The rapid rise in inflation in the US spooked the markets.

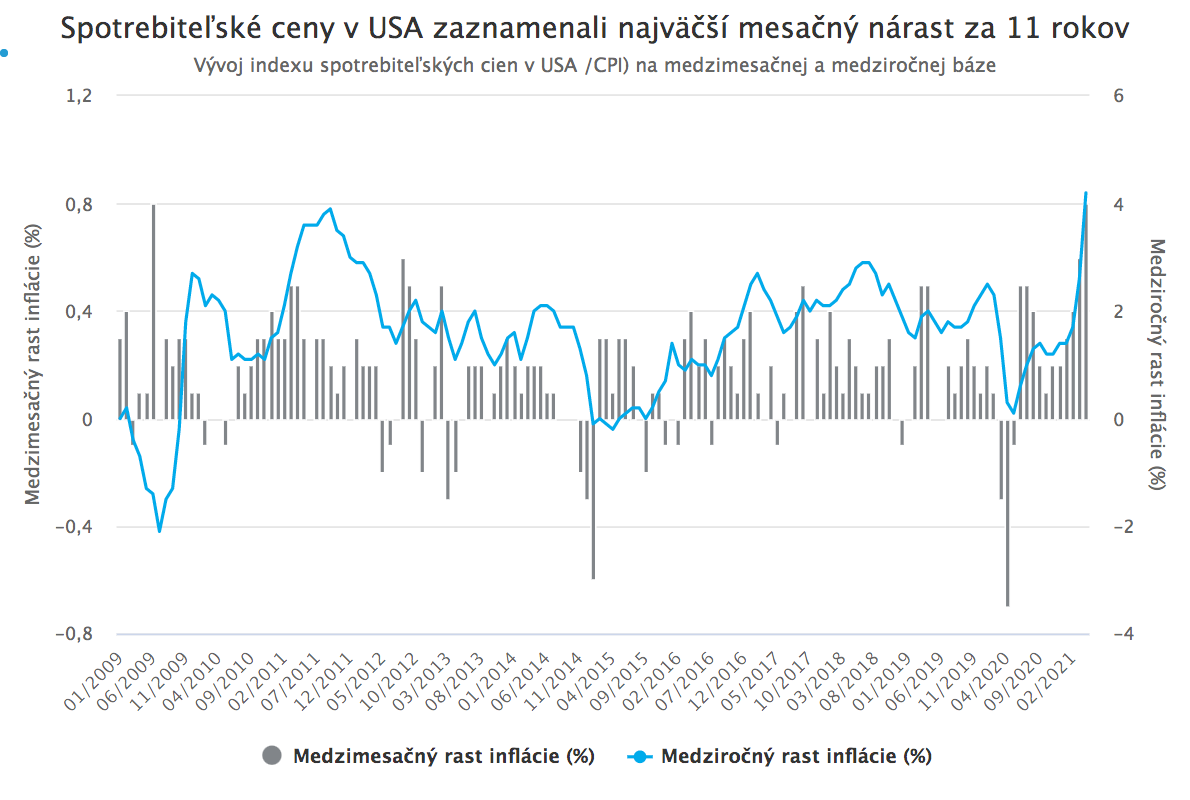

Consumer prices in the United States rose by 0.8% last month. This is the largest month-on-month increase in 11 years. On a year-on-year basis, this represents growth of as much as 4.2%.

