Bonds Are Losing Their Diversification Benefits

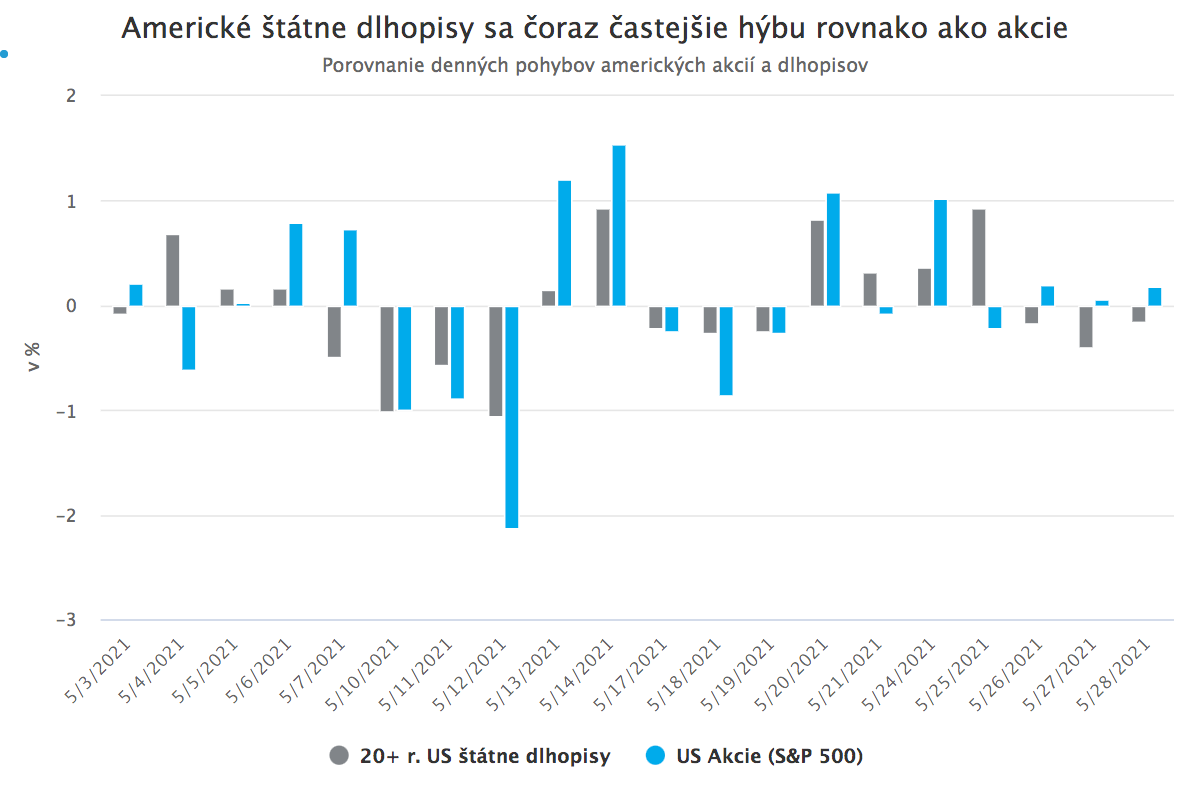

During May, major U.S. equity indices moved in the same direction as U.S. Treasuries for nine consecutive sessions. That record streak included two separate three-day runs of simultaneous declines. Historically, such a pattern is exceptionally rare. In the history of modern financial markets, U.S. stocks and Treasuries have seen only two instances of three straight days of concurrent losses, and never in such close succession.

