Robinhood vs. Wall Street: The dawn of a new era of investing, or the final phase of the bubble?

While previous market sell-offs typically led to an outflow of retail investors from financial markets due to fear of further losses, this time it has been exactly the opposite. The sharp market declines at the beginning of the coronavirus pandemic attracted a record number of retail investors to the markets. The Robinhood app, today the most popular trading platform aimed at young retail investors and a synonym for retail investing, opened as many as three million new accounts since the beginning of the year, with most of them added after the outbreak of the pandemic and the March market sell-offs. Other trading platforms popular among small individual investors saw similar trends.

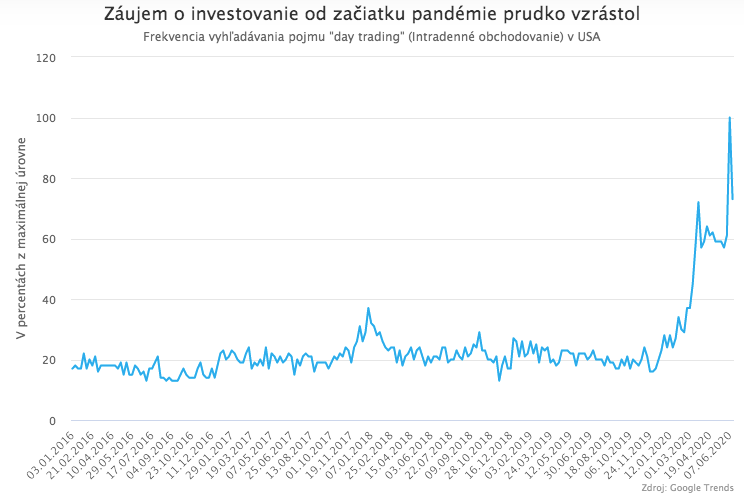

This sharp rise in retail investors’ interest in trading in financial markets is the result of an interesting interplay of several factors. The pandemic struck at a time when a price war was underway among US brokers, accompanied by aggressive advertising that was making investing increasingly accessible and appealing. At the same time, quarantine measures meant that people suddenly had more free time, and those who enjoy sports betting and casino gambling began looking for substitutes for their favorite pastimes, since sporting events were canceled and casinos were closed. “Betting” in financial markets became a natural choice for them. The huge increase in interest in investing since the start of the pandemic is also well illustrated by Google Trends data. Searches for terms such as “day trading” (intra-day trading) saw a rocket-like increase.

While retail investors’ interest in financial markets has surged since the outbreak of the pandemic, large investors have, at the same time, been pulling back from the markets due to enormous uncertainty about the economic impact of the coronavirus. As a result, retail investors now hold a record amount of stocks and options, while institutional investors hold a record amount of uninvested cash.

“I’m a better investor than Buffett!”

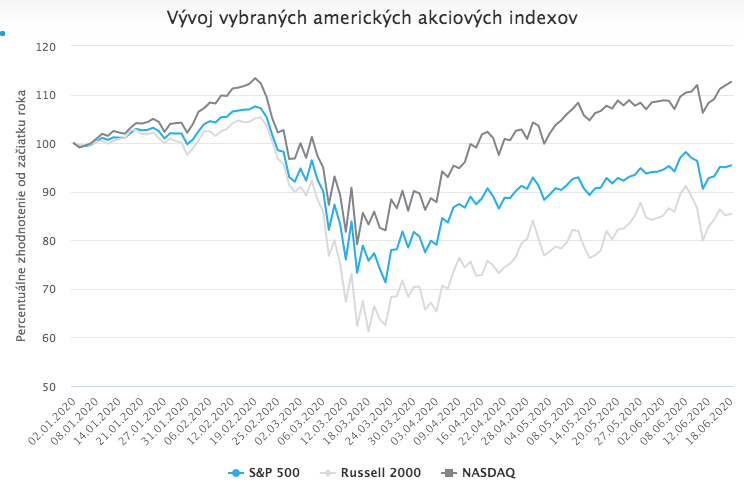

Looking at equity market performance over the past months, especially in the United States, it is clear that retail investors who began investing heavily right after the March sell-off have, since the outbreak of the pandemic, achieved better performance than many large institutional investors, who kept a large share of their assets uninvested and therefore missed a significant part of the sharp rally in April and May.

Indeed, investment legends are now admitting one after another that they misread the situation and missed a large part of the rally. The legendary investor Stanley Druckenmiller admitted that while the S&P 500 rose by 40% from its March low, his portfolio gained only 3%. Airline stocks climbed to almost double just a few weeks after Warren Buffett sold them. Paul Tudor Jones said that current market developments have made him very humble. For the past three months, Howard Marks has explained in each of his famous memos that he does not really know what to do and does not understand the current market environment.

