Investors Welcome the Expected Outcome of the US Election

From an investor perspective, the expected outcome of the US election is likely the best possible scenario. Equities welcomed it with a sharp rally. Biden in the White House should bring greater certainty and predictability to both domestic and foreign policy. A Senate controlled by Republicans, however, would also mean he will not be able to enact any major elements of his reform-oriented economic agenda.

As of Friday morning, at the time of writing this commentary, the final results of the US election are not yet known. It nonetheless appears highly likely that Joe Biden will become president, while Democrats will not secure a majority in the Senate and will also lose ground in the House of Representatives. Naturally, neither Democrats nor Republicans can be pleased with this outcome. From the perspective of investors, however, it is essentially the best possible result.

It means that the unpredictable and impulsive Trump will, in all likelihood, be replaced by a more predictable and rational Biden, who should bring much-needed certainty and predictability to both domestic and foreign policy. Management teams planning an investment in Mexico, expansion into the Chinese market, or imports from the EU will no longer have to worry about whether Trump might announce a trade war via Twitter in the middle of the night, accompanied by salvos of tariffs and retaliatory tariffs.

At the same time, a Senate controlled by Republicans and a weakened position of Democrats in the House would mean the Biden administration will not be able to push through any major parts of its program. Investors therefore would not have to fear tax increases, tighter regulation (with the exception of technology companies), and large public investments or any significant budget spending to support the economy are also unlikely to pass the Senate. The post-crisis political and economic status quo would thus remain intact, with all its positive and negative consequences for the economy and financial markets.

Economic support will remain on the Fed’s shoulders

The fact that Democrats will not be able to support the recovery of the pandemic-hit economy with fiscal stimulus (due to a Republican-controlled Senate) implies one thing: the full burden of supporting the economy will once again rest on the Fed. Fed officials have been repeating for months that the economy urgently needs fiscal support in the current situation, because the monetary-policy tools at the Fed’s disposal are not sufficient on their own.

It is, however, practically certain that once Biden becomes president, Republicans will suddenly rediscover their desire for a balanced budget and lower public debt, even though during Trump’s presidency they turned a blind eye to record debt growth and massive deficits (in a growing economy, no less). Despite the Fed’s urging, Democrats therefore will not be able to enact any significant increase in budget spending (fiscal stimulus) to support the economy.

The economy will thus likely face only a very gradual recovery, characterized by structurally low growth and strong disinflationary impulses. The Fed, seeking to support economic growth and combat deflationary pressures, will have no choice but to continue for years to come with an extremely accommodative monetary policy, marked by record-low interest rates and massive quantitative easing (so-called money printing).

As is well known, however, the transmission mechanism between quantitative easing and the real economy is weak. In other words, central-bank money printing has only a limited stimulative effect on real economic growth, while it has an immediate and direct positive impact on asset prices. The very idea of quantitative easing rests on the assumption that the liquidity injected into markets will lift asset prices. As a result, households and companies will feel wealthier and more confident, spend more, and thereby support the economy.

While the first part of this assumption holds in practice, since the relationship between liquidity (the amount of money in markets) and asset prices is quite straightforward, the second part is more complicated. Higher prices of financial assets translate into higher spending and higher investment in the real economy only to a very limited extent. The result of quantitative easing is therefore primarily rising financial asset prices alongside stagnation in the real economy. A side effect is, of course, a sharp rise in inequality, which can fuel social conflict.

A “blue ebb” pleased equity markets

Market reactions to the likely election outcome therefore reflect precisely the expected stagnation of the real economy combined with disinflationary pressures, long-term low interest rates, constrained public spending, continued attempts to stimulate the economy almost exclusively through monetary-policy tools (with all the above-mentioned implications), and the absence of tax hikes or tighter regulation.

The “blue wave” (Biden as president, Senate controlled by Democrats), which investors had begun positioning for in previous weeks and which would have brought almost the exact opposite, is therefore not materializing. Asset moves in recent days reflect this major shift in expectations. In markets, the blue wave has turned into a blue ebb.

Equities, naturally, responded to this shift in expectations with a sharp rise. Continued central-bank liquidity injections, the fading threat of higher taxes (both corporate and capital gains taxes), the absence of tighter regulation, and a more predictable geopolitical environment are broadly supportive for equity markets.

