The Fed Fundamentally Changed Its Policy. Interest Rates Will Not Rise for Years, Possibly Decades.

The U.S. central bank announced a significant change in its strategy. Going forward, it will tolerate even a more persistent rise in inflation above the 2% target without trying to curb it by raising interest rates. This means interest rates likely will not rise for many years, possibly even decades.

The annual Jackson Hole symposium of central bankers is traditionally one of the most anticipated events of the year among economists and investors. This year, that was true twice over, as it was expected that Jerome Powell, Chair of the Fed, would announce a major revision of the U.S. central bank’s strategy.

Powell did not disappoint. On the very first day of the symposium, which this time took place only virtually due to the pandemic, he announced two important strategy changes with far-reaching consequences for the real economy and financial markets. The first concerns inflation, the second employment. People are speaking of an “epochal shift” and “the beginning of a new era.”

Problems with low inflation

The U.S. Fed, like other central banks including the ECB, considers it desirable for consumer prices to rise at an average rate of 2% per year. Mild inflation at around 2% is viewed, in the long run, as the most appropriate level both for economic growth and for price stability.

The Fed’s previous strategy, shaped in the years of high inflation, focused primarily on the risk of excessive inflation and assumed that whenever inflation began to rise above the 2% target, the bank would raise interest rates to dampen it and thereby preserve price stability.

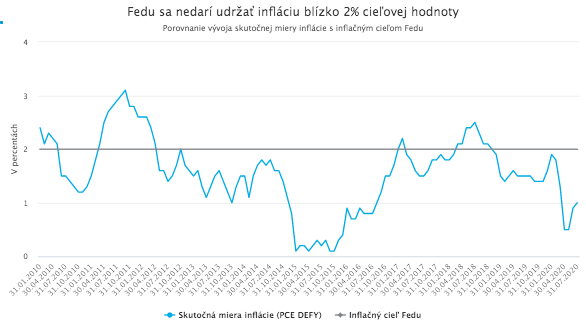

The problem, however, is that in recent years the U.S. economy (and not only the U.S. economy) has not had to struggle with high inflation, but rather with inflation that is too low. Persistently low inflation, well below the 2% target, has been one of the most striking features of the macroeconomic environment of the past decade, and it poses at least as serious a danger to the economy as overly high inflation. It dampens economic growth, raises the risk of a deflationary spiral, and at the same time forces the central bank to keep interest rates at very low levels for a long time, reducing its room to stimulate growth in times of crisis.

In the coming months and years, as the economy recovers from the largest deflationary shock in modern history, it is therefore more important than ever to bring inflation back toward target. But the Fed would have had difficulty achieving that under its previous strategy.

If inflation remains below 2% for a long time and it is expected that if it ever rises above 2%, the Fed will intervene (in line with its strategy) and raise rates to pull it back below 2%, then expected average inflation over the longer term will always remain well below the desired 2%. Since expected inflation is to a large extent a self-fulfilling prophecy with a decisive impact on actual inflation, the Fed’s prior inflation-targeting strategy had little chance of delivering the desired inflation rate.

The newly announced change in the Fed’s strategy is an admission of this problem and an attempt to find a new way to stimulate inflation back toward the target level in today’s environment.

AIT arrives

The Fed’s new inflation strategy is known as AIT (Average Inflation Targeting). The idea is very simple: if inflation rises above 2% after a prior period of low inflation, the Fed will not try to immediately bring it down. Temporarily higher inflation then compensates for the earlier period of low inflation, and average inflation over a longer horizon reaches the 2% target.

In Powell’s words: “We will seek to achieve inflation that averages 2 percent over time. Therefore, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

However, this strategy will not be governed by any specific formula or rule defining over what time horizon inflation should average 2% and what deviations are acceptable:

“Our efforts to achieve inflation that averages 2 percent over time will not be tied to a specific mathematical formula that defines that average. Thus, our approach could be viewed as a flexible form of average inflation targeting. Our monetary policy decisions will continue to reflect a wide range of factors and will not be dictated by any single formula. Of course, if we were to see excessive inflationary pressures or inflation expectations moving materially above levels consistent with our goal, we would not hesitate to act.”

This approach gives the Fed considerable flexibility, but it is also an open question whether its lack of specificity could hinder the formation of clear inflation expectations, and thus the achievement of the goal itself.

Interest rates will not be raised

The only certainty and concrete implication of the new Fed strategy is that interest rates will not be raised even if inflation were to start rising above 2%. In practice, that means they will not be raised for a very long time.

The inflation indicator monitored by the Fed averaged 1.72% over the past 20 years. Inflation was above the 2% target only 27% of the time, and even then only slightly. That means that if the Fed had followed an average-inflation-targeting strategy in the past, it likely would not have meaningfully raised interest rates even once over the last 20 years.

