Trump or Biden?

Only a few days remain until one of the most consequential elections in modern history. A nervous atmosphere, marked by uncertainty and tense expectations, prevails not only among voters and politicians, but also among investors. The outcome of the U.S. presidential election, scheduled for Tuesday, 3 November, will have major implications for the economy and financial markets.

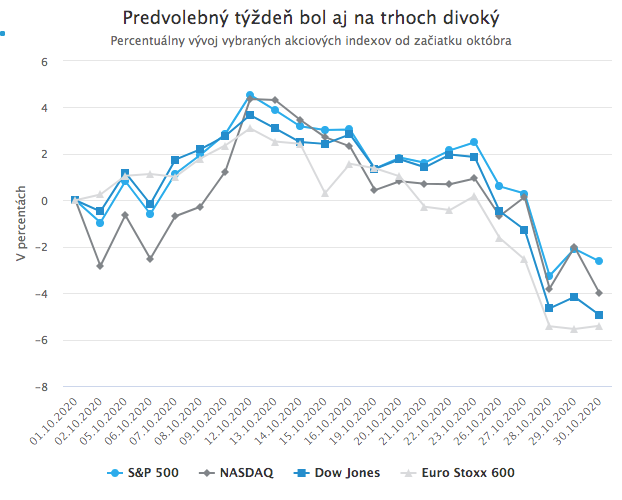

In markets, pre-election anxiety has been expressed mainly through a sharp decline in liquidity and heavy use of options to hedge against the risk of volatile post-election moves. This pronounced drop in liquidity, as investors cautiously waited for the result, contributed materially to this week’s steep sell-off in equities. Low liquidity, combined with negative dealer gamma, amplified downside moves triggered by news of renewed lockdowns in Europe.

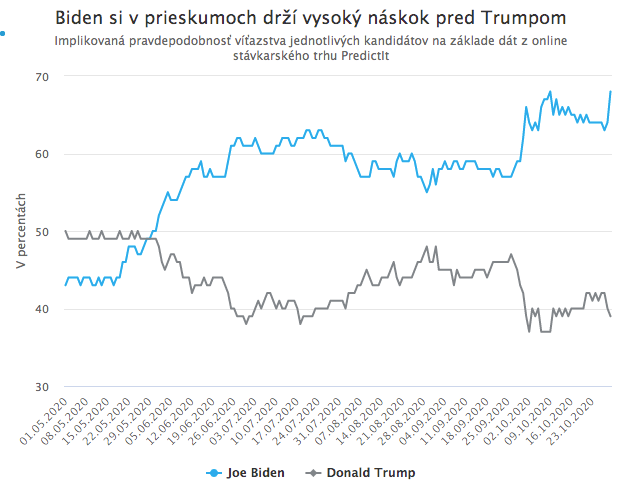

Incidentally, the S&P 500 fell by more than 3% in the week before the election, the first time this has happened in U.S. history. That alone underlines how unusual these elections are in every respect. What, then, should markets expect from the outcome? Would a second Trump victory be better for the economy and markets, or would investors prefer a Biden presidency?

Donald Trump frequently argues that a Biden victory would be a disaster for the economy and the stock market. During the final presidential debate, he warned voters that if Biden wins, “you’re going to have an economic depression the likes of which you’ve never seen… your 401(k) is going to go to hell, and it will be a very, very sad day for this country.”

It is hard to say whether such messaging persuaded any voters to change their preferences, particularly given that the United States (like much of the world) is already in the midst of an economic crisis unlike anything seen in recent decades. In any case, investors and analysts generally do not share these fears. On the contrary, most assessments suggest that Biden’s economic plan would deliver higher growth than Trump’s, particularly over the longer run. As Biden himself noted during the debate, the expert consensus leans in that direction.