Procyclical rotation and reflation are not taking place

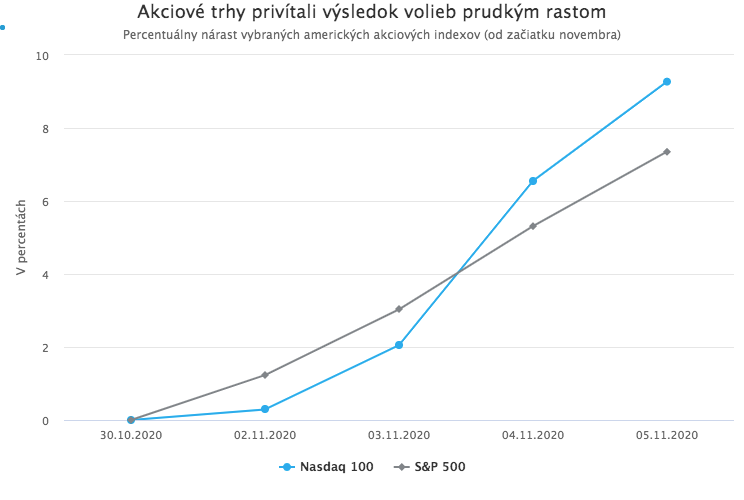

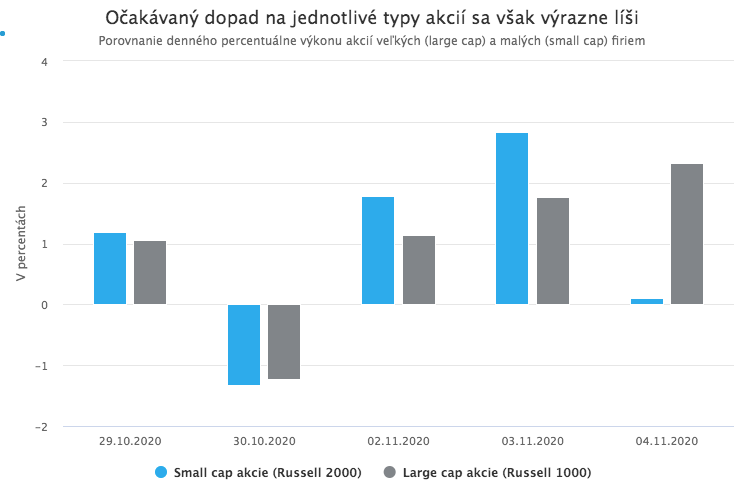

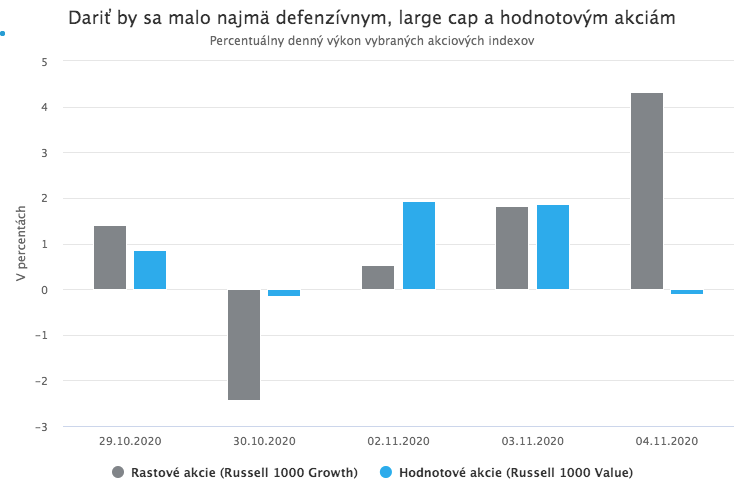

Not all equities benefited equally, however. The strongest reaction to the expected election outcome came from large technology stocks, which today function almost as a defensive investment and a substitute for bonds. They are among the few assets that still deliver attractive returns in an environment of low interest rates, suboptimal inflation, and a stagnating economy. The NASDAQ 100 is heading toward its best week of the year. Shares in other non-cyclical sectors, large-cap stocks, and growth stocks also rose sharply.

