The Euro Area Is Haunted by Deflation

Since the outbreak of the Covid crisis, economists and market analysts have debated intensely whether the shock would prove inflationary or deflationary. For a time, both outcomes appeared similarly plausible. On the one hand, there were forces with clear inflationary potential: disrupted supply chains, forced production shutdowns across many industries, deglobalization pressures, and unprecedented fiscal and monetary stimulus. On the other hand, the crisis also delivered a massive demand shock as living standards deteriorated, unemployment rose, and uncertainty surged, a “deflationary supernova” for the economy.

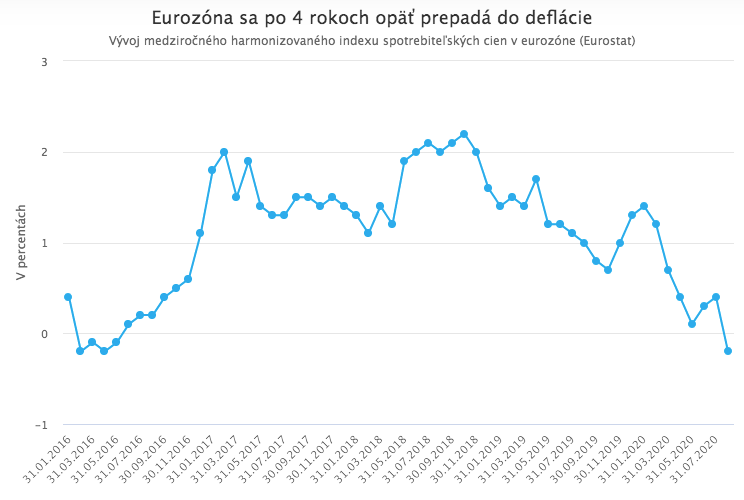

It is now becoming increasingly clear that deflationary pressures are prevailing. Consumer prices in the euro area fell in August for the first time in more than four years. Headline inflation declined by 0.2% year on year, even as economists had expected a 0.2% increase.

Deflation is not the only problem

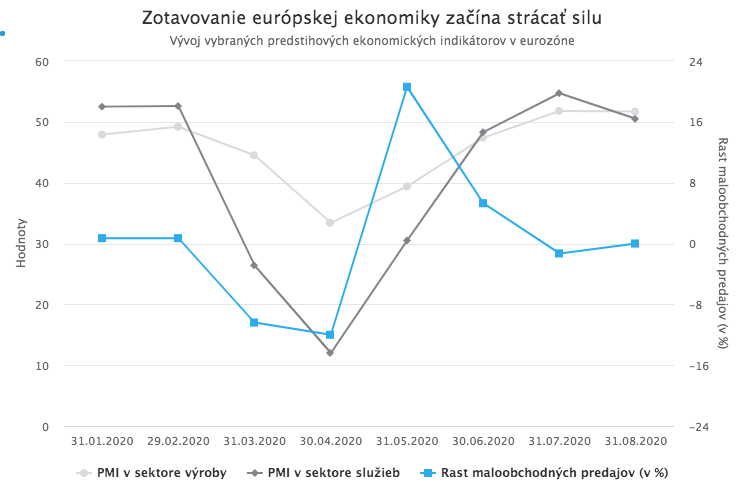

The euro area is slipping into deflation at an exceptionally inconvenient moment, just as its economic recovery is beginning to lose momentum.

Compounding the situation is the strength of the euro, which has appreciated by around 9% over the past four months and pushed up toward 1.20 EUR/USD, its strongest level in two years. This creates two problems. A strong euro weighs on European exports, further slowing the recovery, while also cheapening imports, which can reinforce disinflationary and deflationary pressures.

While the ECB’s own research suggests that exchange-rate pass-through to inflation has weakened in recent years, ECB Chief Economist Philip Lane acknowledged this week that the central bank views euro strength as an issue that warrants attention.

What will the ECB do?

The European Central Bank therefore faces a trio of interconnected challenges: deflationary pressures, a cooling recovery, and an appreciating currency. It is likely to respond as early as its next meeting on 10 September, either by easing policy further or by signaling an intention to do so. In principle, additional accommodation should support growth, lift inflation, and put downward pressure on the euro.

