Rising US bond yields have spooked equity markets.

The expected economic recovery and ongoing stimulus are pushing stocks higher, but at the same time they are unfavorable for bonds. The global equity index MSCI World ended its longest “winning streak” in 17 years this week. It rose for 11 consecutive days.

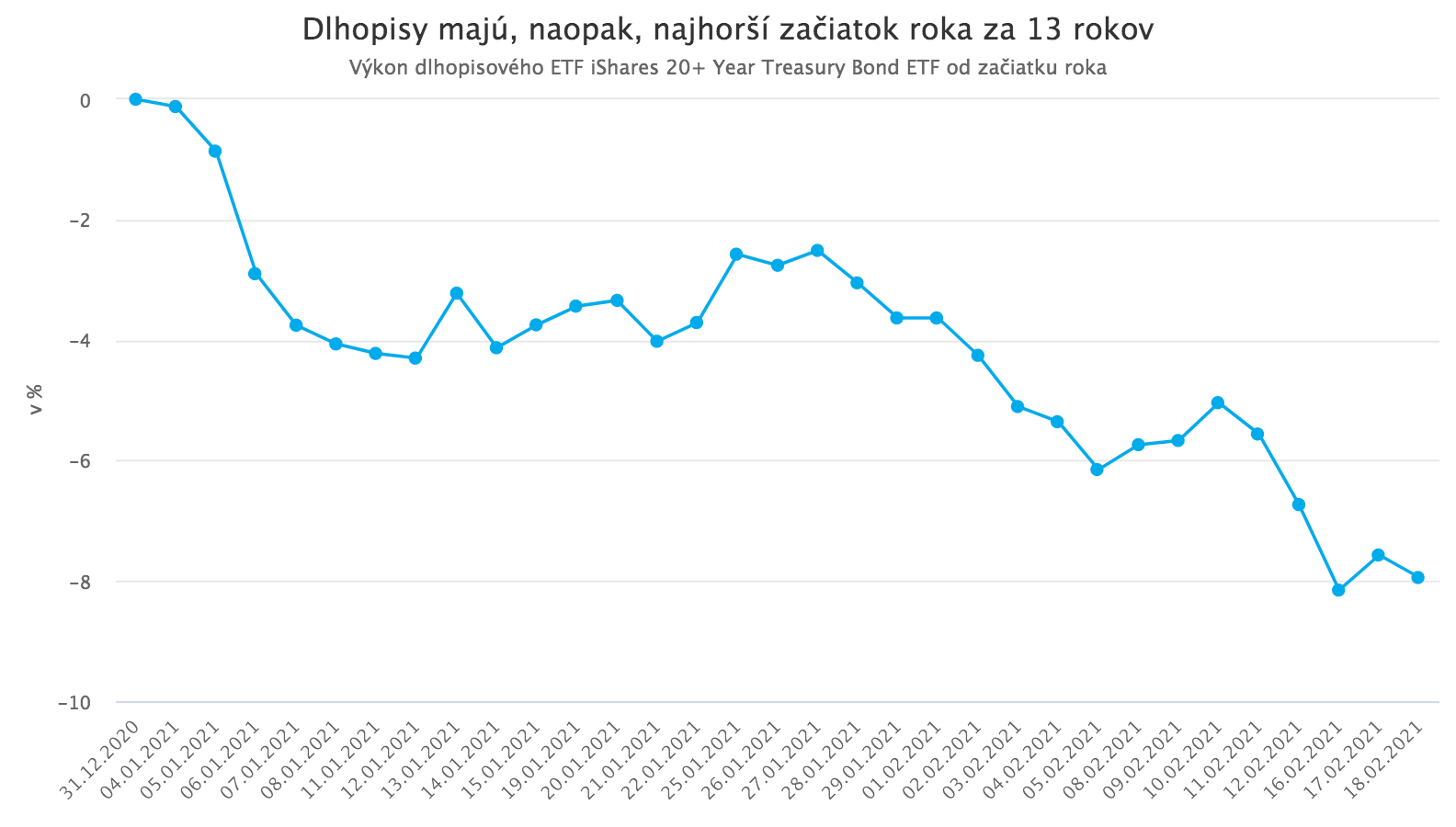

US bonds are also having their worst start to the year in 13 years. The expected acceleration of economic growth after the pandemic is brought under control, together with the USD 1.9 trillion economic relief plan promoted by J. Biden, is driving up inflation expectations and triggering a sell-off in safe US Treasuries.

