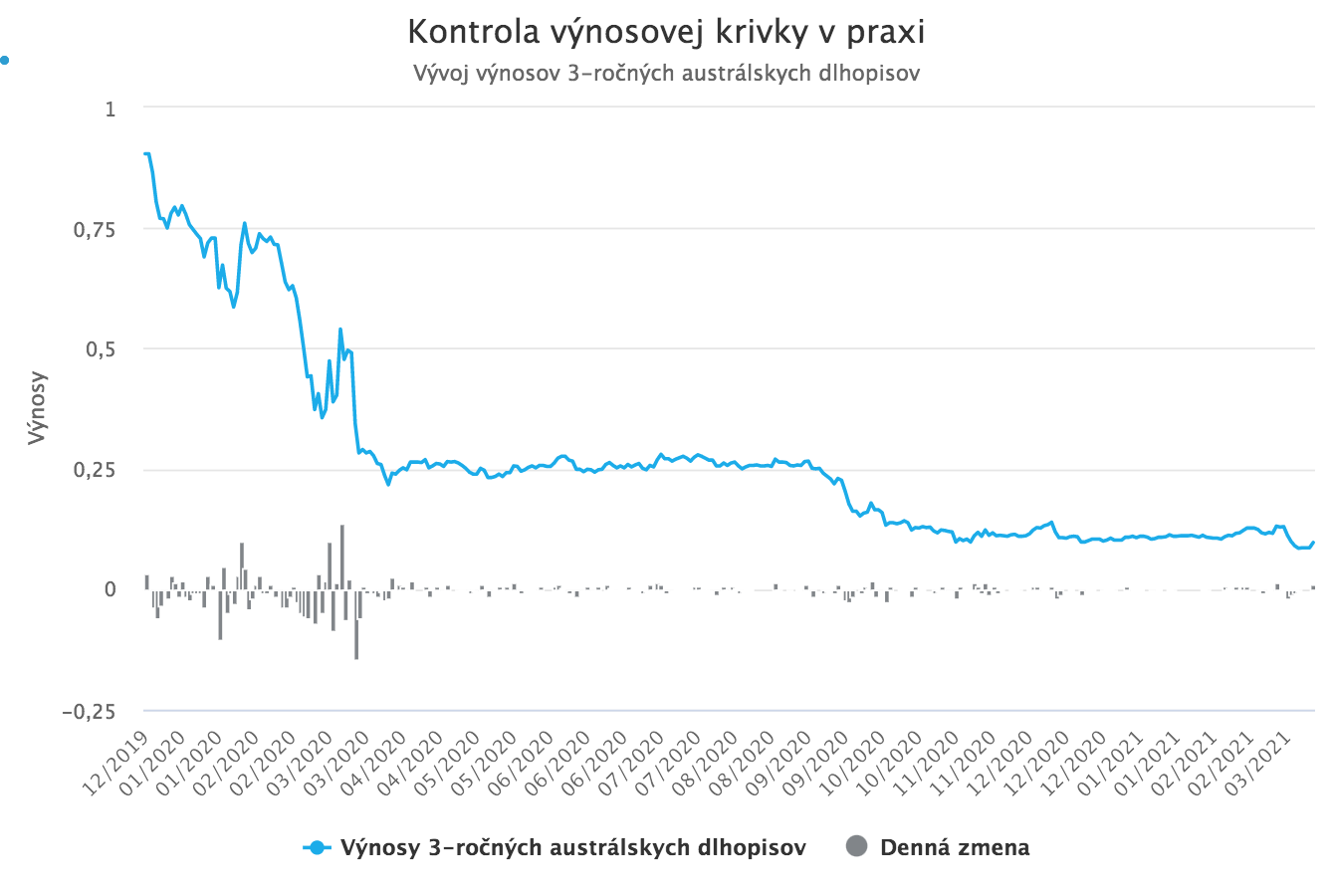

The Reserve Bank of Australia, like the Bank of Japan, uses a yield curve control policy. The RBA adopted this policy in March after the outbreak of the pandemic and primarily targets the yield on 3-year government bonds. Since November, the target level has been 0.1% (previously it was 0.25%). During February, investors also tested the bank’s determination to defend this level. As can be seen in the chart below, the bank managed to hold the line and 3-year bond yields are now back below the 0.1% threshold.