Given long-term macroeconomic trends, it is reasonable to expect that the coming years and even decades will not be different with respect to the inflation trajectory. The bigger issue is likely to be low inflation rather than high inflation. Even the Fed’s own forecasts, traditionally overly optimistic, do not project inflation reaching even 2% by 2023.

It is therefore quite likely that the rate-hiking cycle launched in 2018 by Powell himself, interrupted by the trade war and definitively ended by the pandemic, was the last meaningful period of rate increases in advanced economies for a very long time.

This conclusion is reinforced by the second major strategy revision announced by Powell, which concerns employment.

The Phillips curve is broken

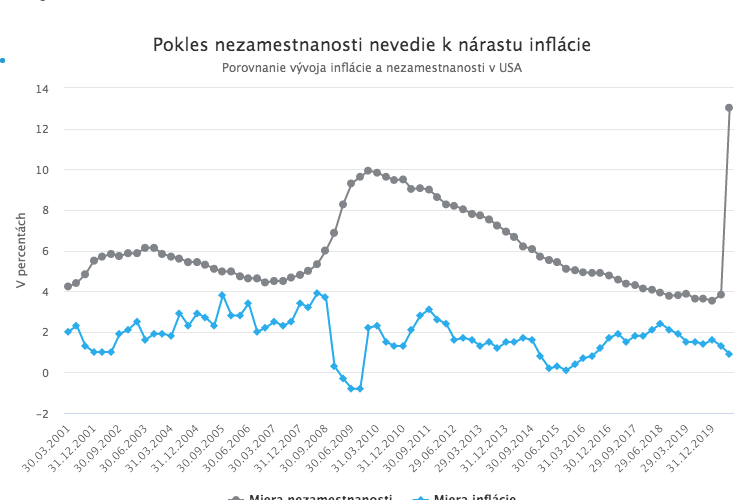

Until now, Fed policy was formally guided by the Phillips curve, which assumes an inverse relationship between unemployment and inflation. Under this concept, there is some “natural” unemployment rate (higher than 0%), and if unemployment were to fall below that rate, wage growth driven by a strong labor market would begin pushing inflation sharply higher.

That means that if the labor market “overheats”, that is, if unemployment drops below the estimated natural rate, the central bank should preemptively raise rates to “cool” the economy and labor market and thereby avert the risk of rising inflation.

It is a nice theory, it sounds logical, and 50 years ago it was even supported by empirical data. The only problem is that today this relationship apparently no longer works, or it is much less pronounced than in the past. One of the main reasons is likely that declining unemployment in the U.S. economy in recent decades has not translated into higher real wages.

That the Phillips curve no longer works is not news among experts. Powell himself acknowledged this during testimony in Congress in July last year, when, in response to a question by Alexandria Ocasio-Cortez about the relevance of the Phillips curve, he said:

“The relationship between unemployment and inflation was very strong 50 years ago, but it’s been weakening and today it’s barely visible … the economy can sustain much lower unemployment than we thought without inflation rising in a troubling way.”

Formally recognizing this reality is at the core of the second major change in the Fed’s strategy announced by Powell at the virtual Jackson Hole symposium.

Under the new strategy, in relation to the labor market, the Fed will, similar to its approach to inflation, tolerate even a prolonged decline in unemployment below the estimated “natural” level without slowing the growth of the economy and employment by raising rates out of fear of inflation.

This change is, of course, logical and correct. If employment growth does not lead to higher inflation, then artificially restraining it by raising rates is simply misguided. It is therefore positive that the Fed has finally, after years, chosen common sense and empirical data over clinging to outdated theoretical economic doctrines.

Looking ahead, this opens the door to adopting more effective economic measures aimed directly at supporting the middle class, which the Fed had previously resisted precisely because of inflation fears. Powell also confirmed this point during his congressional testimony a year ago.

Market reaction

As with other major changes, it will take investors some time to assess what the Fed’s strategy shift will mean in practice and for that consensus to be reflected in asset prices. The initial market reaction, however, was broadly encouraging.

U.S. equities, benefiting from the not-so-surprising vision of perpetually low interest rates, rose slightly on the day of Powell’s speech. The U.S. Treasury yield curve moved higher at longer maturities, likely reflecting some market confidence that the Fed will succeed in lifting inflation closer to target over the long term. Gold fell, as usual reacting mechanically more to yield movements than to vague fears of future inflation. The dollar strengthened very slightly.

In the coming days, it will be particularly interesting to watch movements in the U.S. yield curve. If investors ultimately believe that the Fed will manage to raise inflation, longer-maturity bond yields will rise. That would mean a sell-off in this segment of the bond market. Too sharp an increase in yields, however, could trigger a correction in the equity market.