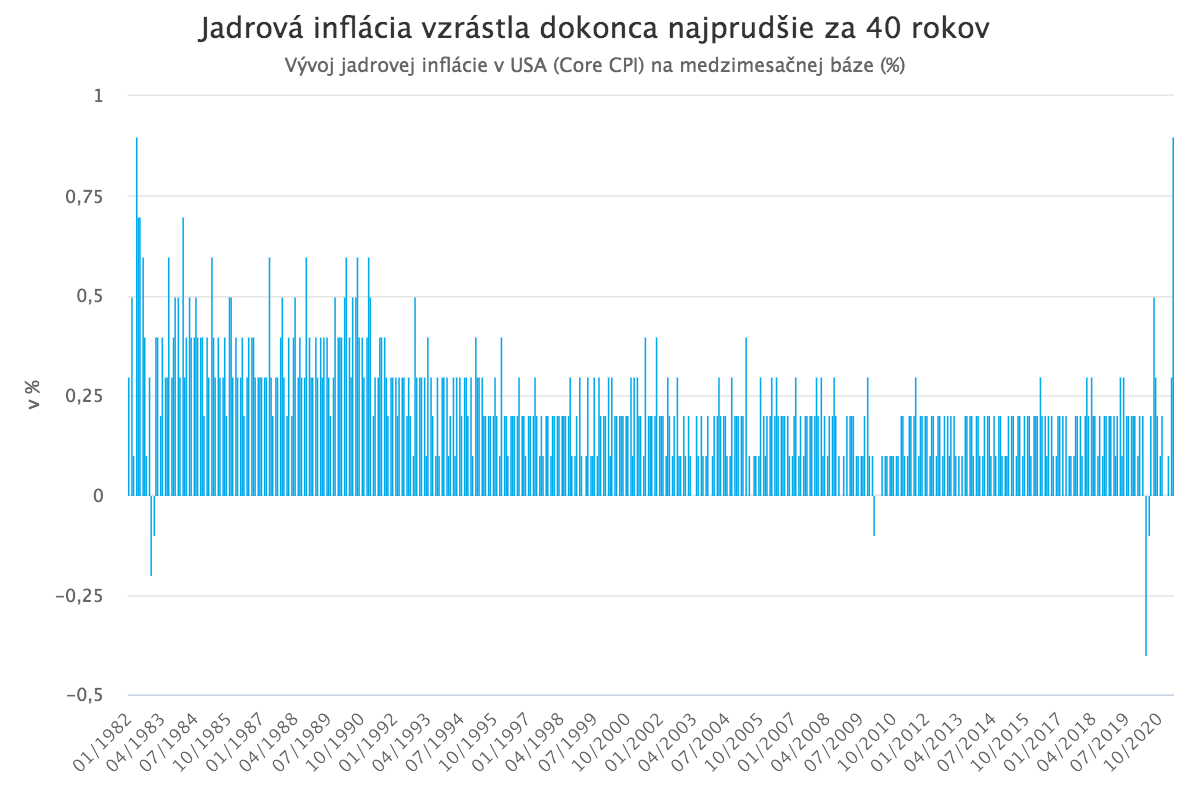

Although the increase in consumer prices was generally expected due to the rapid recovery of the U.S. economy, the low base effect, and substantial stimulus measures, the April figures still came as a surprise. Economists, on average, had expected only a 0.2% month-on-month rise in prices, and even the highest estimates had projected only 0.4% growth. The sharp 0.8% monthly increase in inflation, double the highest forecasts, therefore caught both economists and investors off guard. Core inflation even rose at the fastest month-on-month pace in four decades.

Just a short-term spike, or the beginning of a new era of higher inflation?

At present, it is not clear whether this is only a temporary, short-term increase that will naturally subside after a few months, or whether higher inflation will become the new “normal”. The low base effect, high accumulated savings (also thanks to generous stimulus), and only gradual restoration of normal business operations, many of which still have disrupted supply chains, suggested that once the economy began to reopen and consumers poured their accumulated savings into it within a few weeks, prices could spike in the short term. However, once businesses adapt to demand, restore normal operations, and consumer spending stabilizes at typical levels, price growth should ease. This is also the scenario the Fed expects, and it naturally has its logic. A closer look at last month’s inflation data largely supports it. The sharp April increase in the consumer price index was driven to a large extent by a 10% rise in used car prices, resulting from the ongoing chip shortage in manufacturing, as well as by rising prices in reopening sectors such as dining and recreation.

However, the magnitude of April’s inflation increase, combined with persistent rises in commodity prices and U.S. companies’ difficulties in rehiring workers, which is already forcing them to raise starting wages, is leading some economists and investors to expect that rising prices, wages, and commodities will continue for a longer period and reinforce one another in an inflationary spiral. Of course, we are not talking about hyperinflation, and probably not even double-digit inflation. Still, inflation at a level of 3 to 5% lasting longer than a few months would be a major shock for an economy and financial markets accustomed to exceptionally low inflation in recent years. In such a scenario, the Fed would have to move to earlier and more aggressive rate increases than originally expected, prioritizing price stability over maintaining extremely favorable conditions in financial markets. For investors, this would mean the need to significantly overhaul their portfolios, which today are largely built for an environment of disinflation, extremely low rates, and secular stagnation.