At the same time, many young investors who have been trading for only a few weeks have posted high gains, filling them with euphoria and investing self-confidence. A textbook example of this new generation of investors is Dave Portnoy, who previously focused on sports betting and blogging. After the outbreak of the pandemic, he switched to day trading, which he streams. In his videos he now claims that “day trading is the easiest thing in the world” and that he himself is “better than Warren Buffett.”

Excessive euphoria is not a good sign

For experienced investors, developments like this set off every alarm bell. Instead of the dawn of a new era of investing, in which people like Dave Portnoy become the new “Buffetts” while the real Buffett fades into obscurity, they see the final, manic phase of a market bubble. Of course, seasoned investors’ warnings about a bubble may be motivated at least partly by bitterness that they themselves did not profit from the sharp rally of recent weeks.

Still, the current situation in many ways resembles the eve of the dot-com bubble bursting, when everyone was convinced there was no simpler and more reliable way to get rich quickly than to buy shares of any technology company that had at least some distant connection to the internet. The peak of the US housing bubble was accompanied by a similar mindset, embodied above all in the pervasive belief that real estate prices, like stock prices today, could only rise, and therefore everyone should invest in them, the more the better.

From the perspective of what happens next, however, there is one advantage: even if the sharp rise of recent weeks really is a bubble, large investors waiting for a good opportunity will use its bursting to invest a record amount of idle cash, so it should not take long for stocks to return to their previous levels.

Causality, or just good timing?

An interesting question is whether retail investors simply timed their entry into the market well (whether by skill or luck) at the March bottom, or whether their own trades directly caused the subsequent sharp rally. We do not yet know the answer with certainty. Trades by retail “Robinhood” investors account for only about 1% of total daily trading volume in equity markets, so one can convincingly argue that their trades are too small to move the entire market.

On the other hand, a large share of daily trading is now driven by algorithmic and trend-following strategies, which, together with the FOMO effect, can easily amplify an initial upward impulse. In addition, retail investors are increasingly active in the options market, and through this channel they also influence the prices of the underlying stocks.

Betting psychology in the investing world

While for the most heavily traded stocks with large daily volumes we still cannot say for sure whether the recent moves are the result of retail activity or not, for some corners of the equity market there is little room for doubt. It seems that the basic investment strategy of the new generation of retail investors is to buy stocks whose price has just fallen sharply and hope they return to their previous levels, regardless of whether there is any rational reason for such a rebound. In essence, this is the transfer of betting psychology into the investing world. If luck is on their side, it can lead to fast and substantial gains; if not, the invested amount collapses.

So today, retail investors’ favorite investments include airline stocks, casinos, small-cap companies with low market capitalization, and even bankrupt firms. In other words, stocks that have just fallen sharply. Since large investors would not touch such stocks even with rubber gloves, their daily trading volume is low and their price moves are, to a large extent, the result of retail investors’ activity. And it is precisely in these corners of the market dominated by retail investors that many bizarre, rationally inexplicable moves are taking place today.

Bizarre moves in the Robinhood wonderland

The recent rise in airline and casino stocks, driven by retail investors, can at least be supported by the expectation that the pandemic will fade quickly and that the revenues of these otherwise viable companies will surge again. Although, of course, the irony of investing in casino stocks as a forced substitute for gambling in a casino because casinos are closed should not be lost on anyone.