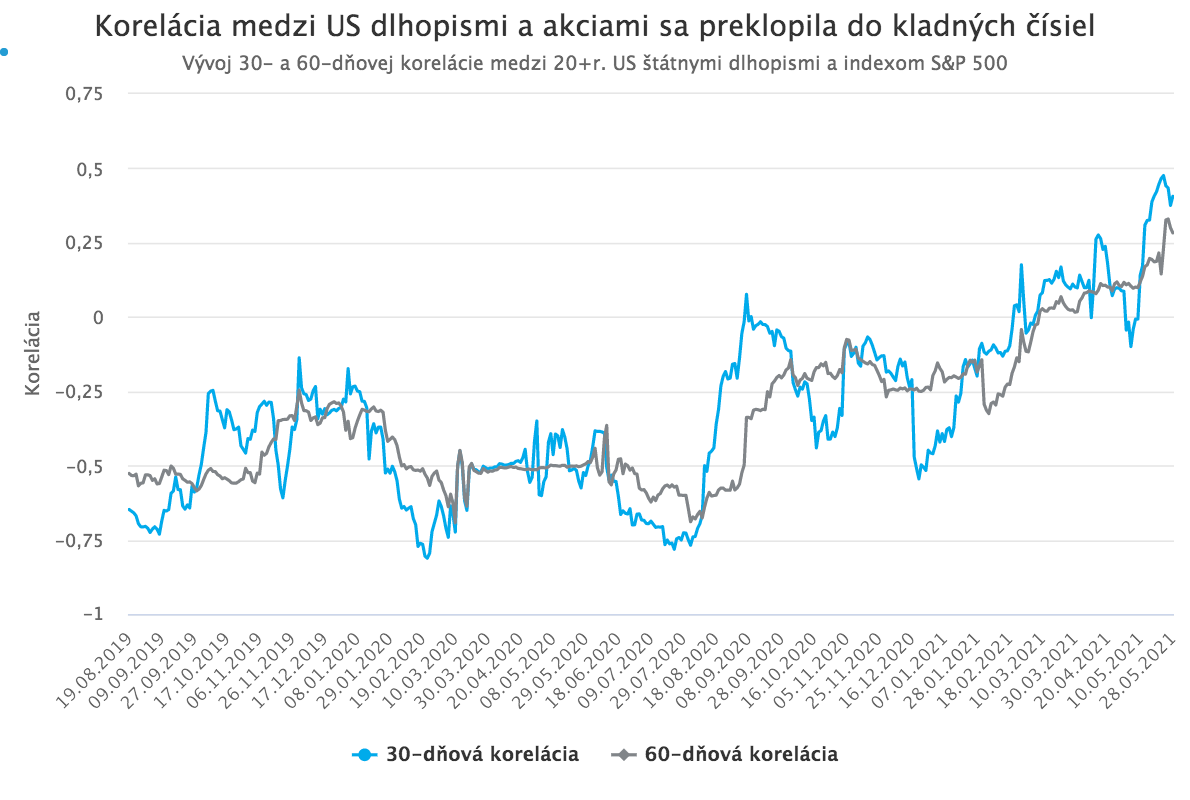

Partly as a result, the stock-bond correlation has flipped into positive territory in recent weeks and climbed to multi-year highs.

This is not merely an interesting but irrelevant historical curiosity. The assumption of a negative correlation between bonds and equities is one of the core building blocks of conventional portfolio construction. If the market behavior seen in recent weeks proves not to be a short-lived anomaly but rather a new feature of the current macroeconomic regime, a vast number of portfolios and investment strategies will need to be fundamentally reassessed.

A cornerstone of traditional portfolios

Classic investment portfolios typically rest on two main components: equities and bonds. Their relative weights vary depending on an investor’s risk profile, return expectations, time horizon, and other factors. What underpins virtually all such allocations, however, is the belief that equities and bonds are negatively correlated.

In practice, this means that when equities sell off, bonds should rise, cushioning part of the losses. Conversely, when bond prices fall (something that was rare over the past decade), equities should generally perform well. The assumption is rooted both in the characteristics of the two asset classes and in observed investor behavior. Equities tend to offer higher long-term returns, but they are more volatile and vulnerable to sharp drawdowns. Bonds typically deliver lower returns, but they are inherently safer and less volatile.

In periods of heightened economic risk and market stress, investors usually reduce exposure to risk assets such as equities and rotate into safe-haven assets, primarily government bonds. That “flight to quality” pushes bond prices higher. Under a negative correlation regime, a stock-bond portfolio should therefore be less risky and less volatile than an equity-only portfolio, while also offering meaningfully higher expected returns than a bond-only portfolio. For decades, this assumption broadly held: the correlation between bonds and equities was mildly negative, and a large number of successful strategies were built on that foundation.

Bonds have limited room for further price gains

Correlations between asset classes, however, are rarely stable over long periods. They shift with the macroeconomic and market backdrop. Over the past several years, a growing number of analysts have warned that the negative stock-bond correlation is not set in stone and could weaken substantially or even turn positive as the environment changes.