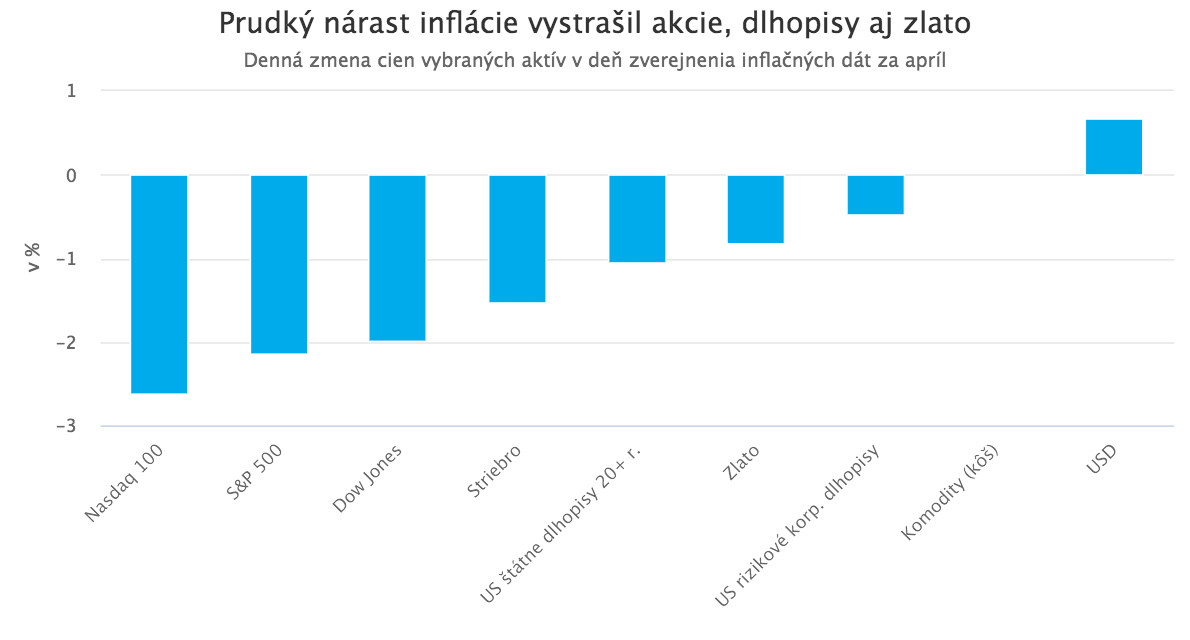

Inflation data pulled stocks, bonds, and gold lower

Concerns about a more persistent rise in inflation, which could, among other things, force the Fed to raise interest rates and significantly change the relative attractiveness of different asset classes, led to a sharp market reaction to the published inflation data. A closer look at the moves that occurred in the markets on Wednesday after these inflation figures were released also suggests what to expect if higher inflation becomes the new “normal”. Equity markets reacted to the data with a steep decline. Virtually all sectors ended in the red, with the exception of energy; however, the largest losses were, unsurprisingly, suffered by the stocks that have benefited most in recent years from an environment of low interest rates and low inflation, namely so-called growth stocks of the largest companies in the technology sector.

Among the major U.S. stock indices, Nasdaq, which has the highest share of such companies, recorded the largest decline. By contrast, the Dow Jones, which is more focused on industrial companies and has a smaller share of large technology firms than Nasdaq and also than the S&P 500, held up relatively best.

The threat of a sustained rise in inflation (and therefore the possibility of higher interest rates) naturally had a negative impact on the bond market as well. Bonds with longer duration, which are the most sensitive to changes in interest rates, fell the most. The TLT ETF, composed of U.S. Treasury bonds with maturities of 20 years or more and a typical component of classic 60/40 portfolios, fell by more than 1%. This was already the fourth consecutive daily decline. Yields on benchmark 10-year U.S. Treasuries rose by 8 basis points to just below the 1.7% level.

Significant moves also occurred in the currency market. The U.S. dollar strengthened sharply in response to the inflation surprise. At first glance, a strengthening dollar as a reaction to rising inflation in the U.S. may seem illogical; however, rising inflation (as long as it is not accelerating too quickly or erratically) increases the probability of interest rate hikes in the U.S., and higher interest rates are supportive for a currency because they increase the attractiveness of dollar-denominated investments.

A strong dollar, however, typically has negative effects on a range of other assets, and Wednesday was no exception. Emerging market stocks and bonds fell sharply, along with the currencies of their home countries weakening against the dollar. As the dollar strengthened, many commodities also declined, even though the outlook of higher inflation would otherwise tend to support them. Precious metals such as gold and silver, traditionally considered hedges against inflation, also fell. As we have pointed out repeatedly, the strength of the dollar and the level of U.S. dollar yields have a stronger influence on their prices than inflation expectations. The strengthening dollar and the increased probability of rate hikes therefore pushed gold prices lower, even as both realized and expected inflation rose.