The ECB also intervened against rising yields

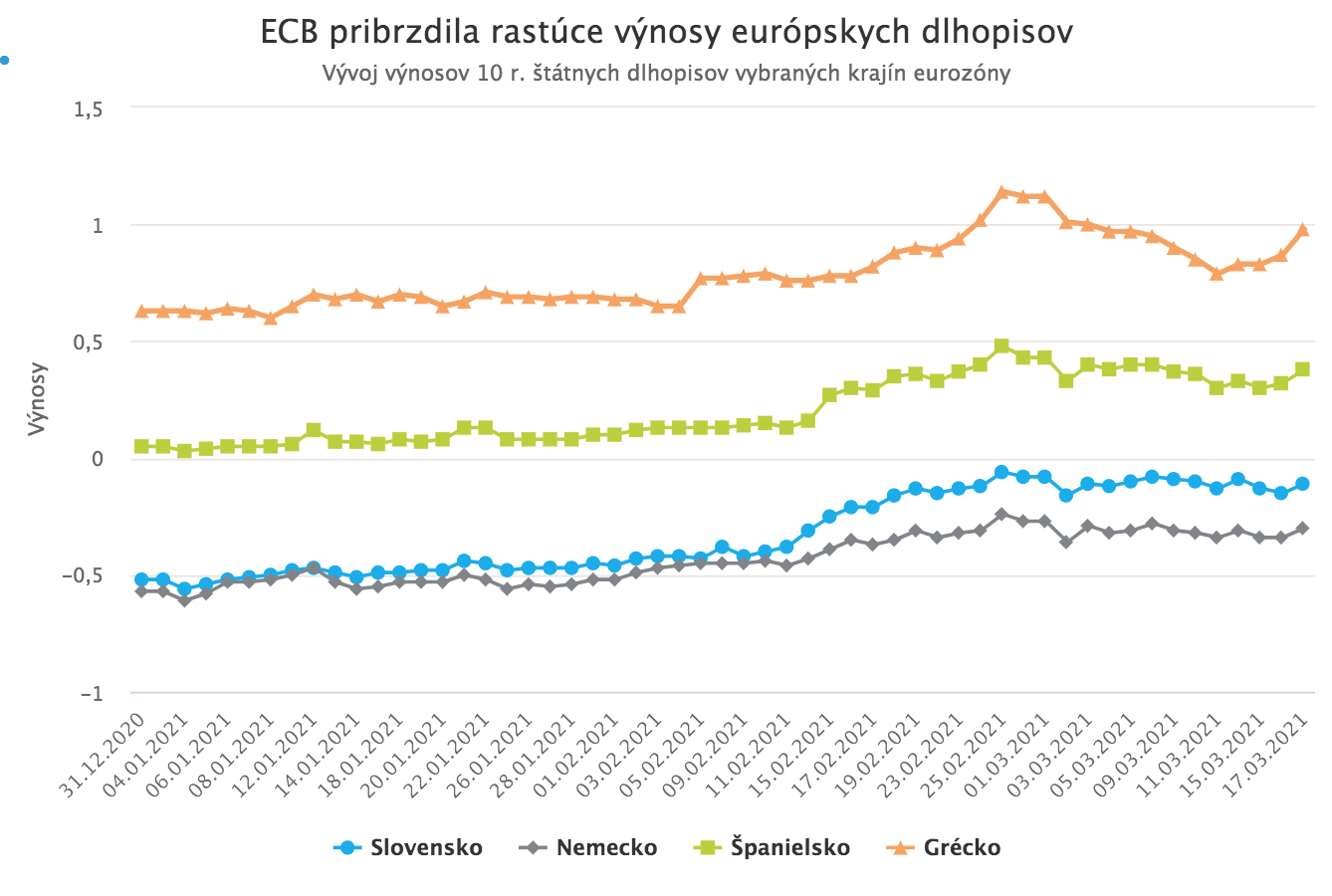

The ECB has also run out of patience with rising bond yields. No wonder. In many European economies, it is still too early to speak of the beginning of a recovery, and the pace of vaccination in Europe is significantly slower than in the United States and some other major economies. As a result, the ECB currently cannot afford any sharp rise in bond yields that could delay the recovery or even revive the specter of a debt crisis in the heavily indebted “periphery” countries.

