Stock markets remain under pressure, but there is no disaster yet

The new year did not start positively for stock markets, and most major indices ended the first quarter in the red. An interesting point is that most indices have erased the losses caused by the outbreak of the war in Ukraine and are even slightly up. The best-known index, the S&P 500, is down more than 5% since the beginning of the year; however, since the outbreak of the war it has gained more than 4%. Of course, after the conflict began, markets reacted with a sell-off, but those who took advantage of the panic have not had reason to regret it so far. The question is how long markets can withstand all the negatives prevailing in the world. Naturally, in the long run, investors who do not react panic-stricken tend to do well, because the main stock indices (S&P 500, Nasdaq, or MSCI World) still deliver an attractive return.

What challenges lie ahead for stock markets?

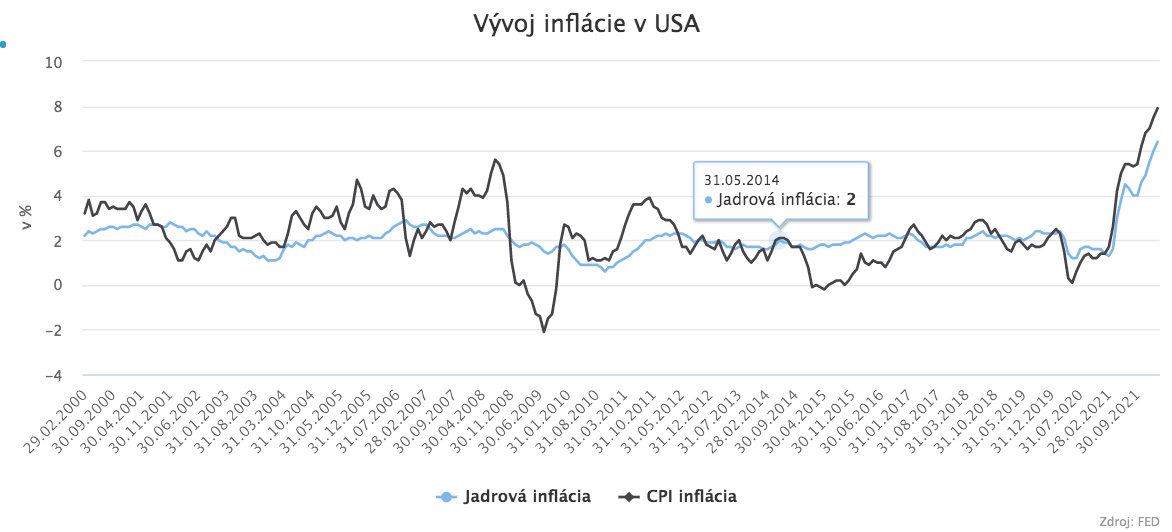

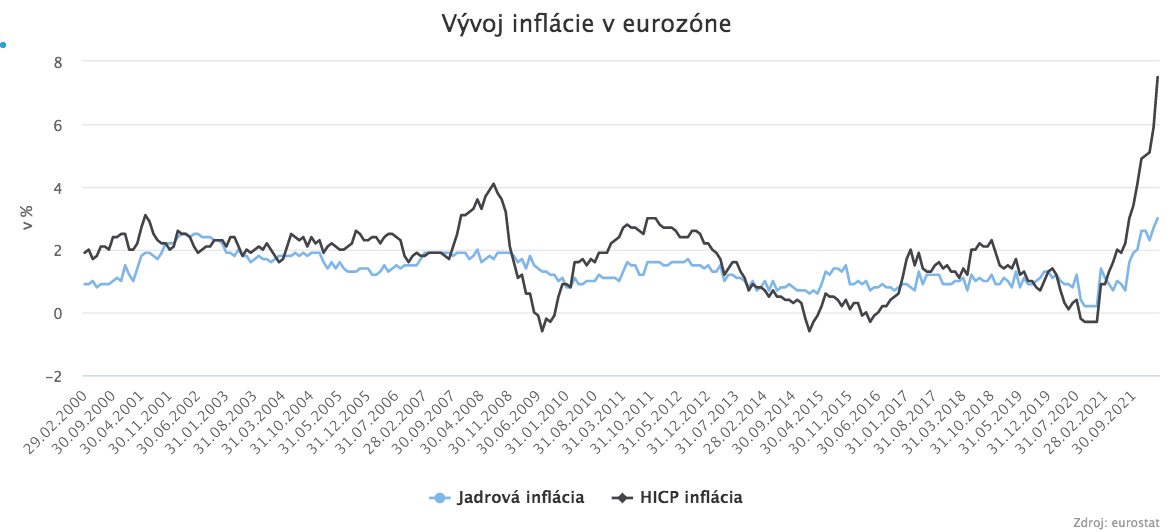

Among the most frequently mentioned and persistent issues is inflation, which still has not gone away and is largely driven by Russia’s actions. Energy prices troubled the world last year, and nothing has changed this year; energy commodity prices remain at high levels. In addition to the EU’s problematic policies, which make electricity and industrial production more expensive through emissions allowances, we also have Russia’s policy of tightening the taps. Already last year there were problems regarding the level of natural gas flows. At that time, the EU entered the winter season with lower volumes of gas in storage than in previous years. Thanks to a mild winter, the Union did not face a gas shortage, but low flows and inventories pushed prices higher. This resulted, and still results, in significantly higher energy costs, especially for businesses that did not lock in energy prices in advance and relied on prices remaining low. Households fall under regulation, and therefore large price jumps in energy do not affect them. It is important to understand that the prices of oil, gas, electricity, and coal actively evolve based on supply and demand in the markets, while production costs do not rise at such a dizzying pace as market prices. This brings attractive margins for the producers of these commodities. An advantage goes to those countries and companies that have long-term or direct contracts with extractors and can thereby bypass exchanges. If a business owner buys gas, oil, electricity, or coal directly on the exchange or from suppliers without long-term contracts, they face truly high prices. Other factors contributing to rising inflation include complications in supply chains, the war in Ukraine, the pandemic, and loose monetary policy. There is a lot of debate precisely about central bank policies. Many economists criticize their loose monetary policy and weak steps toward stabilizing it. The Fed, the U.S. central bank, has already begun to act and is raising interest rates, and it is expected to continue throughout this year up to a level of 2.5%–3%. The second step in fighting inflation is reducing the bank’s balance sheet, likely at a pace of USD 95 billion per month. The main interest rate in the U.S. may reach 3% and could continue rising next year as well. The eurozone has a similar problem with rising inflation, but it is still fundamentally different in two respects. The monetary union’s economy is not in as good shape, and the war in Ukraine does not help at all. Another difference is core inflation, as it is not rising as sharply as headline inflation. Core inflation does not include items over which central bank policy has minimal influence. For this reason, many central bankers primarily monitor core inflation. Today’s situation will put pressure on central bank governors to raise interest rates, which in the short term will weigh on stock valuations. Any recession, suggested by the development of the yield curve on U.S. bonds, will also not support stock growth. A paradox is occurring on the curve, since bonds with shorter maturities offer higher yields than those with longer maturities. This points to investor uncertainty, as they expect economic problems in the near term. This year will likely be highly volatile for stock markets, and opinions on whether the market will rise or fall differ even among the most respected banking houses in the world (JPMorgan Chase or Morgan Stanley).