Finally, “digital gold” also declined. Bitcoin fell by more than 5% on Wednesday even before Elon Musk’s tweet, which then sent it sharply lower. Immediately after the inflation data was released, it fell by 0.7%. So how can a portfolio be protected against rising inflation?

How to protect a portfolio against persistently higher inflation?

If it turns out that the current rise in inflation in the U.S. is not merely a temporary, short-term increase accompanying the first weeks of the economy “reopening” after the pandemic, but rather a persistent and longer-lasting rise, many investors will need to make significant changes to their portfolios in order to adapt to a new environment of higher inflation and higher interest rates.

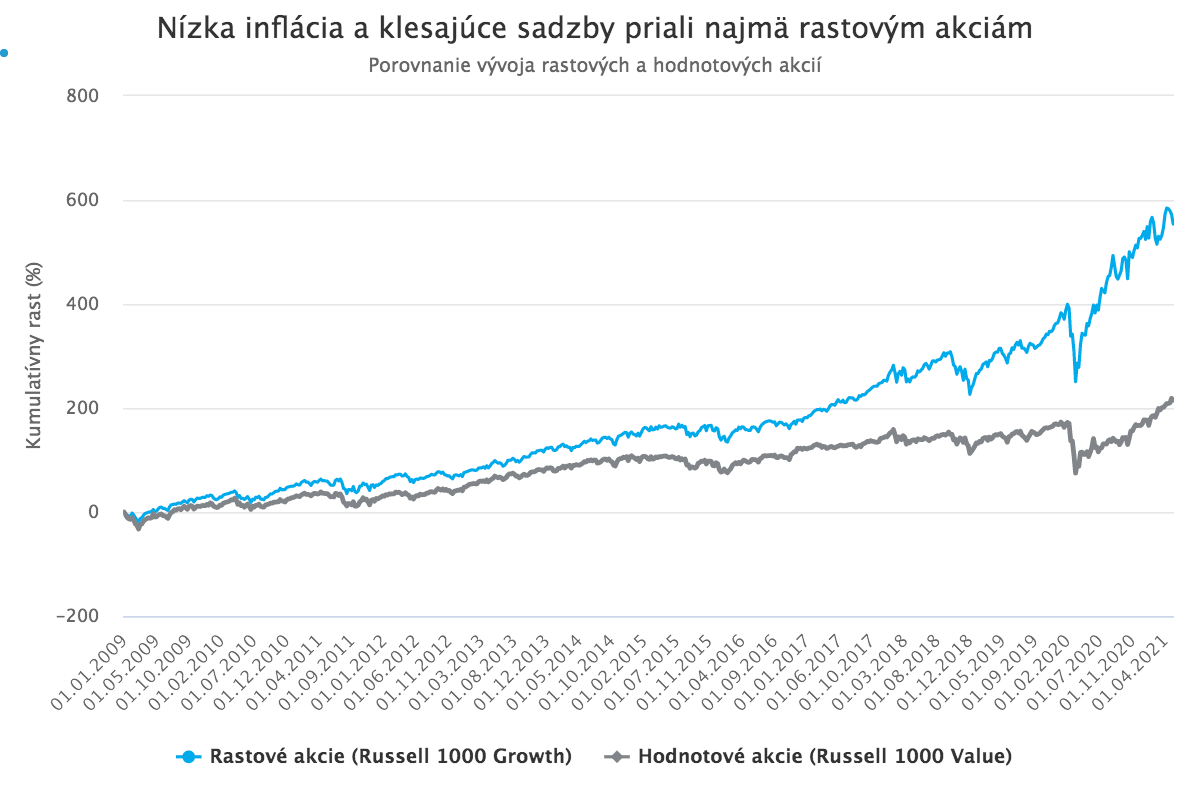

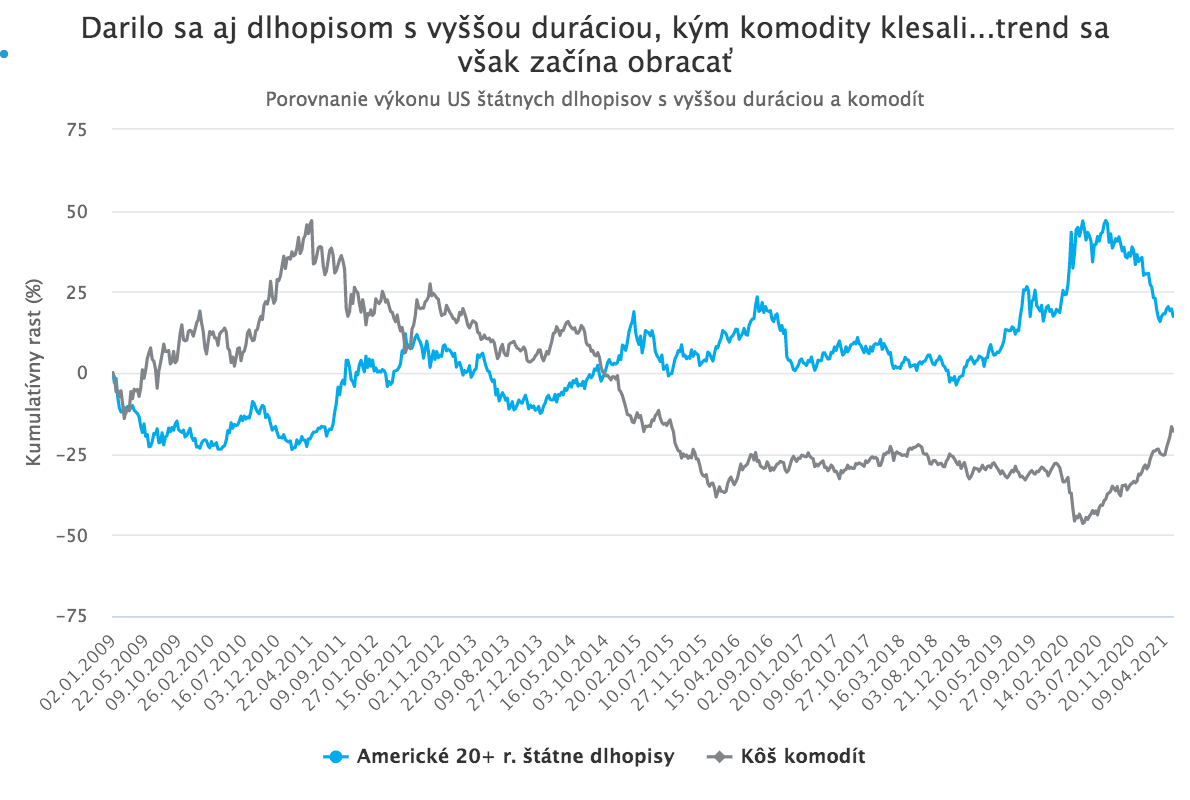

Since the global financial crisis, for more than a decade, the investment environment has been characterized by low inflation or even disinflation, weak economic growth, declining interest rates, and extremely accommodative monetary policy that suppressed volatility in financial markets. In such an environment, the assets and investment styles that benefited most were naturally those that thrive on low inflation, low volatility, and falling interest rates. These include primarily so-called growth stocks led by Big Tech, bonds with the longest possible duration, and assets serving as functional substitutes for bonds, in short, everything that is “long duration, short volatility.”