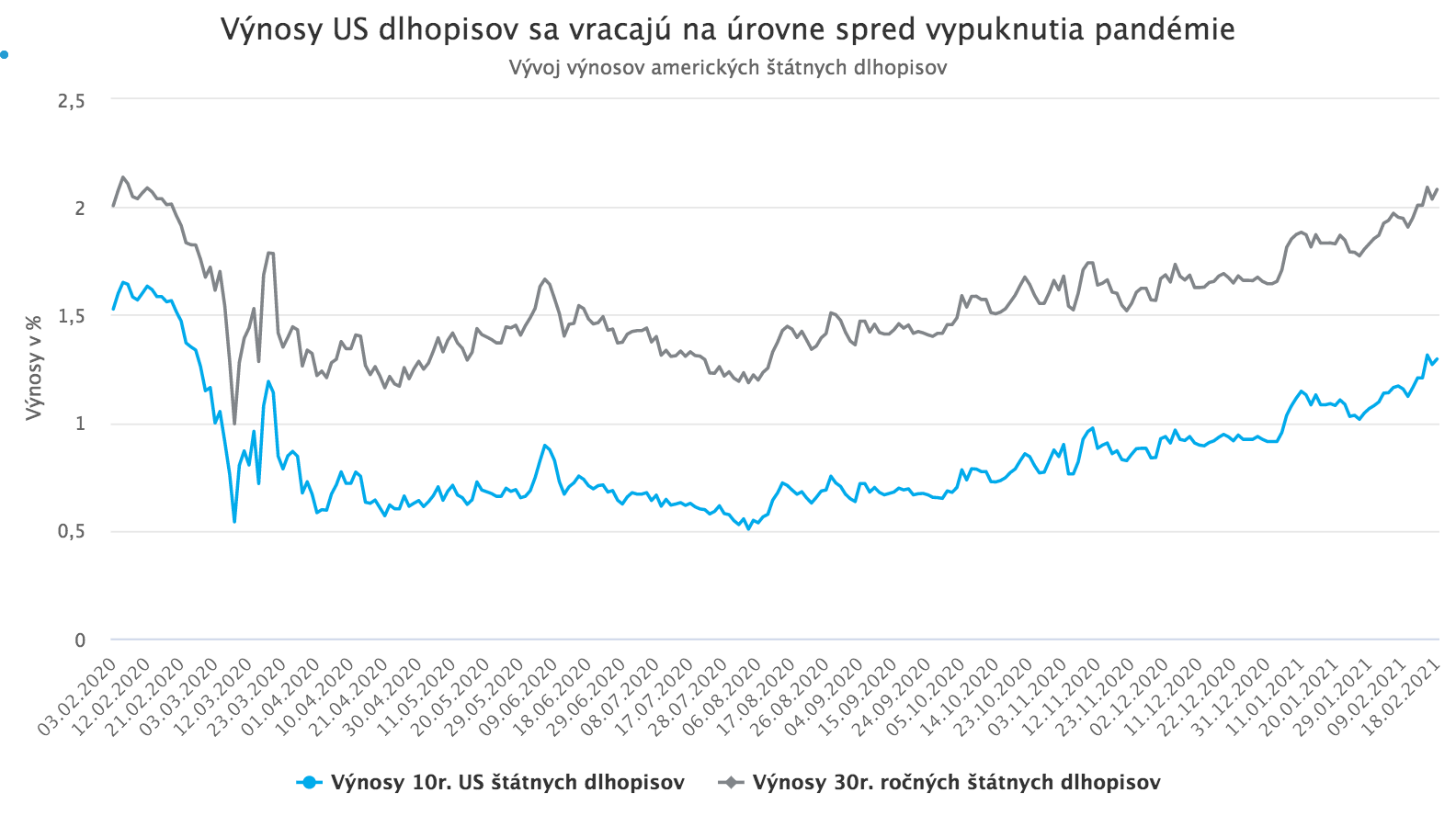

Their yields have been rising steadily as a result of this dynamic. In the case of longer-maturity bonds, we have even seen yields climb back to pre-pandemic levels, and the closely watched yields on 10-year bonds rose this week to their highest level since February of last year.

And it was precisely this sharp rise in bond yields over the course of the week that brought an exceptionally long rally in equity markets to an end.

The complicated relationship between the bond and equity markets

The relationship between bond yields and equity market performance is complex and has many dimensions. On the one hand, rising bond yields should theoretically put downward pressure on stocks, because for companies they mean higher interest expenses and they also mechanically reduce equity valuations, since higher yields imply a higher discount rate applied to future cash flows, which lowers their present value. Rising yields can also, in theory, lead investors to shift money from equities into safer bonds, which become more attractive as yields rise.

On the other hand, if the rise in yields is driven by positive macroeconomic expectations, those expectations simultaneously improve the attractiveness of equities as well, because they increase the size of expected future cash flows. Historical data indeed show that when both equity markets and bond yields are driven by positive underlying factors, both can rise at the same time, and there is no specific level of bond yields that would automatically cause stocks to fall.