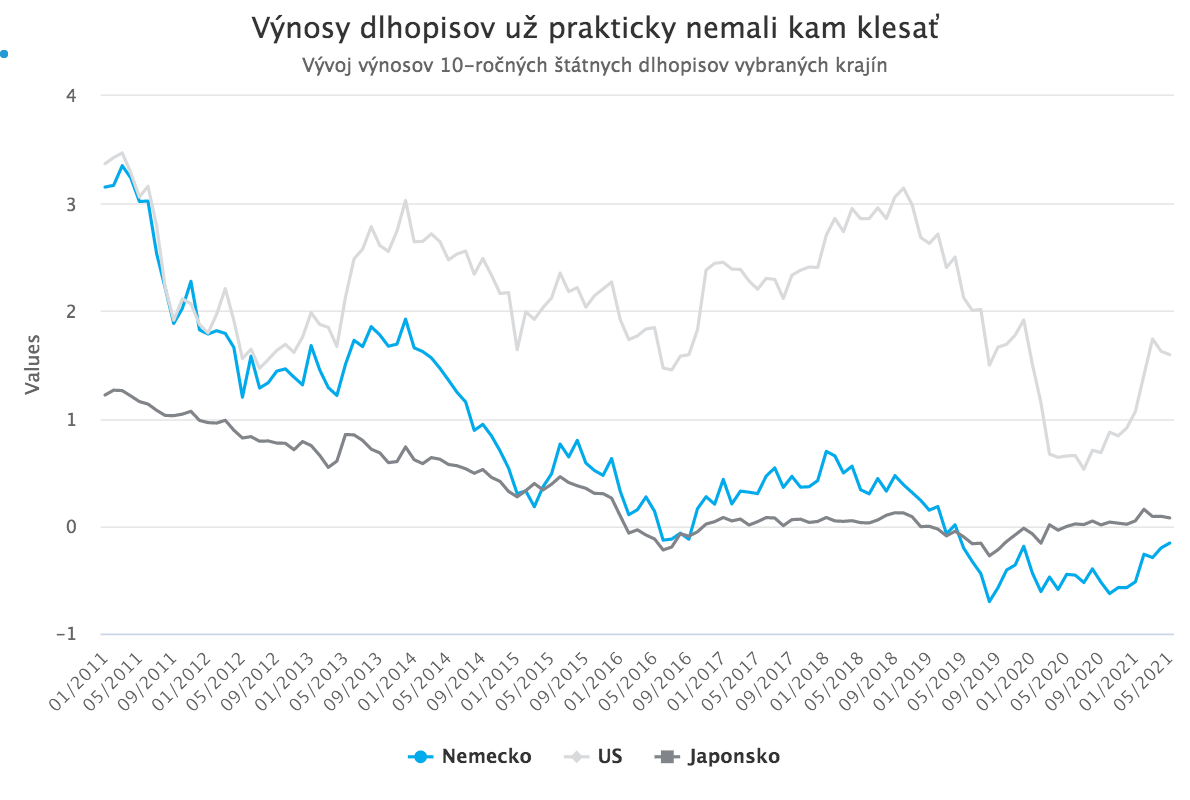

The past decade illustrates why. Equity markets rallied strongly while bond yields fell to record lows, in many cases into negative territory, as post-crisis monetary policy remained exceptionally accommodative. (Bond prices and yields move inversely, higher bond prices imply lower yields.)

This matters because, for bonds to offset a meaningful equity sell-off today, yields would likely have to fall sharply from already low levels, potentially deeper into negative territory. While recent years have shown that yields can reach levels once considered impossible, there are limits. Over time, bond yields cannot sustainably remain far below central bank deposit rates. Even the ECB has learned that policy rates cannot be pushed too deeply into negative territory without the costs eventually outweighing the benefits.

It no longer pays to rely on negative stock-bond correlation

Years of falling yields have pushed bond prices to levels where there is limited upside (in other words, limited room for yields to decline further), but considerably more downside (more room for yields to rise). At the same time, the era of declining yields has driven ever more capital into the parts of the equity market that benefit most from lower discount rates, particularly growth stocks in large technology companies. Their share prices rose sharply, their market capitalizations expanded rapidly, and they became an increasingly dominant force in major equity indices.

From one perspective, these shifts have transformed bonds from a stabilizing component into a potential source of portfolio risk. Yields now sit at levels where the asymmetry is unfavorable: there is far more room for yields to rise than to fall, and rising yields tend to be a headwind for equities.

The unusual joint moves in bonds and equities seen this month are therefore not just random noise. They reflect longer-term changes in the economy and financial markets. A key catalyst has been rising U.S. inflation, which pushed yields higher. That impulse may not persist. U.S. inflation could prove transitory, and other economies may not experience a similarly strong reopening accompanied by higher inflation.

Even so, the balance of risks remains skewed: higher yields (and falling bond prices) appear more likely than a renewed plunge in yields, and any sharp decline in bond prices now tends to weigh on equity markets as well. Traditional portfolios built solely on standard equity and bond allocations, and on the assumption of negative correlation between them, may therefore be significantly riskier than historical data would suggest.

It is thus prudent to complement such portfolios with additional components that are not positively correlated with both equities and bonds, such as real estate or commodities. At the same time, the equity sleeve can be adjusted toward sectors that historically benefit from rising yields, such as financials.