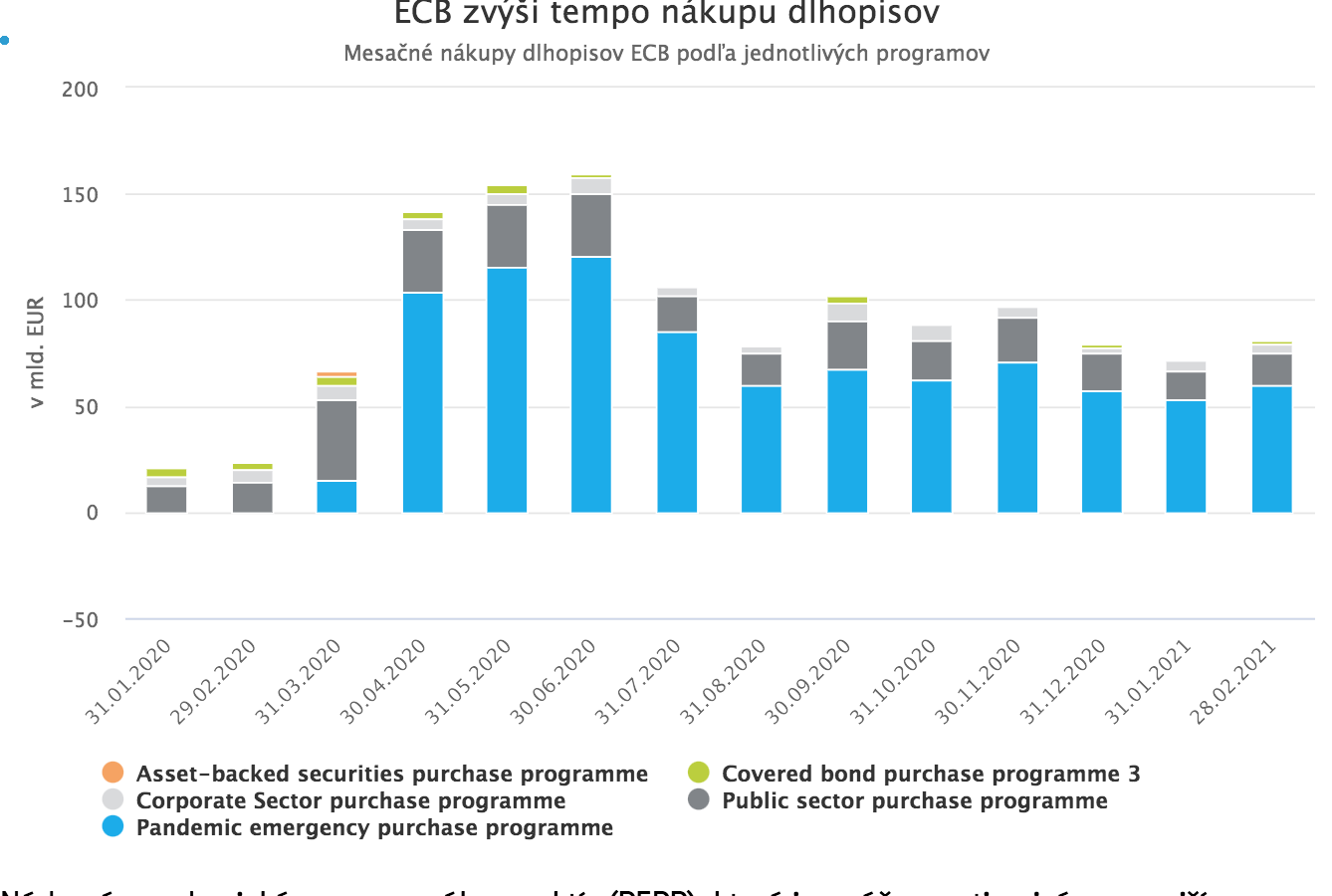

Christine Lagarde left nothing to chance. At the bank’s March meeting, she announced that, in view of current market conditions and the inflation outlook, the ECB will significantly increase the volume of monthly bond purchases under the PEPP program over the next quarter. Purchases will be conducted flexibly, taking into account prevailing market conditions, with the aim of preventing an excessively sharp rise in borrowing costs.