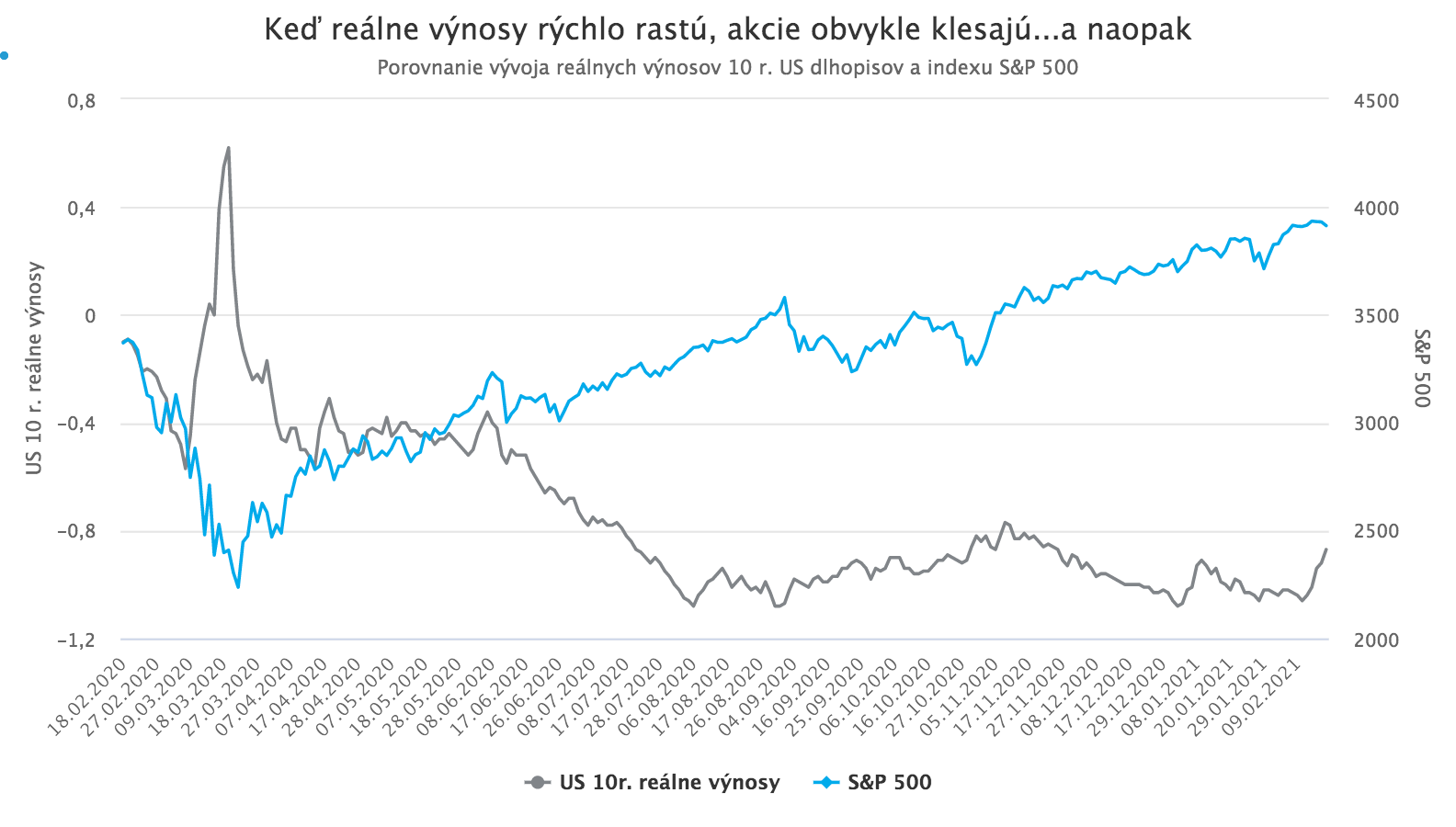

In practice, however, it also turns out that episodes of an overly sharp and overly rapid rise in yields can temporarily derail the equity market, especially when not only nominal but also real yields increase. The last major decline in equity markets before the pandemic, at the end of 2018, was caused precisely by a rise in real yields.

For several weeks now, markets have been worried that the current rise in yields, driven by the pro-cyclical rotation that began in November, is already too sharp and could have a negative impact on the equity market. In a situation where stocks, according to standard valuation ratios, are as overvalued as they were at the peak of the dot-com bubble, concerns about the negative effect of rising yields on equity valuations are especially intense.