By contrast, the types of equities that would be expected to benefit the most from a cyclical recovery and fiscal stimulus clearly underperformed. These include small-cap stocks, cyclicals, and so-called value stocks. The procyclical rotation was thus once again halted at an early stage.

US Treasury bonds reacted with rising prices and a sharp drop in yields, especially at longer maturities. This move also reflects expectations of structurally low rates, suboptimal inflation, and relatively modest budget deficits, which, combined with continued quantitative easing, imply that the supply of long-dated safe government bonds will not increase, and may even decline. In short, reflation is not happening; on the bond market, duration-chasing is back in fashion.

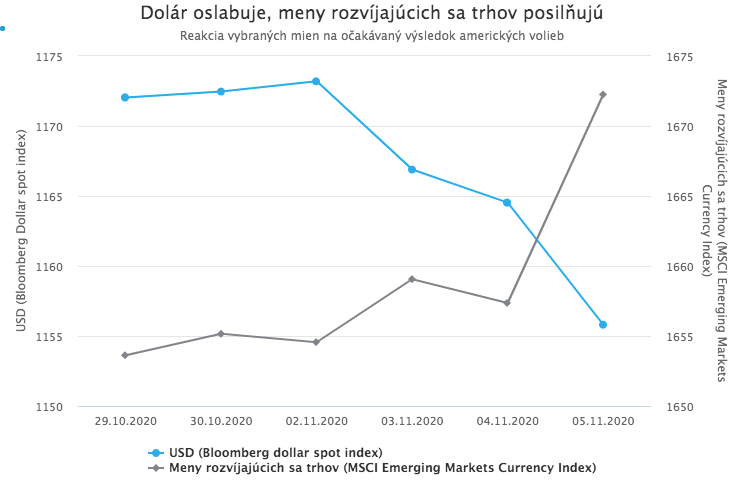

The dollar weakens, emerging-market currencies strengthen

In FX markets, the post-election period saw a sharp weakening of the US dollar and a simultaneous strengthening of emerging-market currencies. The dollar’s decline was likely driven in part by the same factors affecting equities and bonds (expectations of continued Fed money printing and structurally low interest rates, which reduce the dollar’s advantage from a positive interest-rate differential it enjoyed before the pandemic), as well as by the broader appreciation of emerging-market currencies against the dollar. This is, of course, also a result of the expected more predictable and less confrontational foreign policy under Biden.

The dollar was likely also pressured by a general “risk-on” mood among investors that emerged immediately after the first election results. It is worth noting that the dollar, not gold, remains essentially the only “safe haven” that typically strengthens in periods of elevated risk. Optimism in markets, by contrast, is usually accompanied by dollar weakness.

We still do not know the final result

The question remains whether investors have once again moved too quickly, as they did in previous weeks when they were positioning portfolios for a blue wave that ultimately did not materialize. The final election outcome is still unknown.

If Trump were ultimately to win, equities and bonds would not change materially, although FX markets would likely experience several sharp moves.

A larger market impact would occur if, alongside a Biden victory, Democrats ultimately managed to take control of the Senate. In that case, virtually all expectations described above would change, and market moves would reverse again. There would likely be broad downward pressure on equities, while value stocks would outperform growth stocks, small caps would outperform large caps, cyclicals would outperform non-cyclicals, and long-dated bond yields would rise.

Democratic control of the Senate does not appear likely today, but it cannot be ruled out. At least until January, when there will most likely be a new fight for two seats in Georgia, where neither candidate has yet secured the required 50% of the vote.

An additional, and even greater, risk, which we have highlighted before (here and here) and which investors seem to have dismissed too quickly after the election, is that Trump simply refuses to acknowledge defeat, refuses to transfer power peacefully, and the country slips into a constitutional crisis, in the extreme case even toward the brink of civil conflict.

As expected, Trump is already refusing to concede and speaking of election fraud, but his efforts so far appear more tragicomic and are supported only by a narrow circle of close allies without real influence. Even so, it may still be too early to fully dismiss this risk.

If, however, no surprise occurs, that is, Biden becomes president, the transfer of power proceeds relatively smoothly, and Republicans retain the Senate, one can expect the continuation of the market dynamics described above over the coming weeks and months