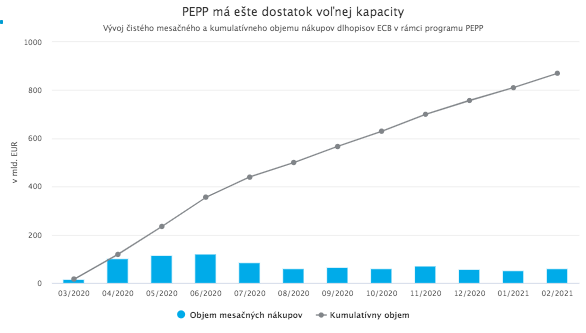

The Pandemic Emergency Purchase Programme (PEPP), which is currently the most important and largest bond-buying program by volume, is well suited for this purpose thanks to its flexible design and large capacity. After it was increased in December last year, its total envelope stands at EUR 1.85 trillion. At present, it still has almost EUR 1 trillion of unused capacity for bond purchases. This “firepower” is undoubtedly sufficient to bring the bond market “into line.”

It can be expected that the ECB will allow some increase in European bond yields; however, the PEPP will ensure that the rise is not too abrupt and that spreads between “core” and “periphery” bonds do not widen.

Large moves in the US yield curve

The only major central bank that has so far not intervened in any way against rising bond yields is the US Fed. It is precisely in the United States where the increase in yields has been the most dramatic. Thanks to rapid vaccination and enormous stimulus, the US economy has already set out on a path of rapid recovery from the pandemic crisis. The continued sharp rise in debt (the United States currently needs only four days to issue bonds in an amount equal to Portuguese or New Zealand GDP), together with massive fiscal stimulus (the recently approved Biden USD 1.9 trillion stimulus package and the planned more than USD 2 trillion infrastructure renewal package), will push inflation higher in a rapidly recovering economy.

When we add to these variables the Fed’s new policy on interest rates and inflation, whose essence is to tolerate a temporary rise in inflation above the 2% target without immediately raising rates, we get an “explosive” mix of factors that could indeed send inflation rapidly higher. Such a rapid increase in inflation could subsequently force the Fed to raise rates sooner than originally expected.

Of course, by a rapid increase in inflation we do not mean any catastrophic Venezuela-style inflation. The assumption is only a temporary increase slightly above the 2% target, which after a few months will prompt the Fed to raise rates and bring inflation back below 2%. However, that is of course enough to trigger a sell-off in longer-maturity, high-duration bonds. For most of last year, investors expected that the Fed would begin raising rates no earlier than 2024, and that inflation would not reach 2% anytime soon.