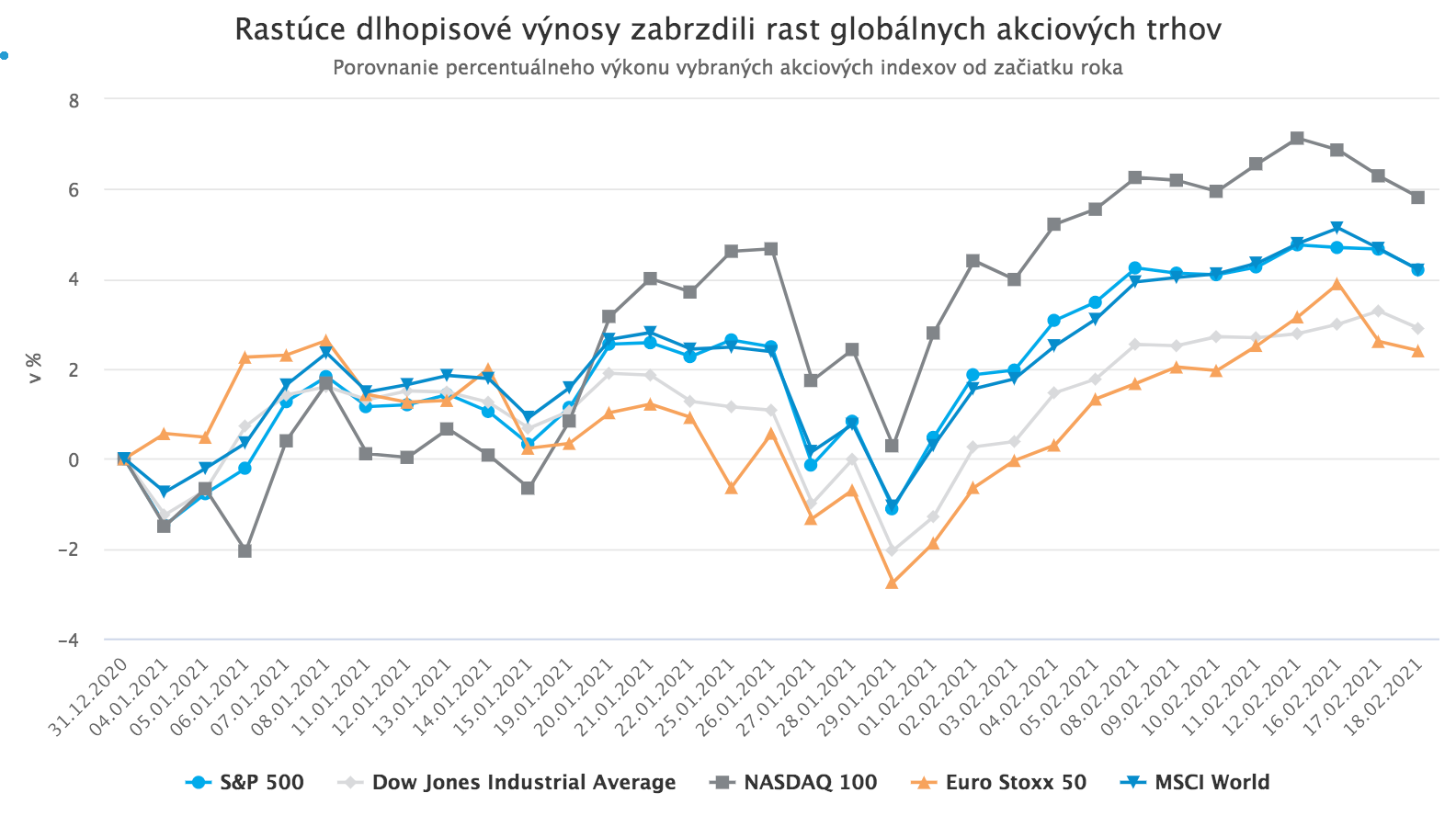

This week’s rapid rise in bond yields back to yearly highs and to pre-pandemic levels spooked equity markets and brought their long streak of rising days to an end. The biggest declines were seen precisely in the stocks that benefited the most from an environment of falling real yields and are considered a (higher-yielding) substitute for bonds, namely the shares of the largest US technology companies. That is why, in recent days, the Nasdaq has fallen the most sharply among the major equity indices, since the five largest US technology companies make up more than 40% of its weight.

