The EU issued its first bonds to finance the post-pandemic economic recovery.

On 15 June, the European Union sold its first joint European bonds intended to finance the post-pandemic economic recovery. This tranche totaled EUR 20 billion and consisted of 10-year bonds with a 0% coupon. It turned out that institutional investors have enormous interest in this type of security. Demand exceeded supply by more than seven times. As a result, the EU joint bonds were sold at a price corresponding to a yield of 0.086%, that is, about 30 basis points above the yield on German bonds with the same maturity. Most EU countries currently borrow at higher rates than that.

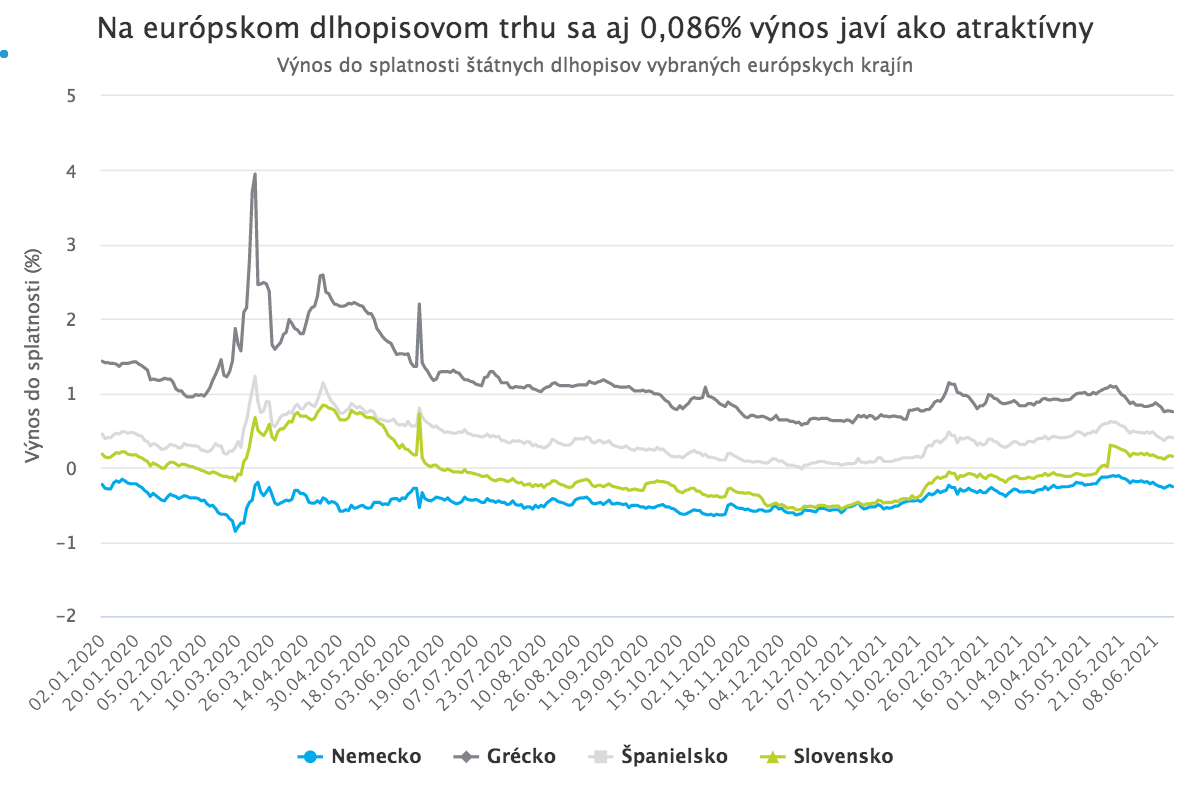

A yield barely above zero on a ten-year maturity can, of course, hardly be considered attractive. Even given generally low yields in the bond market, there are several higher-yielding alternatives. However, for banks, insurers, and other institutional investors who, due to regulatory requirements, must invest a significant portion of their portfolios in highest-rated bonds denominated in their domestic currency, this is still a relatively more attractive alternative compared with German bonds, which still offer a negative yield. The strong demand from European institutional investors for these securities is therefore not surprising.

This closely watched transaction was, to date, the EU’s largest syndicated bond sale. Its significance, however, lies primarily in the fact that it was only the first part of an issuance program with a planned volume of up to EUR 800 billion, intended to finance the Next Generation EU fund designed to support the recovery of European economies after the pandemic.

Joint European bonds

The creation of the Next Generation EU recovery fund was a key component of the plan to revive the European economy after the coronavirus crisis, presented by the European Commission in May last year and, after months of negotiations, ultimately approved. The most revolutionary part of the plan was the way it would be financed. Member states agreed that the European Commission would raise funds for the program by issuing bonds on financial markets; these bonds would not be issued separately by individual member states, but by the European Commission itself. This means they will effectively be a common EU debt instrument, backed by all member states regardless of which countries ultimately receive the largest share of the fund’s resources.

The wealthier northern countries, led by Germany, had long opposed such a step out of concern that they would have to guarantee the debts of highly indebted southern countries. However, the unprecedented economic downturn caused by the pandemic contributed to a reassessment of these positions. Technically, the European Commission backs these bonds with its budgetary headroom, namely the difference between the maximum amount of resources it can request from member states to finance the budget and the budget’s expenditure ceiling.

