ECB Increased Its Bond-Buying Program to EUR 1.85 Trillion

The Pandemic Emergency Purchase Programme is one of the ECB’s most powerful tools. Thanks to it, Greece can now borrow more cheaply than the United States, and a growing number of eurozone member states, including Slovakia, can even issue bonds with negative yields.

At its December meeting, the ECB’s Governing Council decided to increase the envelope of the Pandemic Emergency Purchase Programme by a further EUR 500 billion and extend it at least until March 2022. The total capacity of the programme has thus climbed to an astonishing EUR 1.85 trillion. This decision was widely expected given the renewed slowdown of European economies due to the second wave of the pandemic, and markets welcomed it.

At the same time, the ECB introduced several other changes to its toolkit. For example, it decided to extend the period of favorable terms under the third series of longer-term refinancing operations (TLTRO III), add further rounds of pandemic emergency longer-term refinancing operations (PELTRO), and continue the regular asset purchase programme at the usual pace of EUR 20 billion per month. The overarching goal of these measures is to ensure a sufficient supply of ultra-cheap liquidity and thus encourage banks to lend and invest in the real economy.

The ECB’s key interest rates remained unchanged. It is assumed that cutting them further, deeper into negative territory, would bring more negative effects than benefits.

The ECB’s key tool

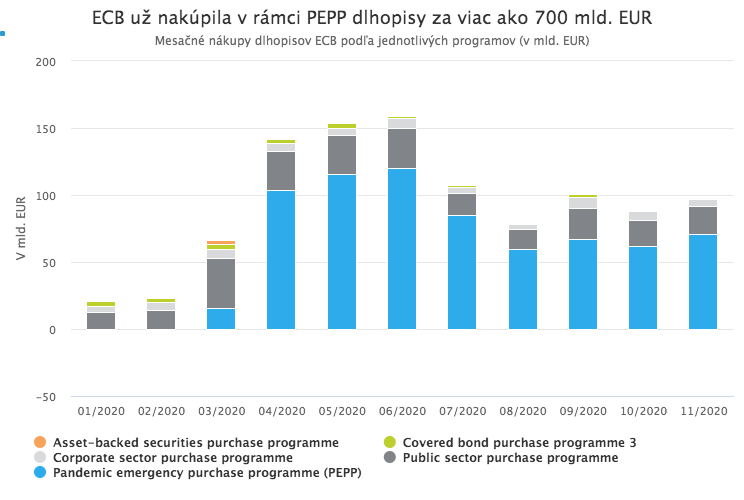

The Pandemic Emergency Purchase Programme, known by the acronym PEPP, is currently the ECB’s key tool in the fight against the economic consequences of the pandemic. The bank introduced it in March of this year.

PEPP is one of the unconventional monetary policy instruments built on the mechanism of quantitative easing. That means that under this programme, the ECB buys bonds in the market from banks and other financial institutions in exchange for newly created euros in the form of bank reserves. This process is therefore often referred to as “printing money.”

PEPP is not the first or the only ECB tool operating on such a principle. Compared with other quantitative easing programmes, however, its advantage is high flexibility and substantial “firepower.” Right after it was introduced, it became the ECB’s most important tool for supporting liquidity. Its original capacity at launch in March was EUR 750 billion. Given the volume of monthly asset purchases and the expected longer duration of the crisis, it quickly became clear that EUR 750 billion would not be enough. The ECB therefore first increased it in June by EUR 600 billion to EUR 1.35 trillion, and now, finally, by another EUR 500 billion to EUR 1.85 trillion.

The cumulative volume of assets purchased under PEPP as of the end of November slightly exceeded EUR 700 billion. That means its original capacity has been almost exhausted in less than nine months. If the programme is to continue at a similar pace at least until March 2022, an increase would have been needed sooner or later.