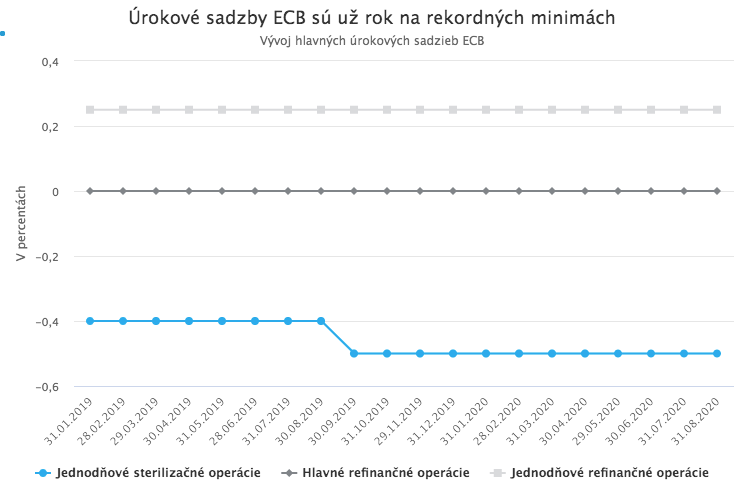

The problem is that the ECB has limited room left to ease. Policy rates have been at record lows for over a year, and further cuts deeper into negative territory are unlikely given the increasingly visible side effects of very negative rates, effects the ECB is well aware of.

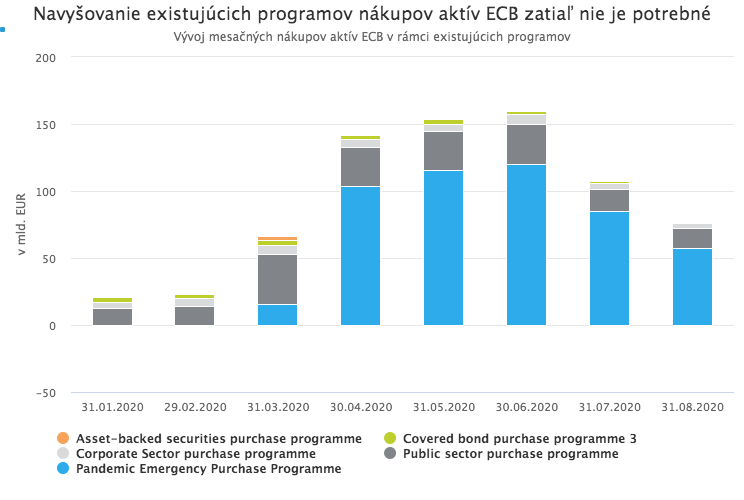

Another option would be to expand asset purchases, in effect “turning up the printing press.” Yet that, too, appears unlikely in the near term because the ECB still has substantial capacity within existing programs, without needing to adjust headline envelopes or announce new initiatives.

Most purchases currently run through the Pandemic Emergency Purchase Programme (PEPP), whose size was increased in June by EUR 600 billion to EUR 1.35 trillion and is scheduled to run at least until end-June 2021. After the first six months, less than EUR 500 billion had been used. Monthly purchase volumes have gradually declined, and conditions in bond markets have not provided a strong rationale for accelerating them. The most plausible outcome, therefore, is a form of verbal intervention at Thursday’s meeting, with the ECB signaling the possibility of further easing in the future.

For now, markets appear satisfied. Euro area bond yields fell notably over the week, both in the “core” and the “periphery.” Italian 10-year yields dropped by 11 basis points to below 1%, while German Bund yields moved further into negative territory, approaching -0.5%. The euro eased from around 1.20 to roughly 1.185 EUR/USD, and six-month Euribor fell to a record low of -0.455%. European equities were on track for gains until they were dragged lower by a sell-off in U.S. technology stocks on Thursday.

Cure or cause?

While few doubt that the ECB’s response will be further easing, or at least signalling it, there is growing skepticism about whether this is the right prescription. It is entirely possible that ultra-loose monetary policy is not a remedy for deflation but, paradoxically, one of its key drivers.

One of the side effects of prolonged monetary accommodation is the “zombification” of the economy, a risk many economists have warned about for years. The term describes a process in which record-low interest rates and bond yields suppressed by central bank interventions allow inefficient and heavily indebted firms to access capital on favorable terms. These companies are effectively kept alive artificially, whereas in a healthier market environment they would exit and be replaced by more productive, financially sound firms.

As the number of such zombie firms rises, the economy can be left with excess capacity, which compresses prices and margins and therefore exerts structurally deflationary pressure. A study published by the U.S. National Bureau of Economic Research in May, examining zombification in the European economy, concluded that in the absence of “zombie lending,” annual euro area inflation would have been 0.45 percentage points higher over the period studied (2012 to 2016).

The share of companies whose profits are insufficient even to cover interest expenses has increased sharply in recent months due to the Covid shock and central bank interventions. Research by Krieter and Belton at BMO suggests that the proportion of such firms now exceeds 20% of the economy. Any additional monetary easing would, by lowering financing costs further, likely accelerate the proliferation of zombie firms and intensify deflationary forces.

The dilemma is that the main alternative to zombification, Schumpeterian “creative destruction” that purges bad investments and inefficient firms, is politically and socially brutal. It would likely entail a (at least short-term) surge in corporate and personal bankruptcies and a corresponding hit to living standards, an outcome neither politicians nor central bankers are willing to own. That is precisely why the ECB is likely to signal more easing on Thursday, even if it may do little to solve the deflation problem.