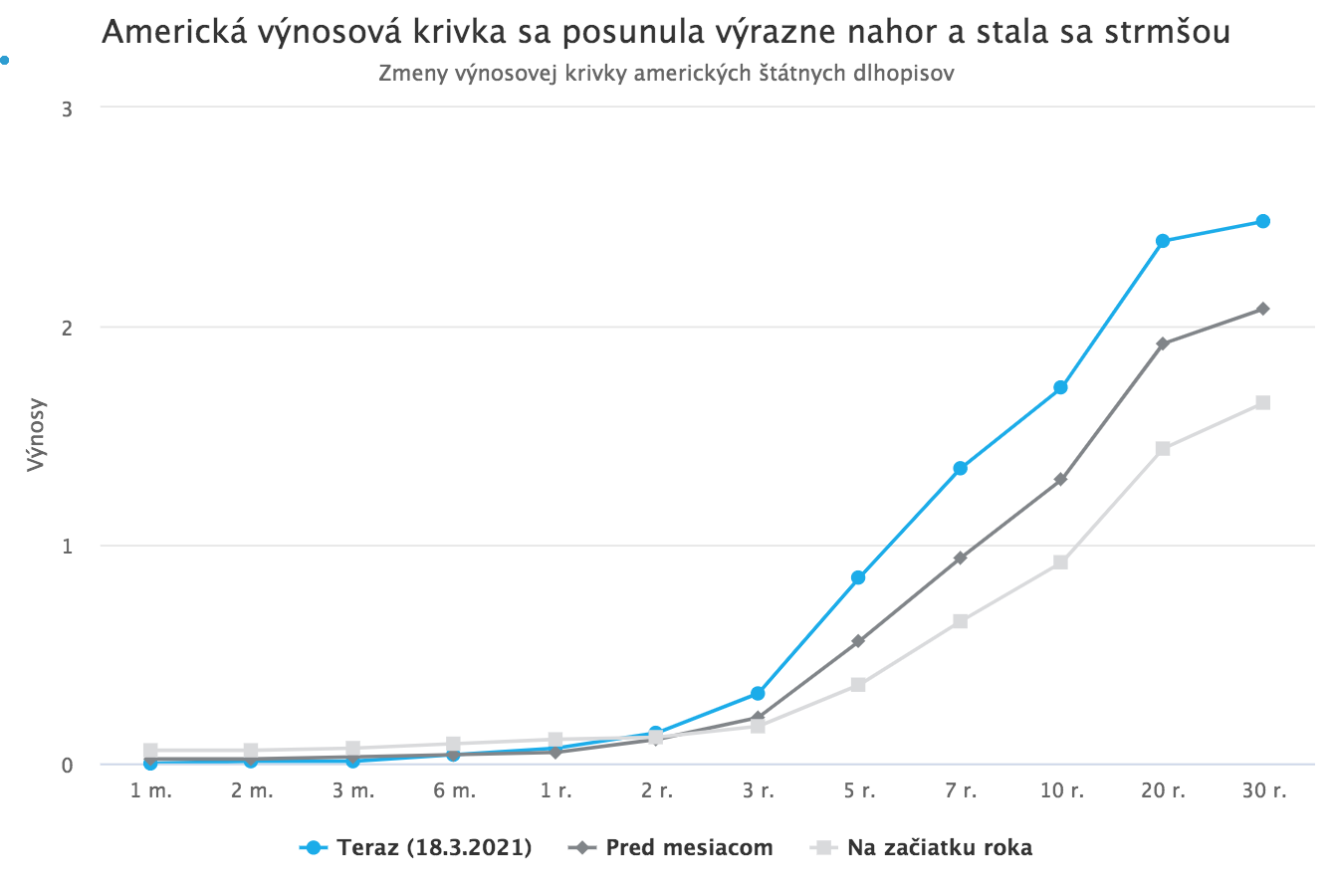

Over the past two months, the US Treasury yield curve has therefore experienced significant moves. Yields have risen sharply and the entire curve has become steeper, as yields on longer-maturity bonds increased the most. Bonds with maturities of 10 years and more have even returned, in terms of yield levels, to where they were before the pandemic broke out.

The Fed has not intervened yet

This development is causing considerable concern among investors. Rising yields naturally mean falling prices for the bonds in question. US Treasuries are held in some amount in the portfolios of almost every investor, as they have traditionally been regarded as a safe and stabilizing component. Under current conditions, however, they are generating losses and are a source of unwanted volatility.

At the same time, rising yields are putting pressure on several important segments of the equity market that, by contrast, benefited from an environment of slow economic growth, record-low rates, and long-term declining inflation, most notably shares of large technology companies.

Rapidly rising US bond yields are also undesirable from the perspective of other countries, especially emerging markets. They push up these countries’ borrowing costs as well, because they reduce the interest-rate differential between their riskier securities and US Treasuries, which are considered the safest. The additional yield offered by emerging-market bonds thus decreases as US yields rise, making these securities less attractive to investors.

Rising US yields also lead to a stronger dollar, with a traditionally negative effect on emerging-market economies and currencies.

However, the Fed is clearly not concerned about this development so far. Unlike other central banks, it has not attempted in any way to stop rising yields, not even through verbal intervention. Although J. Powell emphasized at the March meeting that raising rates is not planned in the foreseeable future, he did not express a willingness to act against rising yields, and he did not even indicate that this development was causing any concern.

The rapidly accelerating US economy can simply afford some increase in borrowing costs at the moment. Given the current sharp pace of the rise in long-term yields, however, it is almost certain that the Fed will have to step in soon, whether due to concerns about the negative impact of higher borrowing costs on the domestic economy or due to pressure from investors.

Until that happens, bank stocks and other financial companies remain in favor, as they benefit the most from rising yields. We assume that the Fed will intervene when 10-year yields approach 2%. They are currently less than 30 basis points away from that level.