The obvious advantage of such bonds is that the EU as a whole, represented by the European Commission, can borrow in the markets on more favorable terms than weaker, more indebted economies could on their own, since the European Commission has the highest credit rating, AAA. It can therefore raise funds for member states on significantly better terms than countries such as Italy, Spain, or Greece would be able to secure independently. This assumption was confirmed in Tuesday’s first-ever sale of these bonds. Among the large EU countries, only Germany currently borrows more cheaply than the European Union itself.

EUR 20 billion is only the beginning

Tuesday’s bond sale of EUR 20 billion was only the first part of a large issuance program to finance the Next Generation EU fund, spread out over several years. The European Union aims to raise EUR 750 to 800 billion in this way by the end of 2026. The next two syndicated bond sales of a similar size will likely take place as early as next month, and the EU plans to issue bonds totaling EUR 80 billion this year. This means that, as an issuer, the European Union will be issuing volumes comparable to those of the largest member states in the coming years. This is a new element that will fundamentally reshape Europe’s capital market.

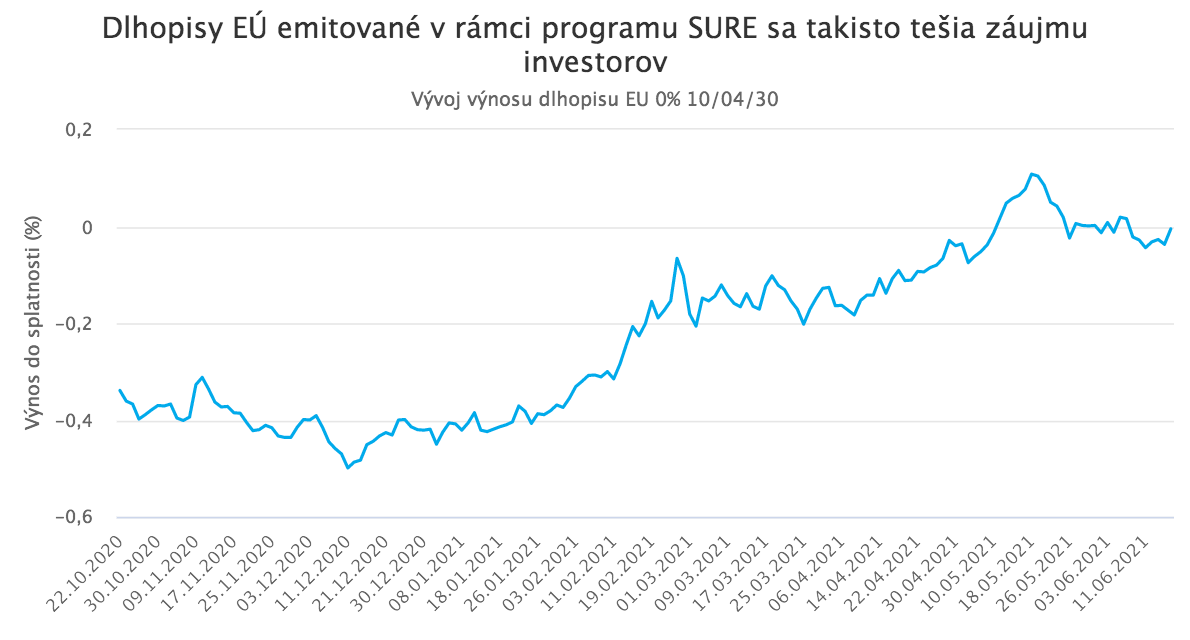

The European Union is not entirely new to bond markets; however, until now it issued bonds only occasionally and in relatively small volumes compared with individual member states. The first more meaningful volumes came only at the end of last year, when the European Commission launched social bond issuances under the EU SURE program, which, like Tuesday’s issuance, also attracted strong investor demand.

In any case, the volume of EU bonds outstanding in the market today is only around EUR 154 billion. However, if issuance under the economic recovery program continues over the coming years as planned, by the end of 2026 there will be almost EUR 1 trillion of joint European bonds in circulation. This volume will make the EU the largest supranational borrower and, beyond the political implications, it will also have a significant impact on European and global capital markets.

An issuance that will reshape the global capital market

EU bonds are well suited to assume the role of a benchmark in the European bond market, a role currently held by German Bunds. As bonds with the highest credit rating, they are also likely to become sought-after collateral. Until now, low issuance volumes have prevented them from fully taking on either of these functions.

As much as one third of the planned EUR 800 billion to finance the recovery will consist of so-called green bonds. Such a volume of green bonds from a major supranational issuer with the highest rating will significantly improve liquidity across the market and may inspire other major companies and institutions to follow suit. The first sale of EU green bonds is expected as early as this autumn.

The growing volume of joint European bonds will also likely have a long-term stabilizing effect on the bonds of riskier European countries. Already when the European Commission first presented the plan to issue joint European bonds in May, yields in countries such as Greece, Italy, and Spain fell significantly.

Finally, the expanding volume of joint European bonds is likely to have major implications for the currency market as well. Rising EU indebtedness may intuitively seem like negative news for the euro; in reality, however, it could strengthen the euro’s position among reserve currencies. One of the most important factors preventing the euro from becoming a global reserve currency today is the low volume of safe euro-denominated assets. European countries with the safest bonds, such as Germany or the Netherlands, issue relatively few securities compared with the U.S. or Japan, while the bonds of other European countries are not considered risk-free. Investors are therefore reluctant to hold large euro reserves because there are not enough assets in which to park them with minimal risk. EU bonds could change that.