Flexibility against fragmentation

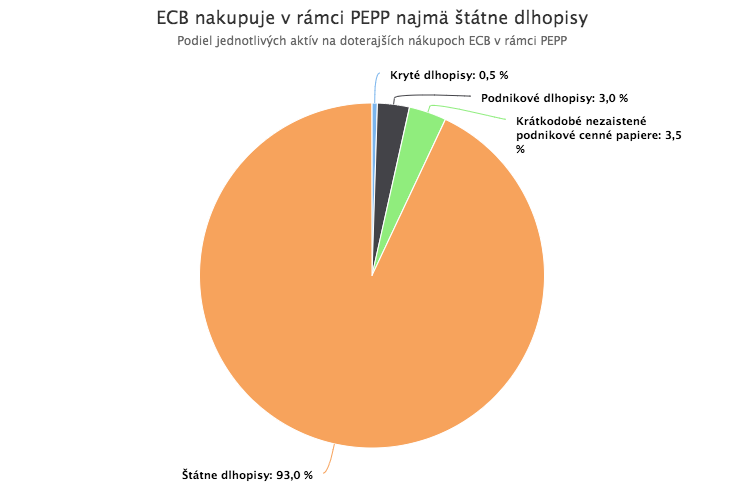

Under PEPP, the ECB primarily purchases government bonds of eurozone member states.

Its key advantage compared with the ECB’s standard asset purchase programme, which has been running for several years and also focuses on buying eurozone government bonds, is flexibility. Under PEPP, the ECB does not have to strictly follow the capital key that obliges it in other programmes to buy each country’s bonds in proportion to the size of its economy. That means it can, as needed, direct more money toward buying bonds of countries that are most affected by the pandemic.

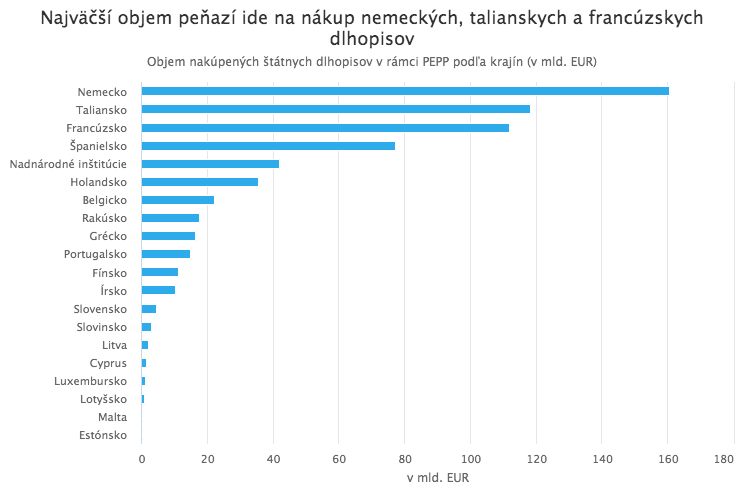

This flexibility is hugely important at the moment because it prevents fragmentation of the eurozone. The pandemic hit southern countries such as Italy, Spain, and Greece the hardest, and they already had the highest debt levels in the eurozone even before the outbreak. If the ECB were not massively buying these countries’ bonds through PEPP, their borrowing costs would surge and a debt crisis would erupt, compounding the problems caused by the pandemic.

Record-high debt, record-low interest costs

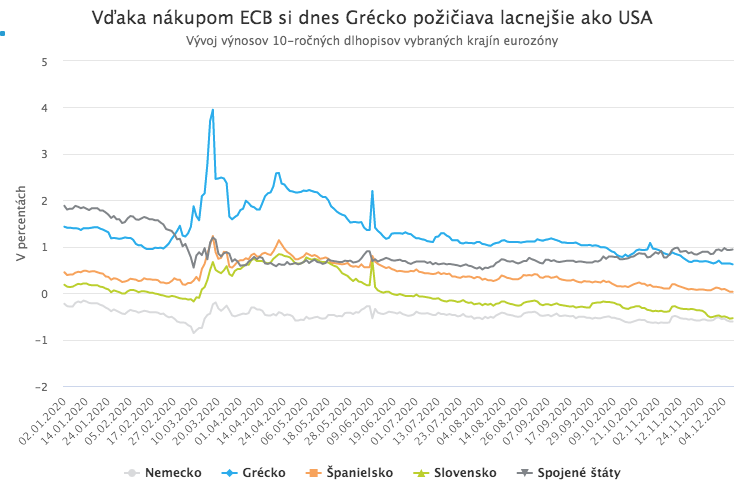

PEPP’s extraordinary effectiveness is demonstrated by the development of eurozone government bond yields. Yields of “peripheral” countries such as Italy, Spain, and Greece fell sharply immediately after PEPP was announced, and, with small pauses, continued to decline throughout the rest of the year. These countries can now borrow at record-low rates, even though their public debt levels are higher than during the European debt crisis.