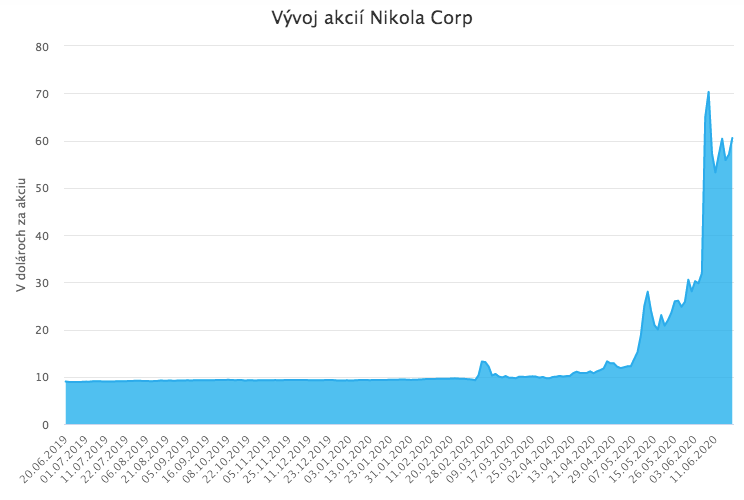

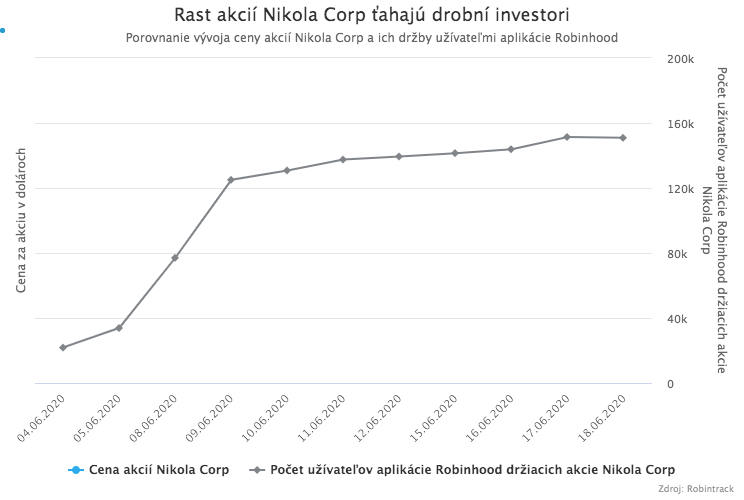

However, the investment enthusiasm of the new generation of investors is also benefiting companies that have never been operational, and it is highly questionable whether they ever will be. For example, shares of Nikola, a company that aims to compete with Tesla, have risen so sharply in recent days that the firm has surpassed Ford in market capitalization. This is despite the fact that it has not sold a single car yet, has no revenues, and does not expect any profits in the foreseeable future. The chart below makes it clear that purchases by Robinhood investors played a major role in its rise.

In recent weeks, it has also happened that the shares of some small company suddenly surge without any obvious reason and then fall back again. The cause usually turns out to be that inexperienced investors simply confused it with another company. For example, shares of Zoom Technologies, which has nothing in common with the communications platform Zoom other than a similar name, rose much more sharply in the first days of the pandemic than the shares of the “real” Zoom, that is, Zoom Video Communications. Within a few days they rose sevenfold. Trading in these otherwise almost worthless shares ultimately had to be temporarily halted by the US regulator, the SEC, citing “investor confusion.”

A few days ago, shares of the small Chinese company FANGDD Network Group suddenly jumped as well. It turned out that some beginner investors had confused it with the group of the largest US technology stocks known under the acronym FANG (Facebook, Amazon, Netflix, Google).

Ad absurdum

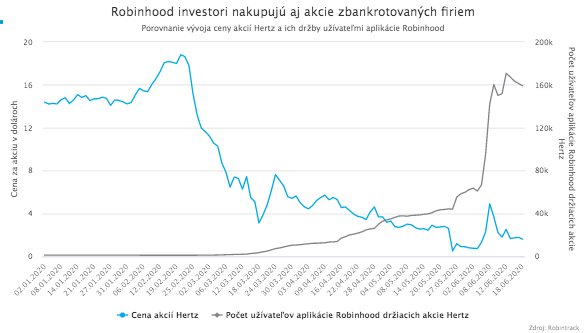

The peak of bizarreness (at least so far unmatched) among beginner retail investors, however, has been the buying of shares of freshly bankrupt companies. Shares of companies such as Hertz, JCPenney, Whiting Petroleum, and others often posted gains of more than 100% even though they had just declared bankruptcy. They were pushed higher by inexplicable purchases by Robinhood investors, who evidently, in this case too, stuck to their favorite investing thesis that stocks that have fallen sharply should rebound, even though the very reason for the drop was the bankruptcy itself.

The bankrupt US company Hertz even decided to use this bizarre mania to its advantage. Seeing that retail investors were buying its shares even after it declared bankruptcy on May 22, it announced a plan to raise capital by issuing new shares worth USD 500 million. This would have been the first case in history of a company in bankruptcy issuing new equity. Of course, this is a complete absurdity, tantamount to legally robbing naive investors.

Hertz does not have enough money today even to repay its bank loans and pay off its bonds, which now trade at 40% of their face value, that being their estimated recovery value. This means that any money raised through selling shares would, by court decision, simply be allocated to the banks and bondholders. The US regulator halted Hertz’s plan, at least temporarily.

Short-term speculation is not a good long-term investment strategy

In conclusion, it should be said that although many speculative trades by small investors, including those described above, may look bizarre, make no economic sense, and may signal the final phase of a bubble, the profits from them are no less real than the profits from trades by experienced investors supported by detailed analysis. The key to success in this type of trading, however, is to close open positions in time and actually realize paper gains. In other words, to pass the “hot potato” to someone else before it becomes clear that it has a real value far lower than the price at which it is currently trading, or that it is even completely worthless.

It is also very important not to confuse this kind of activity, which can bring fun, adrenaline, and the possibility of large gains and losses, with long-term wealth building, where the priority is investment safety and stable, long-term growth.