Rising bond yields also affect other assets

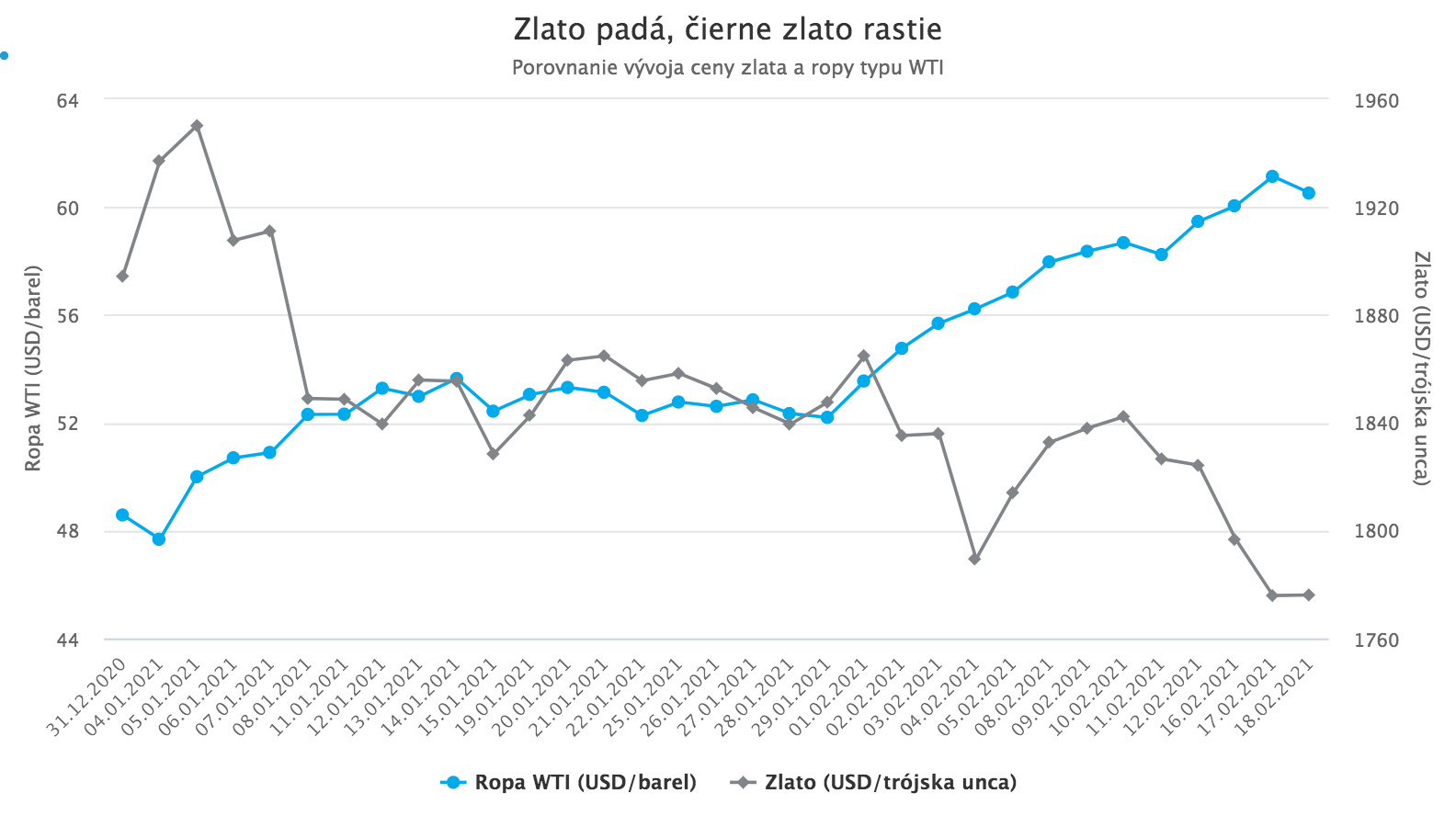

Rising yields are also affecting other assets. Gold can “envy” bonds their worst start to the year in 13 years. This precious metal is currently experiencing its worst start to the year in the last 30 years. It is being pulled down by rising yields. Gold’s decline amid rising inflation expectations may seem paradoxical if we view gold primarily as an inflation hedge; however, as we have emphasized several times in the past, gold responds above all to the development of real yields, and those are now rising.

Since it does not generate any yield itself, it simply loses its luster compared with US Treasuries, which are also considered an exceptionally safe asset and do provide a yield. While gold is falling, industrial metals are doing well, benefiting from the expected economic recovery and rising inflation expectations. Oil is also posting strong gains at the moment, although these are not driven only by positive macroeconomic expectations but also by the current energy crisis in Texas, where severe морозs caused an outage in oil production of up to 4 million barrels per day, that is, 40% of US production capacity.

So far, rising yields have not had a significant impact on the foreign-exchange market. The dollar has strengthened only very slightly in recent days, although higher yields on dollar-denominated bonds should, in theory, markedly increase its attractiveness. It appears that the effect of the continued massive inflow of capital into emerging markets, which should benefit the most from the expected global economic recovery, has so far neutralized pressure for the dollar to strengthen.

From the perspective of risk assets and the global economy in general, this can be seen as a piece of good luck. A strong dollar traditionally slows global economic growth and is unfavorable for risk assets, including equities. Dollar bond yields therefore currently rank among the key economic indicators worth watching closely. Their further development will have a fundamental impact on a wide range of assets and could even influence the real economy.