Rabobank, for example, estimates in its latest election analysis that a Biden victory and the implementation of his economic platform would result in GDP that is 3.8% to 4.6% higher in the long term than under a Trump victory. It is worth noting that while Trump positions the economy as a core strength of his campaign, he has not published a detailed economic plan comparable to Biden’s. Instead, he has released a set of broad, bullet-point priorities for a second term.

Two paths to growth

From this agenda, the 2021 budget, the president’s previous statements, and especially his policy to date, we can piece together a fairly good picture of what Trump’s economic policy would look like in the next term. He would most likely try to kick-start the economy primarily through tax cuts (this time probably also for the middle class) and deregulation. Biden’s plan is significantly different from Trump’s. Perhaps the only area where they overlap is tighter regulation of digital monopolies. Biden plans to support economic growth through higher public spending and massive investments in infrastructure, science, education, healthcare, and the “green” economy. These higher public expenditures would be accompanied by higher corporate taxes (from today’s 21% to 28%), higher capital gains taxes, and higher income taxes for the highest-income groups. Raising the minimum wage is also part of the plan. By the way, perhaps the only area where the two candidates agree is tighter regulation of digital monopolies.

It is expected that Trump’s tax cuts would bring a short-term increase in disposable income (by about USD 3,500 per person by 2025), but over the longer term their impact on economic growth would be minimal. Biden’s plan, by contrast, should increase long-term economic growth. Rabobank writes in its analysis: “We expect economic growth to be higher under a Biden administration than in our base case, since the positive impact of higher public spending is expected to outweigh the negative impact of higher taxes for high-income groups.”

In the short term, Biden’s plan would lead to stagnation in average disposable income; however, over the longer horizon (to 2030) it is expected to grow more strongly than under Trump, precisely thanks to investments that increase the economy’s long-term potential and capacity. It is also quite possible that Biden’s plan will prove more beneficial for the economy even in the short term. His tax plan is highly redistributive in nature. Increasing income for low-income groups, which by definition have a higher propensity to consume than high-income groups, could significantly boost consumer spending. In the U.S. economy, which depends heavily on the consumer, this effect should not be underestimated.

The cost of the expected higher long-term economic growth under a Biden administration would likely be a larger increase in public debt (to 164% to 170% of GDP in the long run). Under a Trump administration, debt is expected to rise at most to 155% of GDP.

Would stocks perform better under Trump or Biden?

A positive impact on the economy today does not automatically mean a positive impact on the stock market. Equity markets and the real economy are more separated than ever before. A Trump victory is expected to have a clearly positive impact on the stock market. Companies would not have to fear higher taxes (they might even see further cuts), investors would not face higher capital gains taxes, and further deregulation could be expected, which reduces companies’ costs and translates into higher margins. That is a straightforward, positive impact on corporate profits that would lift stocks.

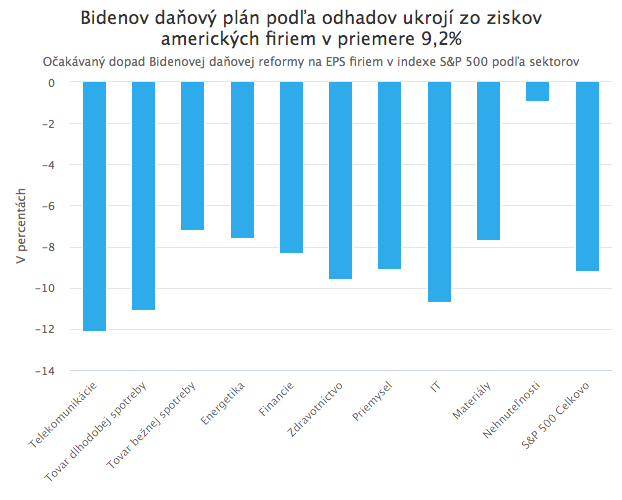

A potential Biden victory is more complicated. His economic plan would have a direct negative impact on stocks through two channels: higher corporate taxes and higher capital gains taxes. The planned corporate tax increase (plus the introduction of a minimum tax and the elimination of certain deductions) is estimated to reduce the average earnings per share of the largest U.S. companies by 9.2%.