Greece can now borrow more cheaply than the United States. Yields on 10-year Portuguese bonds, the first southern eurozone country to do so, fell below zero for the first time this week. Spanish yields fell close to zero. Safer eurozone countries with lower debt have seen yields continue to decline deeper into negative territory. Yields on 10-year Slovak government bonds have already fallen below -0.5% and are approaching those of the safest German bonds.

Thanks to the ECB, eurozone countries can now borrow extremely cheaply and do not have to fear a sharp rise in interest costs like the one Greece experienced not long ago. They have gained more fiscal space to address the consequences of the pandemic. How they use it is, of course, an entirely different issue.

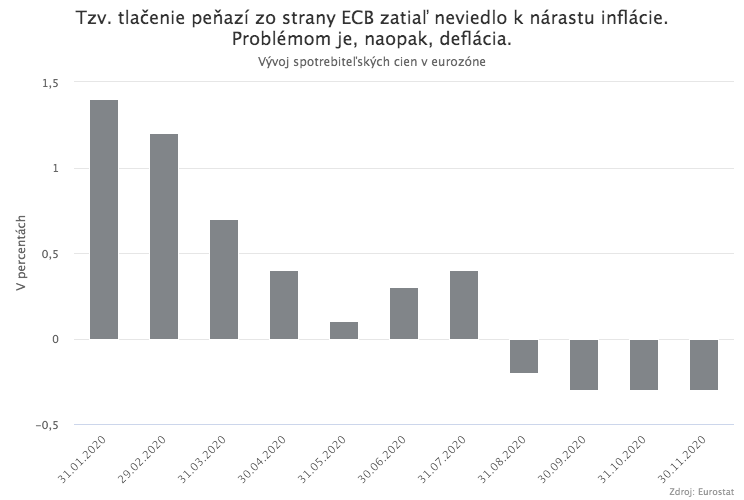

Should we fear inflation?

PEPP is, of course, not a miraculous cure-all without negative side effects. Critics of PEPP and quantitative easing in general often warn that such massive “money printing” by the central bank will lead to a sharp rise in inflation and a debasement of the currency. However, this most common objection to PEPP does not seem to apply here.

The eurozone currently has precisely the opposite problem: deflation and a currency that is strengthening too quickly. Consumer prices have been falling for four consecutive months, and even according to the ECB’s latest forecasts this trend will continue for several more months. This is happening despite the ECB’s “printing presses” running at full speed and the eurozone money supply currently growing at a 10% year-on-year rate.

Inflation is not a simple function of the amount of money in the economy. If the newly created money remains on commercial banks’ accounts at the ECB as excess reserves and does not enter the real economy through loans or investments, there is simply no reason why its growth should translate into higher consumer prices.

Moreover, the current crisis has brought strong deflationary pressure, as consumers and businesses cut spending, either out of caution and precautionary saving or forcibly due to falling income caused by job losses or bankruptcies. It is therefore not surprising that prices in the eurozone are currently declining, and the ECB’s “printing presses” likely will not be able to lift them even to the desired 2% increase, let alone into any inflationary spiral.

The problem of a strong euro

Deflationary pressures in the eurozone are also reinforced by the euro’s rapid appreciation. The common European currency has gained as much as 8% against the dollar since the start of the year. Against most world currencies it has posted double-digit gains. This is a problem for two reasons. A strong euro hurts European exports, further slowing Europe’s economic recovery, and at the same time it makes imports cheaper, which can “import” deflationary pressures.

It was therefore expected that the ECB might take some action against the euro’s strengthening. So far, however, it has not. Christine Lagarde, the ECB President, mentioned at Thursday’s meeting that “the ECB will monitor exchange rate developments and their implications for the medium-term inflation outlook,” but at the same time she emphasized that the ECB’s objective is not to influence the exchange rate.

The euro strengthened immediately after these words, and it seems nothing will stand in the way of its further rise.