Over the years, investors gradually increased their allocation to this group of instruments at the expense of assets and investment styles that are, by contrast, “built” for an environment of higher economic growth, higher inflation, rising interest rates, and greater volatility. These include primarily so-called value stocks, cyclical stocks, small-cap equities, and commodities. For more than a decade, these significantly underperformed the first group, and investors steadily reduced their share in portfolios over the long term.

If inflation rises more persistently, accompanied by an economic recovery, higher interest rates, and increased volatility, the market move will be exactly the opposite, and a massive rotation across assets and investment styles will fully unfold. This rotation has, in fact, already begun in November after the introduction of the first Covid-19 vaccine and, with brief pauses, has continued for several months. However, trillions in portfolios are still waiting cautiously to see whether it will accelerate in full. If, however, inflation rises more significantly, there will be nothing left to wait for and the rotation will accelerate sharply.

Hundreds of billions shifting between asset classes would mean that it would not pay to remain on the “wrong side”, not only because of inflation or higher rates themselves, but also because of the huge reallocations between assets that can materially move their prices. The best way to protect a portfolio in the event of a longer-lasting rise in inflation (not only in the U.S.) is therefore to reduce its duration, increase the share of value and cyclical equities at the expense of growth stocks, reduce the allocation to bonds (especially those with longer maturities), and increase exposure to commodities or real estate, which tend to perform well in an environment of rising inflation.

At Sympatia, we will be happy to help you adjust your portfolio to changing macroeconomic and market conditions.