The planned increase in capital gains taxes would likely lead to selling of some profitable positions in an effort to realize gains before the tax increase. JPMorgan estimates that assuming the tax increase would take effect in January 2022, the volume of such selling would be around USD 200 billion. Most of it would take place in the fourth quarter of 2021, just ahead of the planned increase. In the absence of other factors, such selling would mechanically pull stocks down by a few percent. However, it is unlikely to occur “in a vacuum”, and there are many factors that could offset these selling flows. JPMorgan and Goldman Sachs also point out, based on analyses of past capital gains tax increases, that the impact on the stock market has historically been one-off and short-lived. After the tax is implemented, stock buying tends to stabilize and then rise quickly again.

Against these straightforward and quantifiable negative impacts stand the expected positive effects of factors such as larger fiscal stimulus, a less confrontational trade policy including the removal of Trump-era tariffs, and greater predictability in domestic and foreign policy. These are significant but difficult to quantify, since uncertainty associated with Trump’s political approach has long constrained corporate investment. Reduced political uncertainty, lower tariffs, and a reduced risk of retaliatory tariffs on U.S. firms are therefore expected to lead to higher corporate investment, with a positive impact on long-term profitability. Higher fiscal stimulus would also support demand.

Unlike the negative factors, however, these positive effects are hard to quantify. The overall impact of Biden’s policy on the stock market therefore cannot be determined with certainty. Initially, analysts tended to believe the negative impacts would outweigh the positives. In recent months, however, the consensus has shifted toward a “neutral to slightly positive” overall impact. In any case, a Biden victory would most benefit stocks of companies in areas that would receive his planned public investment, namely infrastructure construction, green technologies, and research and education. Oil companies and other extractive firms with high pollution would almost certainly decline.

The impact of a Biden victory on the stock market is therefore uncertain. It could be mildly negative or positive. What is certain, however, is that the catastrophic scenarios Trump warns about will not occur. If Biden wins, the stock market will not “go to hell.”

A catastrophic scenario does, however, exist in the third possibility we already mentioned in a previous article. That risk is that Trump loses the election but simply refuses to accept defeat, claims the election was rigged, and refuses to transfer power. This would lead to paralysis, a deep political crisis, and the country would move toward the brink of civil war. The economy would, of course, be pushed to the sidelines, a road leading steeply downhill. Markets as well.

Such a scenario is not likely, and as the gap between Biden’s and Trump’s polling widens, the risk declines further, but it is not zero. After all, Trump himself says he will “see” whether he accepts the results, and he talked about rigged elections even when he won. Investors today fear this unlikely but potentially catastrophic scenario the most, and they are trying to hedge against the enormous jump in volatility it would bring. It is therefore very likely that if the election result is clear and the transfer of power is peaceful, stocks will rise regardless of who wins and what policy they pursue. What will matter is that the risk of the catastrophic scenario has been removed.

The dollar and bonds

The massive public investments envisioned in Biden’s plan would almost certainly lead to rising debt. Higher issuance of government bonds would therefore push yields higher. In the event of a Biden victory, markets would expect the U.S. Treasury yield curve to shift upward, especially at longer maturities. Of course, we are talking only about tens of basis points; any sharper rise in yields would be capped by the Fed. Such a policy would also, over the long run, tend to weaken the dollar. Among other currencies, the Mexican peso could benefit the most from a Biden victory.

In the event of a Trump victory, the opposite is expected: a stronger dollar and lower, or at least flat, bond yields, at least in the short term. However, there is one catch. In this respect, the outcome of the parallel Senate elections will be particularly important. If Biden wins but Republicans keep the Senate, they can effectively block a significant portion of Biden’s spending plans. The expected impact of his victory on different asset classes would then be muted.